Audit risk is the inherent risk that an auditor may misstate the results of a financial audit. Such may occur when financial statements are materially incorrect, but the audit report states they are correct. The risk of a misstating opinion arises when financial reports contain material misstatements, which the auditor misses. The audit becomes the assurance, consciously or unconsciously, for shareholders, companies, and regulatory organs in ensuring financial transparency. Any act of omission or commission in auditing that goes undetected can spell disaster in terms of financial loss and legal action.

Understanding audit risk is paramount to auditors, management, and stakeholders. As a result, auditors must analyze various risks throughout an audit to ascertain that actual financial statements are accurate and fair. Generally, there are two main types of audit risks: inherent risk, control risk, and detection risk. Each of these risks contributes to the total risk faced by the auditor.

Audit Risk Meaning

Audit risk is the possibility that an auditor may misstate the audit opinion due to an error or fraud in accounting statements. When financial reports contain material misstatements, and the auditor does not detect them, this is a case where audit risk arises. It constitutes a major concern for the auditors since it affects the credibility of all financial reports and the decisions based on them.

Financial statements are prepared using accounting principles by the business, but errors, fraud, or misinterpretation can creep in. These can give the stakeholders almost false financial information if the auditors have lousy guesswork and fail to detect it. The risk is heightened when an organization has weak internal controls or complex financial transactions.

Audit risk is something auditors try to assess and minimize using various methods. These methods include understanding the environment of their client business, evaluating the internal controls, and performing substantive testing. The less audit risk there is, the more reliable the financial statements become, and further, this represents greater public trust in the system.

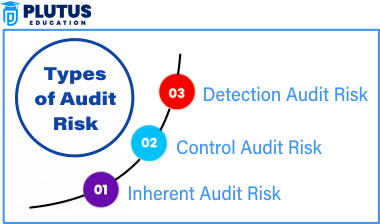

Types of Audit Risk

To reduce the effect of audit risk, auditors adopt policies and procedures for risk assessment. They analyze the financial data, internal controls, and external factors that could affect the financial strength of an organization.

Inherent Risk

Inherent risk is the risk of errors or fraud in financial statements without considering the business’s internal control. Banking and finance occupy much higher risk because of fluctuating regulations and voluminous transactions.

Factors influencing inherent risk

- The complex nature of transactions

- Industry regulations

- History of misstatements in the financial statements

- Management competence and integrity

Control Risk

Control risk is the risk that a company’s internal control systems will not prevent or detect material misstatements within a timely period. If the design or functioning of internal controls is weak, it is possible for errors and frauds not to be detected, thereby increasing overall audit risk.

Reasons for control risk

- Inadequate internal control

- Poor segregation of duties

- Lack of supervision or monitoring

- Human error in financial reporting

Detection Risk

Detection risk is when auditors cannot detect material misstatements in financial statements. Situations may arise whereby the audit procedures employed are insufficient to detect the errors, or human error comes into play.

Some of how a detection risk can be lowered include

- Ensure that audit procedures are effective

- Increase the size of the sample in audit tests

Auditing Consideration of Risk

Almost anything concerning some factors that have been treated is an auditing risk. These include inherent risk, control risk, and detection risk, and each plays an important role in determining the level of risk for an audit.

- Inherent Risk: Inherent risk can be understood as the possibility of error left to be accounted for at the point of unresolved internal controls aiming at rectifying such errors. Thus, this risk is high in industries involving elaborate transactions like financial services and manufacturing.

- Control Risk: Control risk exists when controls fail to prevent or detect material misstatements. Therefore, a company with weak controls will be open to fraud and financial reporting mistakes.

- Detection Risk: Detection risk is expected when the auditor has failed to detect misstatements or errors even after auditing. This risk is driven by the nature of audit procedures and the auditor’s experiences while executing them.

How Detection Risk Can Be Minimized?

All of these components interplay to determine the overall level of audit risk. The auditor can assure financial integrity and reliability if each element is correctly dealt with.

- Integrity: Increase the number of samples used in the audit. Review audit findings several times.

- Healthy risk assessment: Auditors’ knowledge of all three types of audit risks will also help them carry a more effective audit strategy”. Identifying and managing Inherent risk, controlling risk, and detecting risk, therefore, finally allows the auditor to gain greater assurance of the correctness and reliability of the financial reports. Advanced audit techniques

Risk Audit vs Risk Review PMP

Risk audit and risk review PMP are equally instrumental in project management and auditing. While both involve a risk assessment action, they aim for two different objectives. Audit risk is very important for financial accuracy, whereas risk review PMP is fundamental for project management itself. Both audits and reviews have a role in identifying and mitigating risk within various aspects of business.

| Aspect | Risk Audit | Risk Review PMP |

| Purpose | Identifies risks in financial or operational processes | Reviews overall project risks and their impact |

| Focus | Internal controls, compliance, and fraud detection | Project planning, execution, and risk management |

| Frequency | Conducted periodically or annually | Conducted at various project stages |

| Outcome | Audit report with risk findings and recommendations | Project risk management plan updates |

What is Perception of Risk in Audit?

