Assertions relating to the balance sheet are the key statements made by management about the accuracy and reliability of the financial reports. These assertions help auditors ascertain whether a company’s financial position is being reported with an accurate and fair view in conformity with applicable accounting standards. Balance sheet assertions encompass all aspects of adequately recording assets, liabilities, and equity, the completeness of their inclusion, and appropriateness in valuation.

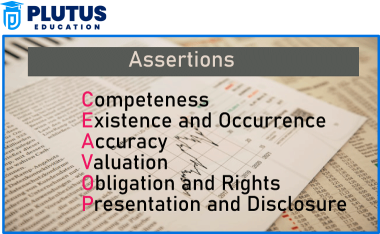

The balance sheet assertions can be divided into five main categories: existence, completeness, determination of rights and obligations, presentation and disclosure, and accuracy and valuation. These assertions assist the auditor in balancing the sheet and assessing the risk of possible material misstatement. An understanding of these balance sheet assertions is also useful in the financial auditing of the accounts and in explaining the accuracy of the financial statements.

Audit Assertions

Financial statement assertions are assertions made by management about the accuracy and completeness of the financial reports. These assertions assist the auditor in testing whether a company’s financial reporting assertions conform to accounting standards, like GAAP rules for the balance sheet and IFRS for financial statements. The balance sheet assertions can be divided into five main categories: existence, completeness, determination of rights and obligations, presentation and disclosure, and accuracy and valuation. These assertions assist the auditor in balancing the sheet and assessing the risk of possible material misstatement. Understanding these balance sheet assertions is also useful in the financial auditing of the accounts and in explaining the accuracy of the financial statements.

Purpose of Financial Statement Assertions

Several assertions exist regarding financial statements, but those primarily concerned with balance sheets are narrowly focused on the company’s financial position in an instant in time. Therefore, verifying the balance sheet and representing the financial statement is very important. These provide a systemized approach for auditing accounts. They would thus:

- To ascertain whether assets and liabilities are recorded correctly in the financial statements.

- To assure the financial statements in terms of legislation.

- To expose error or fraud in financial reporting.

- To assist the auditor in their external audit work.

Balance Sheet Assertions

Balance sheet assertions involve confirming the company’s assets, liabilities, and equity as presented in the financial statements. These assertions become very important for auditors to determine the adequacy of the organization’s internal controls as they pertain to financial reporting. In other words, the balance sheet assertions set out the criteria for an independent audit of the financial statements. They assist the audit in determining whether:

- Assets exist and are valued appropriately.

- Liabilities are disclosed correctly.

- The company owns its disclosed assets.

- The financial statements are complete and disclosed appropriately.

Importance of Balance Sheet Assertion

Each balance sheet assertion is equally important in ensuring that the existing financial statements truly represent the company’s financial position. There are five central balance sheet assertions, which include:-

Accuracy and Valuation

The accuracy and valuation assertion states that all amounts for assets, liabilities, and equities, as stated in the balance sheet, should reflect the correct amounts. This assertion is vital: wrong values mislead the investor and financial analyst.

Why Accuracy and Valuation Matter?

Indeed, if a company were to overvalue its assets, it may be deemed financially more substantial than it is and, in so doing, potentially mislead its investors. Indeed, if its assets were undervalued, it would make the company look weaker than it is and, therefore, have a detrimental effect on its stock price and ability to raise or secure capital. Such an assertion on valuation ensures the truth of what it claims about the respective financial information presented truly reflects its own fair and honest financial standing.

Audit Procedures for Accuracy and Valuation

Various audit procedures by the auditors under the heading of balance sheet verification will apply to testing accuracy and valuation against assets and liabilities:

- Examining invoices, contracts, and purchase receipts for amounts recorded.

- Examine depreciation and amortization calculations to ensure alignment with GAAP balance sheet requirements.

- Compare financial information with external references, including market pricing and third-party appraisals.

- Check impairment evaluations on any assets deemed to have lost value.

The audit procedures would thus assist in ascertaining the accurate picture of the financial statements while seeking to reduce the material misstatement risk.

