The 2015 Bank of Baroda scam rattled India’s financial system, bringing to light severe weaknesses in India’s banking infrastructure and its operating ethos. This scam relates to illegal transfers of about ₹6,000 crore into companies situated in Hong Kong and Dubai by way of 59 such fraudulently opened bank accounts at the Ashok Vihar branch in New Delhi. These transactions were falsely reported to have been made for the import of goods, including dry fruits, rice, and cashew nuts, but such goods were never imported. The scam conducted in the Bank of Baroda involving forex has also thrown open some significant weaknesses in the bank’s compliance and monitoring systems. In this regard, it has been much more consequent in bringing out the risks that arise from inappropriate internal controls, governance issues, and weak KYC rules.

The revelations of the Bank of Baroda scam of Indian rupees 6000 crore tarnished the public image of the Indian banking system. It highlighted issues surrounding the way financial institutions process high-volume transactions and adequately comply with regulatory requirements.

Bank of Baroda Scam

Those who operate the Bank of Baroda fraud made the scandal focalize the unlawful extraction of money that looks and is presented as a legally legitimate trade-based remittance. The scam became a national controversy due to its scale and the involvement of a public sector bank. Fraudsters use the forex services provided by the bank to conduct criminal activity by bypassing regulatory mechanisms. The money was routed to Hong Kong and Dubai, falsely labeled as payments for imported goods. Investigations later established that these were fraudulent transactions as no goods were imported, and the companies that received payments were essentially shell companies.

The very ease with which these scams were perpetrated was what made them all the more alarming. The Ashok Vihar branch, which had no previous experience in processing significant foreign currency transactions, observed an abnormally large number of remittances over some time. By itself, this branch transacted amounts to ₹6,000 crore between July 2014 and July 2015. The scam revealed underlying fragility in Indian banks, in particular with respect to compliance, governance, and control.

The Bank of Baroda scam is a general term used for several abuses of the banks’ operations, whereas the Bank of Baroda forex scam is the most serious. The scale and intricacy of the scam made it a national story, as the probe uncovered the use of banking infrastructure to facilitate money laundering and malfeasance.

How the Bank of Baroda Scam Unfolded?

Fraudsters use the bank’s forex services to remit huge amounts of money abroad. They opened 59 current accounts at the Ashok Vihar branch in New Delhi using incomplete or fraudulent KYC documentation. Transactions were carried out by way of import bills for dry fruits and agricultural products. However, customs and import data revealed that no such goods had been imported.

The scam was preventable because of the very poor internal control at the bank. The branch, however, had a small number of resources to keep track of all these high-value transactions. Even though [we] were able to process high volumes of forex remittances that were out of the ordinary, no alarms were raised by branch staff or compliance units. This lack of scrutiny allowed fraudsters to exploit the system for an extended period.

Revealing the Bank of Baroda Scam 6000 Crore

The scam in the Bank of Baroda involved an unlawful transfer of ₹6,000 crore between July 2014 and July 2015. These transactions accounted for payments done for imports that never occurred. The fraud showed extreme operational flaws in the bank, as it did not try to verify whether these transactions existed or whether any valid shell companies were backing them.

These fraudulent remittances were then presented to the financial hubs of Hong Kong Dubai, places generally associated with money laundering shell companies. More than 400 companies received money, most of which did not have any actual business operations but only the purpose of serving as a front for money laundering.

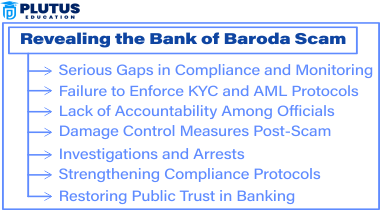

Serious Gaps in Compliance and Monitoring

The Bank of Baroda scam pointed to fundamental weaknesses in the compliance architecture as well as mechanisms of oversight that the bank had in place. Compliant mechanisms are designed to prevent fraud at critical levels, but there, the Bank failed to enforce even the most foundational norms. The Ashok Vihar branch, however, did not show any inadequacy, though the volumes of the remittances were much higher than usual.

