Internal audit gives organizations a tool of unimaginable power in the pursuit of operational excellence and mitigation of risk. It involves a systematic and objective assessment or evaluation of operations within an organization with the aims of ensuring compliance with regulations, optimizing usage of resources, and, generally, enhancing controls. Internal audits expose flaws and offer actionable recommendations, making them the cornerstone of effective management and decision-making.

Internal Audit Meaning

Internal audit refers to a systematic, independent assessment of the internal processes, controls, and systems of an organization. Internal auditors are professionals who conduct internal audits focused on efficiency, risk management, and compliance, which cover not only internal policies but also external regulations. In comparison with an external audit that is mainly carried out for statutory purposes such as examining financial statements, an internal audit has a larger scope, which includes financial, operational, and governance factors.

It can, for instance, take the form of evaluating whether the company’s supply chain is good enough to be aligned with its sustainability goals or whether the company’s financial practices are compliant with regulatory standards. Its value addition lies in enhancing overall performance while at the same time protecting the organization’s assets.

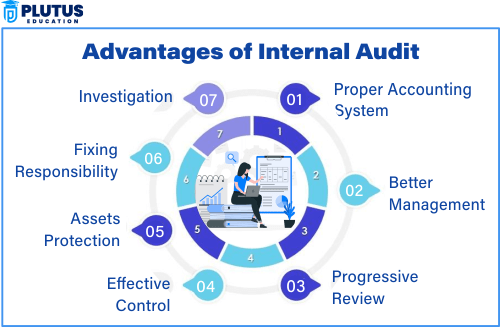

Advantages of Internal Audit

Internal audits offer numerous advantages that make them a vital function within any organization. Here’s a closer look at their key benefits:

1. Effective Management

Internal audits present a clear picture to management regarding strengths and weaknesses in the organization. Through this, inefficiencies and potential risk areas can be identified, and the process allows for informed decisions by the leaders on which areas to hasten their attention.

For instance, an internal auditor could note bottleneck points in some production processes or lacunas in environmental law compliance. Management, with such information, takes corrective action. Thus, ensuring smooth running and compliance.

2. Ongoing Review

In contrast to an annual external audit, internal audits are a continuous process. Continuous evaluations ensure that organizations continuously monitor critical functions and can establish and correct weaknesses promptly.

For example, monthly internal audits can monitor the inventory level. Therefore, avoid overstocking or stock-outs. This preventive method is risky-less and promotes operational efficiency.

3. Improved Performance of Staff

Audits help in employee development as they provide employees with constructive criticism of performance. Therefore, through this, an internal audit develops its employees’ work and relates it to the intended organizational goals and objectives, appreciating the negative and positive aspects of the performance.

More importantly, training can be implied through the process to fill up gaps that may exist, hence upgrading the skills positively. This will positively affect individual performance but will also positively affect the total productive output of an organization.

4. Ensures Optimum Use of Resources

An internal audit checks whether an organization’s resources, be they financial, human, or material are being used efficiently. It helps identify areas of waste or ineffectiveness in resource use.

For example, in an internal audit, some machinery may reveal that it is operating below potential because of scheduling problems. This then prevents the wasteful use of resources; the organization saves costs and increases output.

5. Division of Work

Internal audits are essential in maintaining clear roles and responsibilities within an organization. They ensure that tasks are assigned in the proper allocations where there is no duplication and lead to fewer chances of errors through workflow analysis.

For example, an internal audit may advise the finance department to split one’s job of processing invoices and authorizing payments so that one avoids risking fraud or mistakes.

6. Assets Protection

Internal audits ensure that organizational assets are protected. The type of assets—that could be of a physical nature such as inventory and equipment, or of an intangible nature such as intellectual property reviewed to ensure they remain properly safeguarded.

For example, the methods to safeguard sensitive data or machinery tracking and maintenance procedures. By dealing with weaknesses, asset mismanagement or even theft will not develop.

Limitations of Internal Audit

While internal audits offer numerous advantages, they are not without limitations. It’s essential to recognize these challenges to maximize their effectiveness.

1. Dependency on Auditor’s Skillset

The quality of an internal audit depends heavily on the auditor’s expertise and understanding of industry-specific challenges. A lack of adequate knowledge can result in overlooked risks or ineffective recommendations.

For instance, an auditor unfamiliar with emerging cybersecurity threats might fail to identify vulnerabilities in the organization’s IT systems.

2. Not Completely Independent

Internal auditors, being part of the organization, may face pressure from management or other stakeholders, potentially compromising their objectivity. This contrasts with external auditors who operate independently and are less likely to be influenced.

For example, an internal auditor might hesitate to report issues that reflect poorly on senior management, affecting the audit’s reliability.

3. Limited Scope

Internal audits often focus on specific areas or functions rather than taking a holistic view of the organization. This limited scope can leave critical risks unaddressed.

For instance, an internal audit might thoroughly review financial operations but fail to identify compliance issues in the supply chain.

Difference Between Internal Audit and External Audit

Understanding the distinction between internal and external audits is crucial for appreciating their unique roles in organizational governance.

| Aspect | Internal Audit | External Audit |

|---|---|---|

| Definition | In-house evaluation of operations and controls. | Management reports. |

| Objective | Improves processes, manages risks. | Ensures accuracy and statutory compliance. |

| Frequency | Conducted regularly. | Conducted annually or as required. |

| Scope | Broad, covering all operations. | Narrow, focusing on financial reporting. |

| Reporting | Reports to management. | Reports to shareholders or regulatory bodies. |

Internal audits are an essential component of organizational governance, offering invaluable insights into improving operations, mitigating risks, and ensuring compliance. Despite their limitations, they provide a framework for continuous improvement, helping organizations achieve long-term success. By understanding and leveraging the advantages of internal audits, businesses can enhance their efficiency, protect their assets, and create a culture of accountability and transparency.

Advantages of Internal Audit FAQs

What is the primary objective of internal audit?

The primary objective of internal audit is to evaluate and enhance an organization’s internal controls, risk management, and governance processes, ensuring compliance and operational efficiency.

How does internal audit improve resource utilization?

Internal audits identify inefficiencies and recommend better resource allocation, ensuring that financial, human, and material assets are used optimally to achieve organizational goals.

Why is internal audit important for asset protection?

Internal audits monitor asset management practices, safeguarding physical and intangible resources against misuse, theft, or mismanagement.

What are the key differences between internal and external audits?

Internal audits focus on improving processes and are conducted by in-house professionals, whereas external audits verify financial statements for statutory compliance and are performed by independent auditors.

Can internal audits help in fraud prevention?

Yes, internal audits detect anomalies, strengthen internal controls, and promote transparency, reducing the likelihood of fraud within the organization.