Advocacy threat happens when an auditor advocates or represents a client’s interest so much that they become biased and lack objectivity and independence. The threat results when an auditor defends or represents a client against legal, financial, or regulatory issues. In these instances, the auditor can lose professional skepticism. Affecting the integrity of the audit process. This article discusses advocacy threats, their effect on auditor independence, and real-life examples. Ways to prevent advocacy threats and other threats to auditor independence.

What is Advocacy Threat?

An advocacy threat arises when an auditor or accounting professional advocates for a client. Promotes a client’s interests to the point that their independence is compromised. These allegations may disturb independence, especially when auditors provide non-audit services. Such as representing a firm during a legal proceeding and handling marketing issues. Offering financial advice can quickly generate bias while auditing.

Objectivity can be compromised when auditors take the side of a client in judicial. It monetary issues, creating the potential for bias. This threatens the independence upon which the auditor relies in rendering an opinion. As the auditor’s interests as a client may intervene with their objectivity. This loss of independence can have serious implications for the credibility of the audit process and potentially lead to misleading financial statements.

Conflict of interest can occur in the presence of advocacy threats, which create challenges for auditors to exercise due to professional scepticism. In such cases, the client’s interests take over the public interest. Where simple ethics are no longer followed. Regulatory bodies such as IFAC and ICAI stipulate strict rules to maintain auditors’ independence. Threats against auditors engaged in advocacy breach these tenets. Underscoring the necessity of preserving the ethical foundations of auditing.

What is Auditor Independence?

Auditor independence is the independence of a firm that provides audit services to the client it audits. So, independence allows an audit report to be fair, transparent, and credible. Which builds confidence in the stakeholders, investors, and regulators.

The point is that non-independent auditors threaten the integrity of financial markets and the credibility of information. Audited information is being done by an auditor who is not independent. Investors would not want to extend capital to companies. Moreover, banks would not approve a loan because the auditor may have issued a misleading audit report.

For example, an auditor might be unable or unwilling to report a client. They suspect of financial wrongdoing if they have provided that client with consulting services, as they may lose valuable consulting income. That compromises auditor independence.

Examples of Advocacy Threats

Multiple scenarios can lead to advocacy threats, mainly where auditors are engaged in non-audit services that serve the client’s interests.

- Legal Representation of the Client: Auditors representing clients will always create a conflict in the form of a strong advocacy threat. When acting as a client’s legal representative in court or during similar regulatory disputes. The audit will have a vested interest in sharing and defending the client. Which can lead to stakeholder bias in financial reporting.

- Marketing or Promoting Client’s Financial Products: If an auditor has assisted the company in marketing the financial products (for example, shares or bonds), they may hesitate from an adverse audit opinion as it may prevent sales.

- Lobbying on Behalf of the Client: For their independence, auditors are not allowed to make officials and government lobby on the client’s behalf. For example, when an auditor signs off on a company’s tax exemption claims. They may hesitate to report misstatements in financial tax disclosures.

- Serving as an Advocate in Mergers and Acquisitions: If an auditor negotiates or structures a business transaction on behalf of a client, they may become emotionally or financially vested in the deal in question. This can impact their capacity to issue an unbiased audit report.

- Providing Investment Advice to Clients: Auditors give investments or valuations to the clients, which creates the auditor’s interest because he is also interested in the organization’s financial stability. It creates pressure to issue a clean audit opinion, even when the financial statements contain misstatements or misrepresentations.

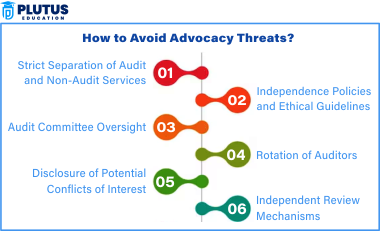

How to Avoid Advocacy Threats?

The independence of auditors and the independence of audits must be protected against advocacy threats to maintain the integrity and credibility of the audit process. Adopting successive measures, which make it possible, among other things, guarantees impartiality and maintains people’s trust in financial statements.

Strict Separation of Audit and Non-Audit Services

Audit firms must not render non-audit services (i.e. legal representation, marketing, financial advisory, etc.) to their audit clients. These conflicting services can create conflicts of interest and compromise the auditor’s independence. Dividing audit and non-audit services will help firm auditors remain neutral and concentrate fully on providing precise financial reporting so the validity of the audit process can be maintained.

