The accounting equation shows the relationship between resources in a business, which is also known as assets, and its obligations or liabilities, plus the owner’s equity in the business. This equation forms the basis of the double-entry bookkeeping system. Using this system, every transaction is recorded in at least two accounts so that the overall balance of a firm’s financial statements is maintained intact. Accounting equation is applicable to every business entity, regardless of its size or industry, as it provides a clear and organized method of recording and reporting financial transactions.

What is the Accounting Equation?

The accounting equation portrays a picture of how financially healthy a company is at a specific time by revealing what the business owns and owes and an owner’s investment in the business. Every business transaction affects one or more parts of the accounting equation and keeps the balance sheet in balance.

- Assets: These represent the firm’s assets. It can either be tangible, such as cash and inventories, buildings, and equipment, or intangible assets like patents and goodwill.

- Liabilities: These are obligations or debts of the company. Liabilities would include loans, accounts payable, and other forms of debt owed to third parties.

- Capital: This is sometimes referred to as shareholders’ equity in corporations. It refers to a residual interest in a company after all the liabilities are paid. It includes the owner’s investment in the business, retained earnings, and any profit that may be reinvested into the company.

What the accounting equation goes to show is that the assets of a firm can be financed either through debt, liabilities, or equity, owner’s equity. Every time a transaction happens, it affects at least two of these elements to such an extent that a balance sheet always balances.

Accounting Equation Rules

Several accounting equation rules are necessary for accurately recording transactions and maintaining balance within the financial statements. These rules include:

Dual-Effect Principle

Every business transaction involves at least two accounts and never disturbs the balance of the equation. Assume that a company purchases a machine by paying in cash. In this situation, one asset would decline cash—and one other asset would increase equipment.

Debits and Credits

In the recording of transactions, the accounting system uses debits and credits. There is always an equal as well as corresponding credit for every debit. For instance, when a business borrows money, it increases the liability of the business, which is credited, while increasing cash assets at the same time.

Equation Integrity

The accounting equation must always be in balance. Any type of imbalance indicates that there are errors in the accounting entries. It could be because of wrong postings, omissions, or duplication of transactions.

These rules lay down the foundation of the double-entry accounting system that ensures that every transaction is recorded exactly in the books of the company. It will reflect all sources and uses of financing as well as all different kinds of resource allocations.

Accounting Equation Fundamentals

The accounting equation finds its roots in the concept that a company’s assets must either be financed by liabilities or owner’s equity. The dual aspect concept further states that every business transaction has a twofold effect that maintains the accounting equation in equilibrium.

Business Entity Concept

The business is a legal entity separate from its owners. In this way, the accounting equation holds for the business, and personal wealth is not included. Owners’ equity simply represents the owner’s right to the assets of the business after the liabilities have been paid off.

Monetary Unit Assumption

Only those business transactions that can be expressed in monetary terms are accrued. This implies that the financial statements are consistent and comparable because items such as customer satisfaction, which are not measured in monetary terms, are omitted from the accounting records.

Time Period Assumption

The accounting equation applies over specific time periods-for example, fiscal years or quarters. It is because of this that businesses are allowed to periodically report their financial position and performance, thus recording all transactions taking place within the timeframe under consideration.

This serves as a base for ensuring the accuracy and consistency in the recording of transactions-a perfect reflection of the true financial conditions of a business in the financial statements.

Types of Accounting Equation

Though the core form of the accounting equation is used in most periods, there are different forms of the equation, depending on the requirements for financial reporting and the nature of the business. These types give further insight or make the equation more simplified, depending on what the purpose requires.

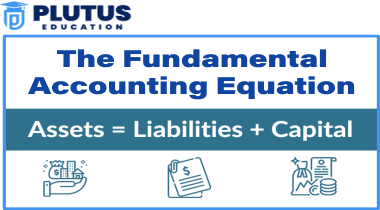

Basic Accounting Equation

The simplest form of the equation is:

Assets= Liabilities + Capital

This version is used to reflect the overall financial position of a business, showing how assets are financed through debentures or equity.

Expanded Accounting Equation

On the expanded version, one can get a better perception of the breakdown of equity components. It thus becomes easier to illustrate how financial activities affect the capital.

Assets= Liabilities + (Capital + Revenues − Expenses − Drawings)

In this form:

- Revenues increase capital.