Existence

Existence is an assertion affirming that all reported balance sheet assets and liabilities inevitably exist on or as at the date of the financial statements. This assertion will arm against the possibility of the beneficiary increasing their balance sheets more than once by reporting fictitious assets or misstated liabilities.

Importance of Existence Assertion

Companies may engage in fraudulent financial reporting by recording fictitious assets that make their financial position appear more substantial. Auditors test the existence assertion to see that the reported assets are authentic and valid.

Existence Audit Procedures

Through the following procedures, the auditors were able to ascertain the assertion of Existence:-

- Physical inspection of assets like inventory, property, and equipment.

- Banks confirm cash balances through bank confirmation.

- Accounts Receivables confirmations sent to customers.

- Investment holdings are corroborated through brokerage statements.

- Confirming that the Existence assertion is satisfied is critical to verifying the balance sheet and the stated financial misrepresentations.

Completeness Assertion

Completeness means the assertion that everything of a financial nature has been recorded on the balance sheet and that nothing has been omitted concerning assets, liabilities, or equity balances. With this assertion, there is a prevention for misrepresenting finances whereby liabilities are either downplayed or assets are kept out of the financial statements.

Importance of Completeness Assertion

When a company does not report all its liabilities, it sounds good news on a stronger financial position than it is; hence, it misleads investors and other stakeholders. The complete audit of financial statements makes the financial statements an accurate statement of the affairs of a company.

Audit Procedures for Completeness

Completeness assertion ensures an auditor’s prevention of the risk of financial misstatement. Completeness of assertion tested by auditors includes:

- Reviewing the accounting records of unrecorded liabilities.

- Examine vendor statements and unpaid invoices.

- Match the shipping documents with inventory records.

- Analytical study on transactional movements around the balance sheet date.

Rights and Obligations

The rights and obligation assertion entails that the company legally owns its assets reported in the statements and is a holder of liabilities.

Why Rights and Obligations Assertion Matters?

This implies that the company should not register any asset that is not owned nor be exempt from declaring any liability that should have been reported. This assertion depicts the company as to what it owns and owes.

Audit Procedures for Rights and Obligations

Meeting the rights and obligations assertion improves the accuracy of financial statements.

Auditors verify by:

- Review and check title deeds and ownership records over the property for audit of ownership records.

- Examine all lease and/or loan contracts.

- Check most insurance coverages for assets in us.

- Review supplier contracts for unrecorded obligations.

Presentation and Disclosure Assertion

The assertion of presentation and disclosure ensures that all company financial statements meet GAAP balance sheet requirements, are comprised of IFRS financial statements, and require all disclosures to be completed.

Why Presentation and Disclosure?

Transparent financial reports are vital for creating that investment confidence. Failure can bring regulatory fines and loss of faith among interested parties.

Audit Procedures for Presentation and Disclosure

By ensuring presentation and disclosure assertion, auditors help keep financial statements credible. Auditors evaluate assertions for presentation and disclosure by –

- Confirming adherence to accounting standards by financial statements.

- Assessment of financial reports for disclosures needed in the reports made.

- Classification of financial information.

- Checking on footnotes for proper footnote accuracy.

Balance Sheet Assertions FAQs

1. What is the purpose of balance sheet assertions?

Balance sheet assertions are intended to make the financial statements applicable to reflect a firm’s financial position fairly. They also lay a basis for auditors to check financial data’s validity, accuracy, and completeness

2. How different are accuracy valuation and completeness assertions?

Among other things, accuracy and valuation assert that all assets and liabilities are recorded against correct values, whereas completeness requires assertion that involves all financial data.

3. Why do auditors verify assertions in financial statements?

To meet any GAAP balance sheet requirements in a short while and also to prevent misstatements from occurring in the financial statements.

4. Why is valuation assertion important?

Valuation assertion states that financial statements fairly value assets and liabilities to prevent unfair inference, which might mislead stakeholders.

5. What are internal controls on financial reporting?

Internal controls over financial reporting are processes to ensure that financial statements are reliable, accurate, and comply with accounting standards. Controls also help prevent errors and fraud.