An audit engagement refers to an understanding between an auditor and a client to review and confirm the correctness and integrity of the client’s financial reports. An audit engagement letter is a written agreement between an auditor and a client specifying an audit engagement’s scope, responsibilities, and terms. An agreement outlines the parties’ expectations before initiating an audit. This letter is significant as it avoids misunderstandings and sets proper professional standards. This article will discuss the meaning, significance, and essential components of an audit engagement letter and information on its preparation and signing procedure.

What is Audit Engagement Letter?

An audit engagement letter is defined as the written agreement given by an auditor to a client before the commencement of an audit. It outlines the parameters for the engagement the audit’s scope and objectives, the responsibilities of the auditor, the responsibilities of the client, reporting format, and the professional standards that will be adhered to. The letter clarifies the responsibilities of both parties in the audit, minimizing the potential for disputes.

A company opening external auditors to audit a financial statement will receive an audit engagement letter that states the financial statements will be audited according to International Standards on Auditing (ISA) and will test financial transactions’ accuracy and compliance.

Importance of Audit Engagement Letter

An audit engagement letter is also a critical stage in the auditing procedure. The auditor and client must maintain transparency and professionalism throughout the engagement.

- Sets Clear Expectations: The engagement letter clearly states what the auditor will and will not do and what the client must provide, helping to avoid confusion about the audit’s scope and limitations. This also gives both parties an overview of the responsibility and deliverables, ensuring no confusion during the audit process.

- Legal Protections are Enforced: Your engagement letter acts as a formal legal agreement that can be used in the event of a dispute. It shields the auditor as well as the client during any disputes, making it clearly defined and understood by both parties and identifying their rights and obligations as it relate to the contract.

- Less scope for dispute: A well-worded engagement letter diminishes the potential of disputes over audit responsibilities. It lays down the parameters for the agency and the consultant so all expectations are established up front, preventing miscommunication and keeping the audit process in the right lane from beginning to end.

- Sets Professional Tone: The engagement letter establishes a professional and structured audit process. It upholds auditing ethics and professionalism, which allows both the auditor and client to conduct their work professionally during the audit, resulting in a productive audit.

- Explains Fees and Timeline: The engagement letter describes anticipated fees, along with their payment terms and timeline for completing the audit. This ensures clarity of payment and deadline and prevents conflict. This assists in planning the client’s financials and allows the auditor’s work to be done within a time frame agreed upon.

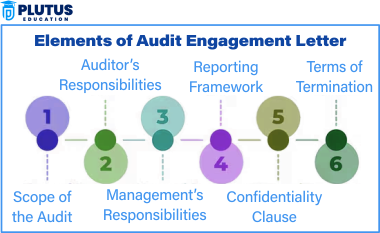

Elements of Audit Engagement Letter

The engagement letter is a comprehensive agreement between the auditor and the client and should include essential components that describe the audit engagement’s structure, scope, and expectations.

Scope of Audit

The audit scope defines what the auditor will focus on, such as financial statements, internal controls, or compliance with regulations. This part defines the scope of the audit and delineates the boundaries of what is and is not included in the assessment. For example, The audit will concern financial statements for the fiscal year ending 31 March 2024. The scope clearly defines the scope of the audit and the areas covered for both parties.

Auditor’s Responsibilities

The auditor’s responsibilities section explains what the auditor will be doing during the engagement (planning, execution, and reporting). It explains how the audit will be carried out under certain standards. e.g., “The auditor shall perform an audit per International Standards on Auditing (ISA). This ensures that auditor contentions and commitments are clear throughout the audit setup process.

Management’s Responsibilities

The section titled Responsibilities of Management outlines the duties of the client’s management to provide accurate records, financial statements, and compliance with laws. For instance, management is responsible for preparing the financial statements and maintaining compliance with tax laws.” This also outlines expectations for management and its role in preserving the integrity of the financial reporting process.