- Expenses and drawings (withdrawals) reduce owner’s equity.

Corporation-Specific Equation

For corporations, the expanded accounting equation also includes components like retained earnings and dividends:

Assets= Liabilities + (Common Stock + Retained Earnings − Dividends)

This version is ideal for publicly traded companies, as it provides a detailed view of how profits are retained or distributed to shareholders.

Personal or Net Worth Equation

In personal finance, the accounting equation simplifies to:

Net Worth= Assets − Liabilities

This equation helps individuals assess their overall financial health by calculating net worth as the difference between assets and liabilities.

Accounting Equation Formula

The accounting equation formula represents the financial position of a business in a simplified form. On this basis, the formula is used for constructing the balance sheet and determining how assets are financed:

Assets= Liabilities + Capital

Here’s a breakdown of the formula’s key components:

- Assets: These include current assets such as cash and inventory, as well as long-term assets like machinery, buildings, and patents.

- Liabilities: These are categorized as current liabilities (due within a year) and long-term liabilities (due after more than a year).

- Capital: This represents the owner’s claim on the business after all liabilities are settled, including capital contributions and retained earnings.

The accounting equation ensures that the balance sheet never goes wrong since any alteration of one side has a corresponding effect on the other side. For instance, if a firm incurs more debt, then liabilities and assets, in that case, cash received increase.

Accounting Equation Format

To make this clearer, the accounting equation is written in very much the format of the balance sheet, so on the one side we have all the assets, and on the other side, the liabilities and equity. Here is one example layout:

| Assets | Liabilities + Capital |

|---|---|

| Cash | Accounts Payable |

| Accounts Receivable | Loans Payable |

| Inventory | Owner’s Capital |

| Equipment | Retained Earnings |

This layout reflects the balance of the accounting equation. For example, if a firm buys equipment on loan, then the increase in assets in the form of equipment will be matched by an increase in liabilities in the form of loan payable and therefore will be in balance with the accounting equation.

Basic Accounting Equation Examples

These basic accounting equations, through examples, will help you understand how various business transactions impact the financial position of a company.

Example 1: Purchasing Equipment on Credit

A business buys equipment worth ₹100,000 on credit. This transaction increases both assets (equipment) and liabilities (accounts payable):

- Assets increase by ₹100,000 (equipment).

- Liabilities increase by ₹100,000 (accounts payable).

The accounting equation remains balanced:

Assets= Liabilities + Capital

₹100,000= ₹100,000 + ₹0

Example 2: Owner Investment in Business

An owner invests ₹50,000 into the business as capital. This increases both assets (cash) and owner’s equity.

- Assets increase by ₹50,000 (cash).

- Owner’s Equity increases by ₹50,000.

The equation remains balanced:

Assets= Liabilities + Capital

₹50,000= ₹0 + ₹50,000

Example 3: Paying Off a Loan

A business pays off a loan of ₹20,000. This reduces both assets (cash) and liabilities (loan payable):

- Assets decrease by ₹20,000 (cash).

- Liabilities decrease by ₹20,000 (loan payable).

The equation remains balanced:

Assets= Liabilities + Owner’s Equity

₹(20,000)= ₹(20,000) + ₹0

These examples highlight how every transaction impacts the balance sheet and the accounting equation, ensuring that the financial records are always accurate and balanced

Accounting Equation FAQs

What is the expanded accounting equation?

The expanded accounting equation provides more detail by breaking down equity into its various components, such as revenues, expenses, and dividends:

Assets= Liabilities + (Capital + Revenues − Expenses − Dividends)

How does the accounting equation impact the balance sheet?

The accounting equation forms the basis of the balance sheet, with assets on one side and liabilities and equity on the other, ensuring the two sides always balance.

What are some examples of the accounting equation in action?

Common examples include purchasing equipment (increasing both assets and liabilities) or generating revenue (increasing both assets and equity).

Why must the accounting equation always balance?

The accounting equation must always balance to reflect the dual effect of every transaction, ensuring that the financial statements are accurate and complete.

What happens if the accounting equation doesn’t balance?

If the accounting equation doesn’t balance, it indicates an error in recording transactions, such as missing entries or incorrect amounts, which must be corrected to maintain accurate financial records.