Risk perception in audit refers to the risk perception towards financial statements carried out by the auditor, management, and other vested interested parties. The factors that lead to a different perception regarding the risk include industry trends, past experiences, and company policies.

- Industries inheritors: Highly regulated industries perceive audit risks differently.

- Environments of the economy: An economy in a recession or inflation will affect the perception of financial risk.

- Company reputation: Companies with a history of fraud will have an increased perceived risk.

What is Risk Assessment in Audit Risk?

Risk assessment in audit is a systematic procedure wherein prospective risks are identified, analyzed, and evaluated for potential chances of causing material misstatement of financial statements. It provides the auditors with an understanding of the business environment, an assessment of the internal controls in place, and identifies areas requiring more scrutiny during audit. The auditor undertakes a risk assessment to ensure he applies the proper audit procedure and effectively deploys his resources.

- Any company, for that matter, will not only be faced with financial, operational, or compliance risks that will constitute, in one way or another, an imperfect presentation of financial statements.

- These risks may stem from external factors dependent upon changing economic conditions or government regulations. In contrast, others may arise from an internal weakness dependent on poor financial controls or fraud.

- The intent of risk assessment in audits is thus aimed at minimising the chances that errors or fraud can slip through without being noticed. Maximising their ability to instill confidence in the financial reports.

Risk Assessment for Detecting Audit Risk

Audit risk assessment is a key area in the planning of an audit. An auditor who breezes through risk assessment may not note key areas that might matter and, therefore, garner an incorrect opinion in the audit report. The results could entail far-reaching effects on the stakeholders, including but not limited to investors, credit givers, and regulatory authorities. Therefore, risk assessment plays a primary role in ensuring that the organisation’s financial statements are not materially misstated but realistically demonstrate a company profile by viewing its financials.

Understanding the Business and Industry

Client’s business operations are analyzed to see how they relate to performance regarding industry trends, the governing regulatory environment, and the relevant financial reporting framework. The investigation may take into cognizance elements such as:

- Nature of the business and competitive situation

- Economic and industry-specific risks affecting financial statements or disclosures;

- Regulatory requirements and compliance obligations.

- Any previous audit reports or findings.

- Understanding the respective business would assist the auditor in also being aware of key financial risks and areas that may require scrupulous investigation.

Identification of Financial Reporting Risks

After understanding the business, the auditor understands the risks of financial reporting. These may include:

- Inherent risk is the result of transaction complexity.

- Control risk because of lack of internal control.

- Detection risk due to limitations in the audit.

Variation of Internal Controls

Internal controls serve as an essential deterrent to financial reporting risks. The auditors aim to assess the organisational internal controls and their efficiency in preventing or identifying misstatements.

- The design and implementation of internal controls

- The effectiveness of the segregation of duties.

- The reliability of the financial reporting systems.

Assessing Fraud Risk

Fraudulent activities matter a lot to audit. Thus, fraud risk concerning the misconduct of financial reporting and misappropriation of assets has to be assessed. For this purpose, auditors will have to:

- Identify areas where management may have been able to manipulate financial data.

- Analyse unusual transactions that may indicate fraud.

- Evaluate any incidents of fraud since previous audits were performed on this company.

Levels of Materiality

Materiality stands for the magnitude of misstatements that, individually or collectively, influence the economic decisions of users based on financial statements. The auditor determines materiality thresholds to hone in on the key aspects of the financial influencer. Auditors concentrate on the areas with the highest financial statement effects.

Developing an Audit Plan

The auditors usually prescribe a detailed audit plan outlining the procedures based on the risk assessment results. It includes:

- Specific audit procedure;

- The extent of testing required.

- A proper audit plan ensures that the audit covers all the risks identified and that the auditor thoroughly performs his job.

Implementation of Audit Procedures

After planning audits, auditors implement the procedures scheduled. This includes:

- Substantive tests to high-risk accounts.

- Analytical procedures to detect inconsistencies.

- Audit evidence to support audit conclusions.

Continuous Reviewing and Revising Risk Assessments

Audit risk assessment is a continuing process. Auditors continuously review and revise their risk assessments during the audit when new information surfaced. As they emerge, new risks would inevitably have to be construed with renewed changes to audit procedures.

Audit Risk FAQs

1. What audit risk is in brief?

Audit risk is the risk of an auditor giving a wrong opinion on financial statements due to errors or fraud not being detected during the audit.

2. How can auditors lessen audit risk?

Auditors can lessen audit risk through thorough risk assessment, employing strong audit procedures, and reviewing financial records in depth.

3. Why are the main audit risks?

The main components of audit risk are inherent risk, control risk, and detection risk. They characterize how these three components define a report on misstatements that can occur in the financial report.

4. What is the difference between inherent risk and control risk?

The nature of business is inherent risk, and weak internal operations give rise to control risk.

5. State the importance of Risk Assessment in Auditing?

Risk assessment enables auditors to concentrate resources in areas with high risk; thus, they can provide more accurate financial statements.