Audit Fees and Payment Terms

The last section of the Word is audit fees and payment terms. It describes the client’s financial obligations, including how much and when, to ensure both sides understand the financial terms of engagement. For instance, Audit fees will be INR 5,00,000, paid in two equal installments. This helps prevent confusion about financial arrangements.

Reporting Framework

Check different standards based upon the reporting framework as per accounting and auditing standards and design your audit. This part confirms the understanding between the auditor and the client regarding the principle on which financial reporting and auditing should be based. For example, the audit will be performed by IFRS and ISA. It guarantees that the audit is performed using accepted, industry-standard processes.

Confidentiality Clause

The confidentiality clause assures the entity being audited that the auditor will treat all information reviewed during the audit with the utmost confidentiality. This clause protects the client’s sensitive financial data and reinforces the auditor’s privacy. For instance, Any financial information accessed during the audit will remain confidential. This clause helps to ensure trust and protects against the possibility that client information would be disclosed without authorization.

Terms of Termination

How you can terminate the audit engagement by either party is defined in the terms of termination section. It outlines the rules and circumstances under which the audit may be terminated before completion. For instance, either party can terminate this engagement upon written notice of thirty (30) days. Doing so ensures that both parties know the process for terminating the engagement early if they need to.

Who Prepares an Audit Engagement Letter?

The American Institute of Certified Public Accountants (AICPA) provides audit engagement letters. The AICPA, as the body responsible for public accounting, has established rules surrounding audits, including when to present an engagement and conditions that must be met to conduct an audit. Your audit firm will prepare the specific terms of your engagement, which will use the appropriate AICPA template.

Some terms of the audit engagement are non-negotiable, so be aware when engaging an auditor. These include provisions regarding management’s obligations to make disclosures about the control environment, the audit’s limits, and both parties’ responsibilities. For instance, Your company’s counsel may also not be able to request modifications, like having the engagement letter prepared on the company’s letterhead or negotiating the terms of engagement.

What Terms of Engagement Should be Included?

All audit engagements need to be governed by the appropriate terms of engagement according to the AICPA; make sure that the terms are included in your engagement letter. The engagement letter can be varied, depending on the scope of services. When drafting the engagement letter for a SOC 1 or SOC 2 audit, the AICPA specifies that the following elements must, at a minimum, be included in paragraph 08 of AT-C section 205.

- Audit Objectives: The purpose of the audit.

- Scope of Work: What areas will the audit cover?

- Client’s Responsibilities: What documents and support must the client provide?

- Audit Fees: Payment terms and schedule.

- Timelines: When the audit will start and end.

- Confidentiality Agreement: Protection of sensitive financial data.

- Termination Clause: How the engagement can be ended if necessary.

When Should the Engagement Letter Be Sent and Signed?

When completed, the audit engagement letter should be sent to you before starting the audit and signed before any audit work begins.

It should be issued as soon as you have received verbal confirmation of your appointment as the auditor, but ideally, it should be signed before the commencement of any audit work.

If there’s no written engagement letter, send one to existing audit clients immediately so all documents are current and on record.

Also, in cases where the audit involves subsidiaries and the parent company, a separate engagement letter should be sent to ensure the terms are clear for both.

Audit Engagement Letter FAQs

1. What is an audit engagement letter?

An audit engagement letter is a professional agreement between a client and an auditor that details an audit’s scope, terms, and obligations.

2. Why is an audit engagement letter important?

It specifies expectations, avoids misunderstandings, sets out legal obligations, and promotes transparency in the audit process.

3. Who prepares the audit engagement letter?

The auditor drafts the engagement letter and forwards it to the client for approval and signature.

4. What are the most important things to include in an audit engagement letter?

It must have audit scope, responsibility, fees, timelines, confidentiality, and reporting standards.

5. When to send an audit engagement letter?

It should be sent prior to the commencement of the audit and signed prior to the commencement of any audit work.