An auditor is a third-party professional who inspects and assesses an organization’s financial statements, operations, or systems to validate accuracy, compliance, and reliability. Auditors Responsibility describes auditors’ tasks and responsibilities when scrutinizing financial statements, compliance with the law, and ability to find errors or fraudulent activity. Auditors are extremely important regarding financial accountability and transparency, confirming whether the financial statements reflect a true and fair view. They are supposed to work independently, adhere to professional guidelines, and evaluate risks properly. In this article, we will discuss who an auditor is, the major duties of an auditor, audit risks, and the guidelines auditors work under.

Who is an Auditor?

An auditor is a qualified professional checking a company’s financial records for accuracy, compliance, and reliability. Auditors review an organization’s financial statements, internal controls, and risk management processes.

A chartered accountant auditing a company’s financial statements checks whether revenues and expenses have been captured correctly. If there are discrepancies, the auditor returns to the board and regulatory bodies.

Auditors Responsibility

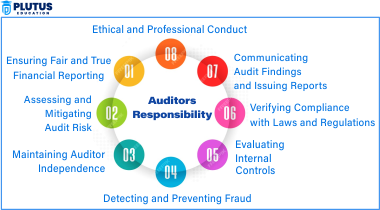

By their very nature, auditors occupy myriad roles to sustain financial accountability and adherence to regulations. Here are eight main auditor responsibilities, along with explanations.

Ensuring Fair and True Financial Reporting

Financial statements also require a proper audit. They review financial statements for mistakes, deficiencies, or any misinformation. Auditors ensure that such financial statements meet regulatory guidelines by following well-defined standards like IFRS or GAAP. This gives stakeholders confidence in the company’s financial status and aids informed decisions.

Assessing and Mitigating Audit Risk

They analyze the risk of a wrong audit opinion, which would misrepresent a company’s financial standing. They scrutinize high-risk areas (e.g. asset valuation, revenue recognition, etc.) for errors, fraud, or compliance. These risk-based auditing techniques help direct auditors’ attention to the highest risk areas: To obtain an accurate final audit opinion, auditors must cover the highest risk areas.

Maintaining Auditor Independence

Auditors should keep their distance from the company they audit so that outside factors do not affect their judgment. They cannot have any personal or financial ties to the company under review. Professional organizations such as ICAI and IAASB have robust standards from the independence perspective to ensure that auditors remain objective and maintain objectivity while conducting their audit services.

Detecting and Preventing Fraud

Auditors have an essential part to play in the identification of fraudulent activity taking place within an organization. They examine financial transactions to detect fraudulent behavior like phony invoices or fraudulent revenues. When auditors identify fraud, they report it to the audit committee or an appropriate authority. This role is crucial to keep companies transparent and accountable and mitigate fraudulent risks.

Evaluating Internal Controls

Internal controls auditors are responsible for testing whether the internal control systems in place within an organization are effective. Such controls are essential to mitigate errors, fraud, or operational inefficiencies. Auditors identify recommendations to control weaknesses and if any, recommendations to improve. With appropriate internal controls in place, it protects the company’s assets, minimizes risks, and leads to smoother work processes that benefit the organization in the long term.

Verifying Compliance with Laws and Regulations

Auditors ensure that companies comply with all the laws and rules that apply to them, from tax laws to corporate governance to labor regulations to environmental rules. Auditors scrutinize statutory records, tax filings, and legal contracts, as any deviation from the law can bring penalties or a legal case. Staying true to the rules protects the manufacturing company from costly penalties and reputational damage.

Communicating Audit Findings and Issuing Reports

No matter which type of auditor is auditing, auditors will write a report summarizing their findings after completing an audit. The report discloses whether the financial statements are fair and accurate, along with any risks or fraud. It might also include suggestions for improvement. Auditors share the report with relevant stakeholders such as management, investors, and regulators, promoting transparency and recommending future actions.

Ethical and Professional Conduct

Auditors must adhere to the strictest ethical standards to maintain professionalism and integrity. The code of ethics for professional accountants, which IFAC issued, provides guidelines restricting conflicts of interest, bribery, and other unethical activities. Compliance with such standards guarantees that auditors conduct their work honestly and impartially, fostering confidence among clients and stakeholders.

Internal Auditor Responsibilities

An internal auditor checks and tests that the company’s internal controls work effectively toward achieving business objectives. They analyze financial and operational processes to ensure everything works well together. The internal auditor identifies control weaknesses and recommends improvement opportunities so that the company can achieve its full potential.

The auditor also looks for trivial fraud and reconciles financial documents with operational data. Maintain the company’s compliance with laws, industry standards, and guidelines. Internal auditors also check whether the processes and procedures the company has in place are working as per the plan, which helps businesses steer in the right direction and develop their processes.

What are the Responsibilities of a Forensic Auditor?

A forensic auditor utilizes auditing and investigative techniques to identify whether fraud has occurred and its extent. They analyze financial records, transactions, and other relevant information to identify any instances of fraud. Forensic audits are extremely involved, lengthy, and meticulous as they ascertain the origin and impact of the fraud.

A forensic audit requires monitoring systems for a company to have in place. Proper monitoring generates excellent logs and measurements that allow the forensic auditor to develop a timeline of events. This is helpful to the company because it offers insight into how fraud can be prevented in the future by tracking suspicious activities and discovering the truth behind them.

Duties & Responsibilities of An External Auditor

AU Section 110, responsibilities of auditors performing attestation services AICPA In doing so, when an auditor is auditing financial statements, it is their job to design a plan and collect evidence, to say with reasonable, nor absolute, assurance that financial statements are free from material misstatements incident to error or fraud. Minor errors or fraud that do not significantly alter their statements are not the auditor’s responsibility.

Auditors for other types of attestation examinations follow SSAE 18. These standards guide how auditors should audit and report based on the service provided. However, auditors express opinions or conclusions, and the subject ‘matter’ is the responsibility of the client, not the auditor.

One of the audit mutually exclusive responsibilities of an auditor is to request a written and signed assertion. This statement asserts that the information presented in the financial statements is complete and accurate. Management must provide the information on which auditors base their findings. If management does not accept, the auditor needs to express a qualified opinion on the audit report.

Who is Responsible for Audit Risk?

Audit risk is the risk that the auditor may give an incorrect opinion because of misstatement, fraud, or deficiency in internal control. Audit risk is the responsibility of many different parties.

Audit risk is the risk that an auditor will issue an incorrect opinion after completing testing. Audit risk is a function of both the auditor and management. The accountant is ultimately responsible because that person has had the required professional skepticism and due diligence to challenge the evidence presented in support. Management, in turn, must present full and accurate information.

Auditors Responsibility FAQs

1. What are the main auditor responsibilities?

Auditors provide financial accuracy, fraud detection, internal control assessment, compliance, and independent reporting.

2. Who controls audit risk?

Auditors, company management, audit committees, and regulatory bodies control audit risk.

3. What guidelines do auditors follow?

Auditors abide by ISA, GAAS, ICAI, SEC, and IFAC Code of Ethics for professional auditing standards.

4. What is the difference between external and internal auditor responsibilities?

Internal auditors concentrate on risk management, whereas external auditors issue independent opinions regarding financial statements.

5. External auditor is responsible to whom?

External auditors are accountable to shareholders, investors, regulatory bodies, and audit committees.