Investment appraisal refers to evaluating possible investments in financial terms. Such an appraisal may occur within a defined period or may be short-term. One of its main objectives is to decide what investments should be made or not based on their costs, projected returns, related risks, etc. It utilizes several investment appraisal techniques so that the money is allocated correctly. The advantages and disadvantages of investment appraisal depend on how accurate the market is when it is done and its future in the business setting. The main advantage is that a structured approach can be adopted in making decisions in finances to ensure that one is in business with it. The one main drawback is that estimates are the basis of it, and sometimes miscalculations are made on those, leading to wrong investments. Despite this, businesses rely on it as a key decision-making tool for expansion, acquisitions, and long-term project viability, ensuring better resource utilization.

What is Investment Appraisal?

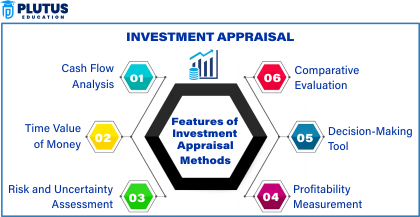

Investment appraisal examines an investment’s profitability and feasibility before committing funds. Different methods are used by businesses and investors to predict the returns and risks involved with the investments under consideration: for example, these might be the Net Present Value (NPV) method, Internal Rate of Return (IRR), payback method, or Profitability index. Appraisal will help an owner decide wisely, optimally allocate capital, and stabilize the business in the long term. A robust investment appraisal minimizes uncertainty and clarifies strategic planning; thus, it is an essential tool in corporate finance and capital budgeting.

Advantages and Disadvantages of Investment Appraisal

Investment Appraisal is integral to decisions made to keep a business afloat. The practice is the guide that finds investments that could bring the most future return from the present value of outlay. Investment appraisal compares several alternatives and provides information on the most efficient use of capital. Using investment appraisal methods, forecasts could be made on how investments will perform financially, and plans could be made accordingly. However, it is not without challenges. Such projections may be interfaced with external factors like inflation, competition, and economic instability. Bad investment decisions may arise due to misinterpretation of financial data, which may negatively affect the growth of the business.

Advantages of Investment Appraisal

Investment appraisal benefits a business entity in managing finances more competently because it lessens uncertainty. Some of these are listed below with some explanation:

Improved Decision

Making Evaluations of investments permits businesses to gauge various investment alternatives systematically, thus making the decision-makers the most likely candidates to select the best project for investment based on expected profitability. Applying the two methods of Net Present Value (NPV) and Internal Rate of Return (IRR), the insight brought along by using this method helps one establish the future cash flows and the total returns possible from the investment.

Effective Resource Allocation

Organizations often have scanty resources and must decide where the money goes. Investment appraisal thus results in such companies investing with the profit maximization investment; hence, capital caps are all kept clear. The company devotes itself to strategic allocations.

Risk Management

Investment appraisal identifies a business’s financial risks before investing. These schemes also address visualizing possibilities, understanding varying situations, and preparing for uncertainties, as the company would like to adopt to minimize the chances of incurring financial losses.

Long-Term Financial Planning

Cash flow forecasts for companies usually use the investment appraisal technique. Estimating revenues and expenses over time will base future planning for the company toward sustainable growth while avoiding liquidity crises.

Investment appraisal and methods have proven most important when comparing many existing projects within businesses. When these evaluations are done with different options, the company will finally present the highest returns investment possible from an aligned business goal.

Disadvantages of Investment Appraisal

The investment appraisal can provide structured decision-making; however, certain limitations abound. The table below discusses significant disadvantages along with their explanatory notes:

Uncertain Predictions

Investment appraisal methods depend upon financial projections, which cannot always be accurate. Future cash flows could be influenced by market conditions, inflation, and external factors; this often renders such forecasts useless. If businesses only rely on estimates, then it is likely that investment decisions will be made on a poor basis.

Ignores Qualitative Factors

Certain investment appraisal techniques consider predominantly financial metrics. Qualitative factors, such as brand reputation, employee satisfaction, and customer loyalty, significantly affect a company’s success and are usually disregarded.

Complex Calculations

Some investment appraisal methods, such as NPV and IRR, involve advanced financial calculations. Small businesses may be unable to interpret results in the decision-making process accurately. Companies lacking the expertise may find themselves miscalculating expected returns.

Over-Dependence on Numerals

Although investment appraisal lays out the numerical results, it ignores environmental circumstances, such as an economic recession, regulation changes, or competitive assault. Companies that focus only on numerical data and ignore external attacking forces may soon find themselves in a mismatch situation.

Time-Consuming Set-Up

Investment appraisal involves detailed data collection and analysis. The company has to gather financial reports, estimate future cash flows, and evaluate multiple scenarios. This may take some time, thereby delaying making investment decisions.

