Difference between auditing and corporate governance. Auditing is an activity that characterizes a comprehensive process. That contributes significantly to corporate governance systems. Other specific terms relate to corporate governance, such as auditing as a whole system of rules and practices within a company. Auditing primarily concerns the methodical evaluation of a company’s financial statements, regulatory consideration and financial audit. Two main aspects denote business transparency and accountability. Other avenues would be the ethically acceptable means within which they practice laws.

Auditing and corporate governance conditions in organisations. Where trust in investors and fraud tendencies are minimised. Auditing entails checks on financial statements. Corporate governance encompasses facilitating ethical business practices. The two thus render credibility to organisations while sustaining their future development.

What is Auditing?

The word audit refers to any process of review meant to give a certain degree of assurance. Concerning an organisation’s financial records, internal controls, and operational processes. Accordingly, it assesses the organisation’s financial statement. Ensures it complies with other regulations. There are also instances in which the auditor examines the monetary transactions. Reports discrepancies or fraud cases and possible mismanagement.

This method of auditing has been the best for transparency in the affairs of companies. In other words, auditing assures stakeholders of the integrity and independence of the report. That fairly presents the organisation’s financial standing. Auditors are, therefore, expected to work within the rules and standards that govern auditing. Carrying the experience and attitude of professional scepticism and integrity in every situation. The audits are performed to protect the interests of investors, regulators, and other stakeholders. Assuring them that a company’s financial activities meet the existing regulations and ethical practices.

Corporate Governance Meaning

Corporate governance is the rules, practices, and processes that guide and control a company. However, it concerns a commitment to transparency, accountability, and fairness in decision-making. Good corporate governance describes ethical conduct. That enables a more efficient and responsible manner of business operation.

Corporate governance is also about the ownership and management of companies. It deals with policies, laws, and internal controls that guide the actions of executives and board members. Above all, strong corporate governance structures prevent clients’ financial scandals and regulatory offences.

As an important area of corporate governance, board structure and shareholder rights are joined with risk management. Corporate ethics for trust-building among investors and other stakeholders. Effective corporate governance practices give companies a competitive advantage. Also, sustainability over the longer term.

Type of Auditing and Corporate Governance

Auditors can be classified as either internal or external. Internal auditors are responsible for the organisation. Considerators conduct independent assessments to communicate their opinions. Financial statements to shareholders and regulators.

Types of Auditing

Corporate governance gives principles of ethical decision-making, accountability, and fairness. the two safeguard stakeholder interests against the backdrop of these enduring successes. Therefore, it is an organisation with solid auditing practices. Good corporate governance will minimise scandals, attract investments, and foster ethical behaviour.

- Internal Audit: An internal audit performed by internal auditors to review processes. Identify risks and improve operational efficiencies.

- External Audit: An independent auditor conducts this audit to give an objective opinion on the financial statements.

- Forensic Audit: This audit is performed to collect evidence. Detect fraud and ascertain misstatements, misconduct, or criminal behaviour.

- Compliance Audit: Determines whether the client has established satisfactory systems. In compliance with prescribed industry regulations and legal standards.

- Operational Audit: Auditing that assesses the efficiency. And the effectiveness of a particular business process.

- Tax Audit: Examining tax records for the required assessment of tax laws.

Types of Corporate Governance

The corporate environment governing auditing and corporate governance is heavily regulated. The essence of financial transparency and accountability. Statements are based on auditing and are accurate and reliable statutory reports on the economic state.

- Principle-Based Governance– This is based on principles and ethical standards but does not prescribe rules.

- Rule-based governance– requires strict and detailed compliance with corporate laws and regulations.

- Board-Centric Governance- This emphasises a board-centered governance model wherein the board plays a central management role.

- Stakeholder-Oriented Governance– Stresses the interests of all stakeholders.

Importance of Auditing

Auditing in the broader financial spectrum creates accountability and the organisation’s success. In a wider scope, auditing stimulates investor confidence, enhances corporate governance, and improves operational efficiency.

- Auditing gives strong credibility when assessing the financial position of any organisation. Audit reports form the basis for the decision-making process of investors, creditors, and regulators.

- Proper audits create an image of the company in the market. Regularly, investors and lenders would be much more comfortable. Investing in companies with an appropriate audit. On top of all that, an audit takes care of tax-wise compliance and avoids legal issues and penalties.

- Corporate governance is the collection of laws, principles, and processes. Through this, the corporation’s management is governed. It assures fairness, transparency, and accountability in the corporate decision-making process.

- The justification of good corporate governance is ethical conduct. Good governance creates a privileged environment. for the business to operate efficiently and responsibly.

- Corporate governance speaks to the systems through which companies are managed and controlled. That, in turn, encompasses efficiency and objectivity. And accountability in the prepared policies and laws.

- Internal controls guiding the actions of all executives and board members will be exercised. Companies with excellent corporate governance are inherently less lugubrious with financial scandals and regulatory penalties.

