Audit procedures are the steps taken to gather evidence and make conclusions about a business’s performance or results. These procedures include inspections, observations, inquiries, confirmations, and more. They consist of audit procedures through which the auditor examines financial statements, transactions, and internal control systems to ensure accuracy and compliance with regulations. This checks whether the economic data of a company are complete, valid and free from errors or fraud. Audit usually follows a systematic approach to examining financial integrity and reducing its associated risks.

A structured audit process brings enhanced transparency and trustworthiness to financial statements. Auditors adopt different kinds of audit procedures suited to the industry, size, and regulatory needs. Procedures also detect fraud and ensure compliance with policies and governing laws while confirming that proper accounting principles have been followed.

Meaning of Audit Procedure

The auditor uses audit procedures to gather and analyze financial information. These steps help auditors obtain sufficient and appropriate evidence to form an opinion on a company’s financial statements. Audit procedures include document reviews, confirmations, physical inspections, and analytical testing.

The auditor uses such a procedure to ensure that financials are accurate, reliable, and prepared according to accounting standards. The main aim is verification of the correctness of financials. It addresses the detection of misstatements, fraud, or even error. Companies must hold records since maintaining the same approach makes their audits smooth and avoids legal and financial complications later.

Audit Procedure Steps

Audit procedures, though defined approaches, must be scrupulously followed to attain reliable and accurate audit results. In-depth knowledge of the company enables auditors to customize their work based on business needs, including speaking with management and staff to get firsthand knowledge of financial affairs. Audit procedures comprise the following steps :

Get an Understanding of the Business and Environment

The phase during which the auditors get detailed into the understanding of the company’s operations, the industry dynamics, the financial reporting processes, and the regulations governing the company. Generally, reviewing documents such as the company’s internal controls prior financial statements helps the auditor determine areas of risk and the main areas for the audit.

Risk Assessment and Planning

Risk Assessment is the major part of the audit process, and during risk analysis, auditors assess the sections that would need auditing for financial, fraud, and error-prone areas. Under risk level assessment, the frauds also review the previous audit reports, present market conditions, and effectiveness of internal controls.

When the auditor identifies the business risk, he will prepare an audit plan defining the scope, objectives, and specific audit tests. The plan will provide an effective and focused audit related only to high-risk areas and segments, thereby managing the audit in manageable chunks.

Evidence Collection for Audit

Evidence sufficient and appropriate to substantiate the finding will comprise the analysis of documents, verification of transactions, and analytical procedures. The standards of audit evidence are based on reliability.

- Examining the records and documents related to financial transactions

- Confirmation of balances with third parties (e.g., banks, suppliers, customers)

- Physical verification of assets,

- Analytical reviews of financial data

Evaluation of Internal Controls

Internal controls underlie the complete error or fraud in the financial statement. The auditors would evaluate the internal controls and their efficiencies on the risk of material misstatements. Internal controls add strength to the audit risk basis, and hence, if there is a lack of adequate internal control, there will be an increase in the number of additional audit procedures.

Conducting Substantive Testing

The substantive test is intended to authenticate the data of a financial statement. Therefore, substantive tests include examining sampled transactions, account balances, and final financial statements about the individual account to ascertain and detect misstatements.

- Test of Details: Checking the particulars of some transactions, invoices, and receipts; Analytical

- Procedures: This is a financial comparison of data, time series, or a comparison done against industry benchmarks or standards.

Audit Opinion and Reporting

After the audit procedures have been performed, the results are documented in a way that builds toward an audit opinion. The auditors also write an audit report; the conclusion of this report summarizes the audit findings and the accuracy of the financials and discrepancies noted during the audit.

- An Unqualified Opinion: True and Fair Presentation with Compliance

- Qualified Opinion: Some areas are resolved as issues but do not affect general reliability.

- Adverse Opinion: Validity and Fairness of Financial Statements are questioned materially.

- Disclaimer of Opinion: Insufficient for reasonable assessment

Communicating Findings and Recommendations

In the final stage, the auditor discusses the findings derived from audits with management and other stakeholders. The auditor also offers recommendations for improvement to financial reports and internal controls within the organization.

