The balance sheet format is a fundamental tool in financial accounting, providing a snapshot of a company’s financial condition at a specific point in time. It systematically lists all the company’s assets, liabilities, and shareholders’ equity, thus helping stakeholders gauge its capital structure and liquidity. Understanding the balance sheet is crucial for investors, management, and financial analysts as it provides key insights into the company’s operational efficiency and financial health.

What is a Balance Sheet?

A balance sheet is a financial statement that reports a company’s assets, liabilities, and shareholders’ equity at a particular point in time. It offers a basis for computing rates of return and evaluating its capital structure. The balance sheet is commonly used for a detailed analysis of a company’s financial health and operational efficiency.

Components of a Balance Sheet:

- Assets: Resources owned by the company that are expected to bring future economic benefits.

- Liabilities: Obligations the company owes to outsiders that it must settle in the future.

- Equity: The residual interest in the assets of the company after deducting liabilities.

Assets must always equal the sum of liabilities and equity, maintaining the foundational accounting equation:

Assets = Liabilities + Shareholders’ Equity.

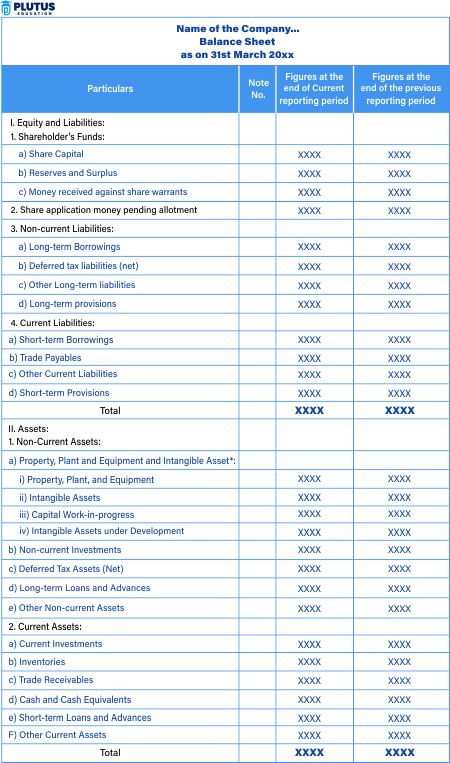

Balance Sheet Format

The structure of a balance sheet is divided into two main sections—assets on one side, and liabilities plus shareholders’ equity on the other. This format ensures that the balance sheet always balances according to the aforementioned equation.

Vertical Format

- Current Assets: Cash and other assets that are expected to be converted to cash within a year.

- Non-current Assets: Long-term investments, plant, property, and equipment.

- Current Liabilities: Obligations due within a year.

- Long-term Liabilities: Obligations payable over a longer period.

- Equity: Includes common stock, preferred stock, retained earnings, and treasury stock.

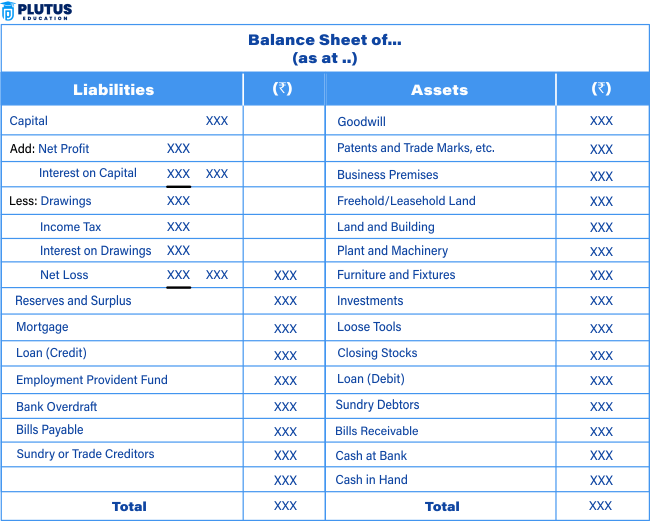

Horizontal Format

A horizontal balance sheet format presents assets on the left side and liabilities with equity on the right side. This layout allows for easy side-by-side comparison of a company’s financial position.

How to Prepare a Balance Sheet?

Preparing a balance sheet involves several systematic steps to ensure accuracy and compliance with financial reporting standards.

Steps to Prepare a Balance Sheet:

- Identify and Calculate Total Assets: Sum all current and non-current assets.

- Identify and Calculate Total Liabilities: Include all current and long-term liabilities.

- Determine Shareholder Equity: This can be derived by subtracting total liabilities from total assets.

- Compile the Data: Arrange the data into the balance sheet format, ensuring that total assets equal total liabilities plus shareholders’ equity.

Solving Examples of Balance Sheet

To elucidate the balance sheet format, here are examples presented in a table format. These examples will showcase typical entries found in company balance sheets:

| Category | Example Entry | $ Amount |

|---|---|---|

| Assets | ||

| Current Assets | Cash | $50,000 |

| Accounts Receivable | $30,000 | |

| Non-current Assets | Property | $300,000 |

| Equipment | $150,000 | |

| Liabilities | ||

| Current Liabilities | Accounts Payable | $40,000 |

| Long-term Liabilities | Bank Loan | $200,000 |

| Equity | Common Stock | $100,000 |

| Retained Earnings | $190,000 |

Conclusion

Understanding the balance sheet format is essential for anyone involved in the financial sector, as it provides crucial insights into a company’s financial strength and operational capabilities. By correctly structuring and analyzing the balance sheet, stakeholders can make informed decisions regarding investments, credit, and strategic planning. The balance sheet remains a critical tool in financial analysis, highlighting the importance of accurate and transparent financial reporting.

Balance Sheet Format FAQs

1. What is the most critical aspect of the balance sheet?

The most critical aspect is ensuring that the total assets always equal the sum of total liabilities and shareholders’ equity.

2. Why is it important to separate current and non-current items in the balance sheet?

Separating these items helps in assessing the liquidity and financial stability of the company, providing clear insights into short-term and long-term financial health.

3. How often should a balance sheet be prepared?

Typically, balance sheets are prepared quarterly and annually to comply with financial reporting standards and to keep stakeholders informed.

4. What role does shareholders’ equity play in a balance sheet?

Shareholders’ equity represents the owner’s claims after all liabilities have been settled. It is a key indicator of the financial health and net worth of the company.

5. Can a balance sheet show company performance over time?

No, a balance sheet provides financial information at a specific point in time. To analyze performance over time, one would examine multiple balance sheets in conjunction with other financial statements like income statements and cash flow statements.