Independence Policies and Ethical Guidelines

Professional codes of conduct exist for auditors, which must be adhered to when conducting their duties and which Operation Auditors must follow, such as the ICAI, IFAC, and ACCA. These rules help auditors remain objective and principled and behave professionally in what they do. These ethical principles serve as guidelines for auditors to conduct themselves with the impartiality and objectivity that is the foundation of the auditing profession, ensuring they uphold the trust placed in them by stakeholders and contribute positively to the financial ecosystem.

Audit Committee Oversight

Companies needed an independent audit committee to oversee the relationship between auditors and management. These committees help ensure auditors can do their jobs without company leadership interference. The presence of an audit committee encourages transparency and accountability, as auditors can review the financial statements without bias, and also serves as a safeguard to ensure that stakeholders in the organization are confident in the integrity of the audit process.

Rotation of Auditors

Auditor rotation is a means to mitigate familiarity threats, ensuring that audits are conducted with fresh perspectives. The familiarity arising from long-term engagement can create bias or impairment of judgment to the company’s financial statements and may indicate the need for change. Rotating auditors help establish independence, increase objectivity, and guarantee that the audit is an accurate, unbiased assessment of the company’s financial health.

Disclosure of Potential Conflicts of Interest

The auditors are required to declare all relationships or engagements that may give rise to advocacy threats before taking up an audit assignment. By disclosing potential conflicts of interest, auditors can help ensure these activities remain independent and stakeholders are aware of potential biases. Auditors can mitigate the damage to their credibility and the public trust in the audit process by proactively disclosing these relationships and establishing guidelines for their consideration to protect their credibility and that of the audit process from the public trust perspective.

Independent Review Mechanisms

Independent regulatory oversight in the form of external peer reviews ensures that the auditors are sufficiently unbiased. This helps ensure that auditors meet the established standards and are objective in their work. These external reviews serve as important checks and balances, as they work as a deterrent to ensure that auditors do not engage in any behaviour that may undermine the ethical standards of their profession and that the financial reporting process remains transparent and reliable.

Other Threats to Auditor Independence

Auditors’ independence is essential to facilitate the credibility of the audit process. Besides advocacy threats, other threats can impair auditor independence: self-interest threats, self-review threats, familiarity threats, and intimidation threats, among others. Training on these threats and how to mitigate some of them minimize the effects and help to uphold the integrity of objectivity and unbiased financial statements by auditors.

Self-Interest Threat

This self-interest threat occurs when the financial interest between the auditors and the client overlaps. For example, when owning shares, receiving personal loans or receiving contingent fees. Such financial relationships can affect the auditor’s independence and result in biased judgments. Auditors cannot be conflicted, as this would undermine the trust in the audit process.

Self-Review Threat

Intimidation threats arise when powerful clients pressure auditors to sign off on favorable audit opinions or ignore irregularities in the books . Such pressure can impair the auditor’s capacity to discharge his duties without bias. Auditors need to protect their independence by not succumbing to external. Organizational pressure and using their professional audit judgment so that both internal and external stakeholders get the actual results of the audit.

Familiarity Threat

When auditors have longstanding relationships with clients there is an increased potential for complacency or other forms of a familiarity threat. Auditors, over time, may get too cozy, leading to less stringent reviews. This can potentially impair their error or fraud detection capabilities. As some matters are likely sensitive or contentious, auditors must uphold objectivity by separating the previous relationship history from the current audit. Conducting the audit professionally.

Intimidation Threat

Intimidation threats arise when powerful clients pressure auditors to sign off on favorable audit opinions or ignore irregularities in the books . Such pressure can impair the auditor’s capacity to discharge his duties without bias. Auditors need to protect their independence by not succumbing to external. Organizational pressure and using their professional audit judgment so that both internal and external stakeholders get the actual results of the audit.

Advocacy Threat FAQs

What is advocacy threat in auditing?

An advocacy threat occurs when auditor advocates or favours a client’s position, sacrificing objectivity and independence.

How does advocacy threat impact auditor independence?

It causes bias and conflict of interest and diminishes the auditor’s capacity to issue an unbiased and credible audit opinion.

What are typical examples of advocacy threats?

Examples include legal representation, marketing client financial products, lobbying, and offering investment advice.

How can threats to advocacy be prevented?

By segregating audit and non-audit services and imposing independence policies. Implement auditor rotation, and monitor audit committees.

What are some other threats to auditor independence?

Other threats are self-interest, self-review, familiarity, and intimidation threats.