Types of Investment Appraisal

Investment appraisal methods are primarily divided into discounted cash flow methods and non-discounted cash flow methods. The main difference between these two categories is that discounted cash flow methods consider the time value of money, i.e., the cost incurred toward obtaining future cash flow; non-discounted cash flow methods do not consider the time value of money on their cash flow. Each method has unique advantages, limitations, and applicability depending on the type of investment being analyzed.

Discounted Cash Flow Methods

Discounted cash flow (DCF) methods consider the time value of money. That is, the funds received in the future will be worth less than the amount received today. These methods are helpful for appraising long-term investments, wherein the future cash flows are adjusted to present value.

Net Present Value

The net present value (NPV) is one of the most popular and widely applied investment appraisal techniques. It measures the difference between a cash inflow’s present value and a cash outflow’s present value. A positive NPV means the investment is good and profitable, while a negative NPV means losing money.

Internal Rate of Return

It is a further established method to measure the rate of return on investment by determining the discount rate that would make net present value (NPV) equal to zero. Since IRR increases, the attractiveness of the investment increases.

Discounted Payback Period

The period calculated with this method is where time is considered to pay back the initial investment outlay. This method discounts future cash inflows in a slight conversion to the allowance for a time as opposed to regular cash inflow and, thereby, is better.

Not Discounted Cash Flow Approaches

These cash inflow approaches consider money flow without considering the time value of money. These methods are convenient to measure and thus must be used for short-term investments and smaller companies with less finance for a profession.

Payback Period

The payback period shows the time for any investment to recover its cost. The payback period is one of the most straightforward techniques of investment appraisal and is generally considered for an organization where benefits are primarily in the form of immediate returns.

Accounting Rate of Return (ARR)

ARR measures profitability as the ratio of average annual profits to the initial investment cost; hence, it is a straightforward way of comparing different investment opportunities.

Which Method of Investment Appraisal Works Best?

The situation in question may dictate the very best methods of investment appraisal. For instance, the financial aims of the business, its risk tolerance or aversion, and the kind of investment will dictate which methods are best. Some methods emphasize yield more, while others focus more on the risks involved. The following tabulated description lists various investment appraisal techniques’ key features, advantages, and disadvantages, matching their applications.

| Method | Time Value of Money Considered? | Main Purpose | Advantages | Disadvantages |

| NPV (Net Present Value) | Yes | Measures total value added by an investment | Considers future cash flows; useful for long-term planning | Requires accurate cash flow forecasting |

| IRR (Internal Rate of Return) | Yes | Determines the expected rate of return | Helps compare different investment options | It may provide misleading results for projects with uneven cash flows |

| Discounted Payback Period | Yes | Measures time needed to recover investment | More accurate than a simple payback period | Ignores cash flows beyond the payback period |

| Payback Period | No | Measures how quickly investment is recovered | Simple and quick | Ignores time value of money and future profitability |

| ARR (Accounting Rate of Return) | No | Measures return based on accounting profits | Easy to calculate | Ignores cash flows and time value of money |

Each method comprises advantages and disadvantages, and businesses must adopt a mixture of such techniques to evaluate and obtain the best value for investments.

Pros and Cons of Investment Appraisal FAQs

1. What are the advantages and limitations of investment appraisal?

The advantages and disadvantages of investment appraisal will depend on how well the evaluation process is completed. The most important advantage is that a structured finance analysis will guide the business’s decision-making process. On the other hand, the central aspect of its disadvantage is that it relies on estimates that may prove to be erroneous in terms of ever-changing market conditions and unexpected costs.

2. Why is investment appraisal necessary for business decision-making?

Investment appraisal is an essential tool for evaluating possible investments in terms of profitability and risk. This allows for efficient allocations of resources, financial planning, and long-term stability. Investment appraisal techniques will enable a company to evaluate several projects vis-à-vis the other and select the most appropriate, thus minimizing financial exposure.

3. What are the universal techniques of investment appraisal?

The most popular investment appraisal techniques include NPV, IRR, Payback Period, and ARR, each giving different angles of view on investment profitability for application in business establishments with other investments and well-informed choices between them.

4. Specify the most critical limitations of investment appraisal.

Investment appraisal has limitations: reliance on uncertain forecasts, complex calculations, and ignoring qualitative factors. Primarily, it would focus on financial data, neglecting outside factors such as changes in the market or customer satisfaction. Some combined investment appraisals might be more effective with other strategic analyses for sound decision-making.

5. How investment appraisal helps in financial planning and risk management.

There would adequately be cash inflows and outflows to prepare financial plans because flows of funds formed through investments would need to be predictable. There would have to be adequate funds for operations. Risk planning will be done for potential financial risks identified before the facilities are committed.