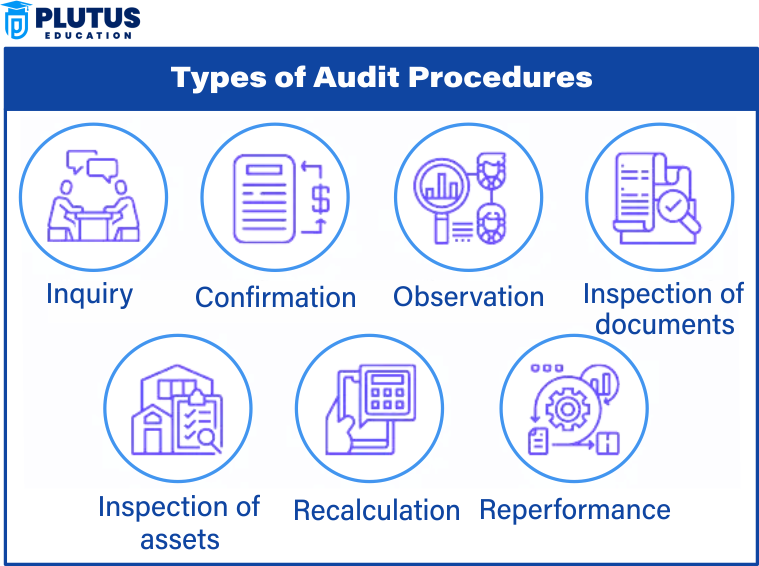

Audit Procedures Types

Audit procedures are of various types based on their purpose and method. Each type contributes to the auditor’s efforts to present, and therefore verify, financial data and to hunt for errors or fraud.

Analytical Procedures

Analytical procedures correlate financial information of a certain period with that of some prior periods to identify unexplainable variables or anomalies. The auditors may detect inconsistencies through ratio analysis, trend analysis, and benchmarking.

Example: Increased revenue of a company while expenses remained unchanged calls for an explanation from the auditors for such an unusual pattern occurrence.

Inspection of Records and Documents

The accuracy of transactions is confirmed by verifying records consisting of invoices, contracts, receipts, and financial statements. This verifies that all transactions recorded are sufficiently evidenced in authorized documents.

Example: Auditors check purchase invoices to validate recorded expenses.

Observation

Observation simply means the witnessing of business operations or internal controls. Such a procedure helps auditors in ascertaining compliance with laid-down policies and procedures.

Example: An auditor observes cash handling procedures to ascertain compliance with financial policies.

Confirmation

Confirmation consists of a request to third parties to confirm balances and transactions from an independent perspective. It is a tool to substantiate the financials.

Example: Banks confirm account balances, and customers confirm outstanding receivables.

Recalculation

Recalculation in the work of an auditor implies that the auditor checks the client’s mathematics. In other words, during recalculation, the auditor merely scrutinizes and re-performs certain numerical calculations to check for their validity and look for errors.

Audit Planning Procedures

Audit planning procedures provide a successful audit with its foundation since proper planning allows the audit to organize, streamline, and minimize risk while accomplishing tasks.

- Understanding the Relevant Requirements of a Client: Customer interaction is an important part of the auditor’s business process, generating financial objectives and relevant regulatory requirements.

- Determining Audit Scope and Objective: The audit scope specifies what will be examined, the objectives, and the reason. Hence, the major criteria help keep track of major financials.

- Risk Identification and Resources Allocation: By assessing the types of transactions done within the business, the auditors identify the possible risks and allocate the resources accordingly.

- Audit Program Preparation: An audit program describes specific procedures, timings, and responsibilities. This provides certain assurance that all principle areas receive systematic attention.

Compilation of Risk Assessment Procedures in an Audit

Risk Assessment during an audit is critical as it detects all kinds of financial and operational risks within an organization. An organization can identify by an audit from the risk assessment whether there is any misrepresentation or fraud within its economic data.

- Identifying Financial Risks: For example, auditors are aware of issues that might threaten revenue-generating streams and all other relevant operational problems as far as they might impinge on financial reporting.

- Testing of Internal Controls: A good internal control system will reduce the risk of financial misstatement. Thus, they evaluate the design and operational effectiveness of such controls by the auditors.

- Fraud Risk Assessment: Fraud risk areas are identified by auditors, which would prevent or detect such frauds.

Audit Procedure FAQ

1. Why is it important to have audit procedures?

Audit procedures ensure the financial statements are accurate, true, and fair under the prescribed accounting standards. They also help detect fraud, errors, regulatory violations, etc.

2. Describe the main steps in an audit procedure.

They consist of understanding the business, risk assessment, evidence gathering, internal controls evaluation, substantive procedures, forming an opinion, and reporting the findings.

3. Name the various audit procedures?

Analytical procedures, inspection, observation, confirmation, and recalculation.

4. How do auditors conduct risk assessments?

Risk assessments are opportunities for auditors to analyze financial records, internal controls, and fraud risks that affect potential risks for financial accuracy.

5. What do audit planning procedures do?

Audit planning procedures define the scope, objectives, and approach for audit to improve efficiency and effectiveness.