- Among the issues that corporate governance has to deal with are board structures. Rights of shareholders, risk management, and corporate ethical behaviour. These are all at stake in their respective importance as the main contributors. To establish trust between investors and other stakeholders.

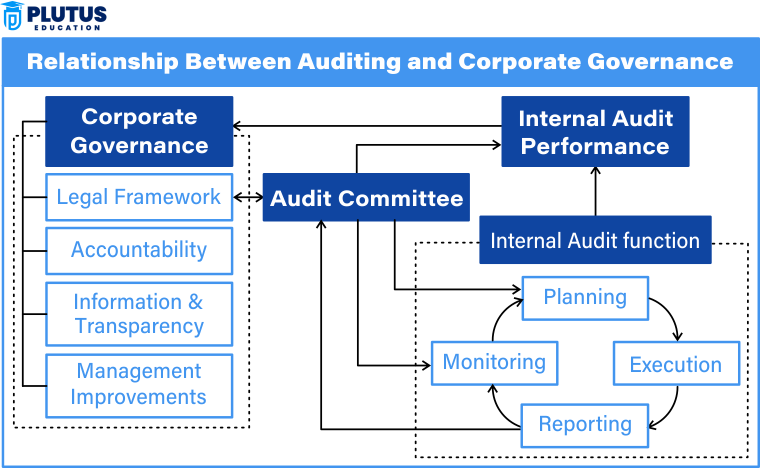

Relationship Between Auditing and Corporate Governance

Audits and corporate governance are interrelated, working interdependently to maintain the firm’s integrity, transparency, and accountability. A well-governed company will rely on audits to enhance and promote its credibility and image among stakeholders.

- Auditors review corporate governance policies for ethical and legal conformity. They will also examine board decision-making processes.

- Corporate governance, in turn, directly affects the nature and scope of auditing. Therefore, companies with enhanced governance mechanisms. Will conduct robust operations auditing to safeguard financial integrity and honest business conduct. Good governance will allow auditors to obtain relevant information from management and the latter’s undivided cooperation.

- The relationship between auditing and corporate governance is central to eliminating financial scandals and regulatory offences. Good governance ensures that whatever is recommended by the audit is implemented. It makes for better financial soundness and confidence from investors. Without good auditing, corporate governance mechanisms may also fail to recognize. Leading to mismanagement and subsequent regulatory implications

Objectives of Auditing and Corporate Governance

The culture should be thus established: approvals, transparency and accountability, and financial integrity. This goes for audits and corporate governance practices. Which protects stakeholders, minimises fraud, and enhances business efficiency. Within the credibility of value, the company garners investors’ trust to comply with all regulatory approvals.

- Ensure Financial Accuracy – Internal audits bring to light the truth and accuracy of general financial statement facts from misrepresentation.

- Fraud Detection and Prevention – Internal fraud and weaknesses can be detected. The internal controls are exposed through strong internal controls.

- Examine Risk Management – This is the one that helps an organisation minimise its financial and operational risks.

- Ensure Transparency – Benefit from an open business environment and its ethical nature.

- Hedge Stakeholder’s Interests – Safeguard the rights of investors, employees, and customers.

Importance of Auditing and Corporate Governance

Auditing and corporate governance remain central to corporate survival and continued expansion. as future financial estimates cannot measure their significance. However, future light requirements are built by the walls of confidence and foundations against fraud across financial instruments like auditing and its governance.

- Auditing is like an independent evaluation of financial statements. This ensures that the organisation understands the accurate picture of its financial position.

- It is a way of tax compliance, manipulations through figures, and the maintenance of investors’ trust. Companies thus face market fluctuations, severity and penalties from governmental organisations.

- Some of the aspects in which this corporate governance would have benefited. Including ethics regarding the decision-making of the shareholders, considering their interests. Ensuring that these ethics are enhanced in terms of the business.

- The benefit of such companies from the corporate governance dimension. They attract investments and retain human capital, thereby creating welfare in the organisation. Risk reduction brings the cash closer to a possible. Financial equilibrium and provides grounds for a sustainable future.

Auditing and Corporate Governance FAQs

1. Why is auditing and corporate governance important?

Auditing and corporate governance guarantee, in turn, the accuracy of the information in the financial statements. Ensure their transparency and hold them accountable to stakeholders.

2. What are the main types of audits?

These are the main types of audits. Internal, external, forensic, compliance, operational, and tax audits.

3. How does corporate governance impact business growth?

With better corporate governance, decisions are made within an organisation. Become more effective and attract investors to strengthen stakeholder trust. Resulting in sustainable business growth.

4. What are the main objectives of auditing?

These objectives are financial accuracy, fraud detection, risk assessment, and operational efficiency improvement.

5. How does auditing help in preventing fraud?

Fraud will be prevented by identifying discrepancies in the financial records, compliance with regulations, and improving internal controls to lower fraud risks.