Failure to Enforce KYC and AML Protocols

The fact that this scam was supported by non-observance of KYC (Know Your Customer) and AML (Anti Money Laundering) procedures shows the presence of various reports indicating the use of fake or partial documents for opening the documents. Irrespective of efforts at verifying the factual authenticity and legitimacy of the accounts and transactions, a considerable number of high monetary value transactions have been conducted. The bank has failed to monitor and track those accounts in suspicious behaviors. It is compulsory on the banking side under PMLA, as per law, to report any suspicious transaction to the Financial Intelligence Unit (FIU).

Lack of Accountability Among Officials

The fraud lay bare the lack of accountability across several levels of the bank. Senior officials ignored the red flags, while branch-level staff failed to carry out their duties effectively. This absence of responsibility facilitated cheating in the system with great ease.

Damage Control Measures Post-Scam

After the Bank of Baroda scam was exposed, the authorities acted very rapidly to reduce the effects that this would have on the people and to have full confidence in the bank. Because of all these weaknesses and when this fraud exploited them, various measures had to be adopted in order not to allow such attacks again in the future.

Investigations and Arrests

The fraud had led to an investigation by the CBI, ED, and RBI. The investigations depicted the extent of the fraud and the individuals who were guilty. Several arrests were made, such as the officials in the banks who colluded with them on the scam or were simply unaware of their duties.

Compliance Protocols ended

The RBI introduced new guidelines and regulations for foreign exchange transactions to provide better protection and monitoring. Banks were given the high task of improving their KYC controls, strengthening their internal controls, and using technology to monitor high-net-worth transactions.

Rebuilding Public Confidence in Banking

The government and regulatory bodies made efforts to restore public confidence in the banking system. This included strengthened supervision of public sector banks and the implementation of reforms aimed at improving governance and accountability.

Red Flags and Warnings Ignored

Bank of Baroda foreign exchange scam reeked with red signals either missed or avoided. The same red flags averted the crime if acted appropriately at the opportune time.

A glaring red flag was the fact that large numbers of forex transactions were being done at the Ashok Vihar branch. This branch, which had meager resources and no previous experience of dealing with such large remittances, suddenly saw transactions worth ₹6,000 crore in a single year. Such a dramatic increase was, quite frankly, an alarm bell that should have rung in the bank’s compliance departments.

A further red flag was the lack of or falsified account holder documentation. In the 59 accounts used in the fraud, a number of the accounts were opened with false identities. Proper verification of these papers would have unearthed the scam at a very early stage.

The Number Game: Breaking Down the Scam

The Bank of Baroda scam of 6000 crore involved a complex network of fraudulent transactions carried out over a year. The funds were moved out to more than 400 shell companies in Hong Kong and Dubai, all of which were set up only to enable such illicit transfers. The magnitude of the fraud demonstrated the weaknesses of India’s banking system, inter alia, concerning fx and trade finance.

Bank of Baroda Scam FAQs

What was the Bank of Baroda scam?

Implicated illegal transfer of HKD 6,000 crore to Hong Kong and Dubai conducted via fraudulent currency swap transactions has taken place in the Bank of Baroda scam. These transactions were deceptively reported as payments for goods that did not exist.

What is the Bank of Baroda forex scam?

The Bank of Baroda forex scam relates to the misutilization of the foreign exchange conduits for money laundering. Fraudsters routed funds through shell companies under the guise of import payments.

What amount of money was part of the Bank of Baroda scam?

The Bank of Baroda scam of 6000 crore involved illegal remittances worth ₹6,000 crore between July 2014 and July 2015.

What gaps were exposed by the Bank of Baroda scams?

The fraud highlighted the critical weaknesses in compliance, KYC regulations, and surveillance systems. It exposed the absence of strong internal controls and the bank officials’ negligence.

What actions were taken after the scam?

Authorities started investigations, made several arrests, and imposed tighter measures for forex transactions. The Reserve Bank of India, in its effort to enhance governance and supervision of banks, took some steps.