Banking institutions form the core of any economy as they collect deposits, distribute credits, and manage wealth. These financial institutions play a critical role in ensuring financial stability, economic growth, and public trust in the monetary system. In India, banking institutions have evolved to be very diversified with services to individual, business, and government units. This article deals with what are banking institutions, their types, and their objectives, at least in the Indian scenario. Knowing about the role and functions of banking institutions helps us know how important these are in making a prosperous economy.

What is Banking Institutions?

Banking institutions are organizations that deal with money and provide financial services such as accepting deposits, granting loans, and facilitating transactions. These institutions act as intermediaries between savers and borrowers, ensuring efficient capital flow within the economy. An example is a savings account with a bank, where the institution accepts deposits and provides interest in return, which is a basic example of how banking institutions work.

Types of Banking Institutions in India

Banking institutions in India are diverse, catering to the financial needs of different sectors and individuals. They are broadly classified into the following categories:

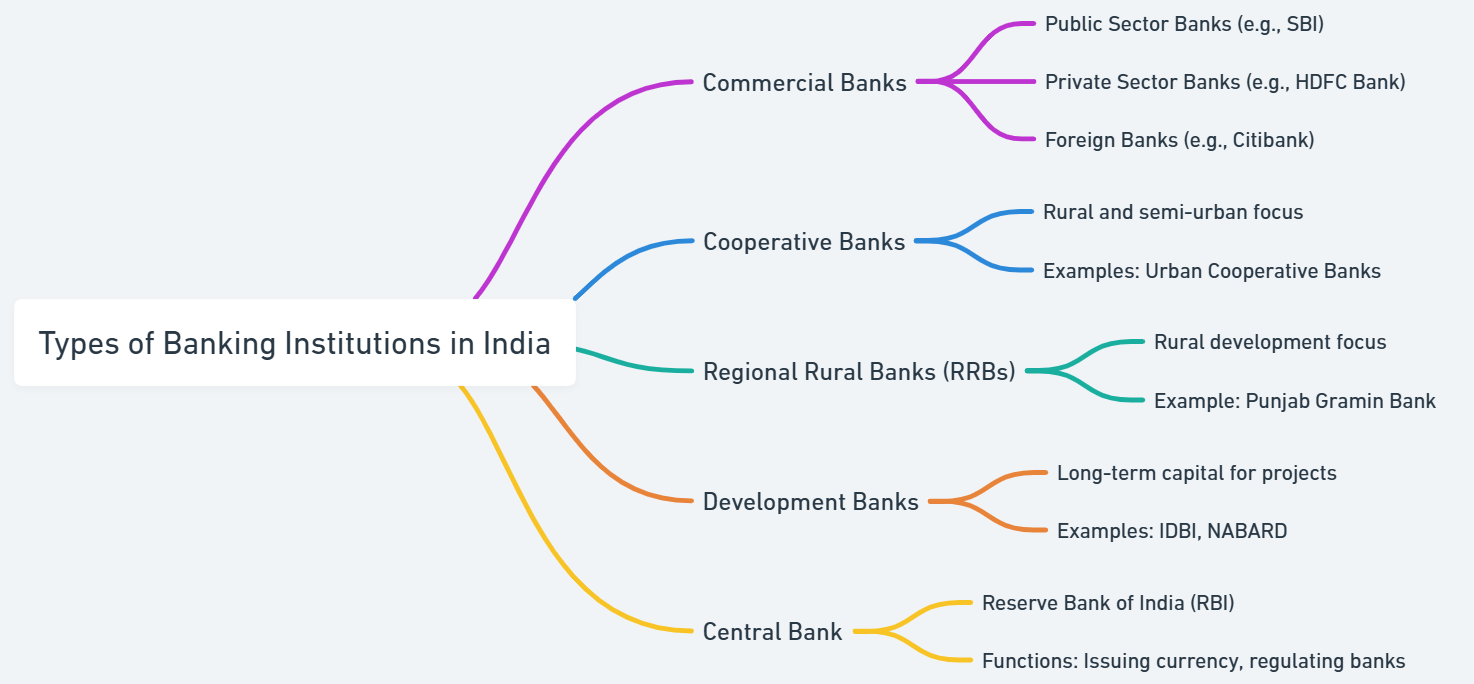

Commercial Banks

Commercial banks are the largest banking institutions in India, focused on earning profits while providing essential financial services. They offer loans, accept deposits, and facilitate foreign exchange to support businesses and individuals. These banks also help in economic growth by offering safe investment options like mutual funds and fixed deposits. For example, people use their services to save money, take loans, or manage international trade smoothly.

Commercial banks have three main types: Public Sector Banks (e.g., SBI), owned by the government; Private Sector Banks (e.g., HDFC), run by private entities; and Foreign Banks (e.g., Citibank), headquartered abroad but operating in India. Their functions include providing credit, enabling international trade, and offering secure investment products. These services make them a crucial part of India’s financial system.

Cooperative Banks

Cooperative banks focus on helping people in rural and semi-urban areas. They operate on a cooperative model, where members are both owners and customers. These banks support agriculture, small businesses, and housing by offering financial assistance tailored to local needs. Their goal is to promote community welfare rather than just profit-making, making them a vital part of the rural economy.

Cooperative banks are smaller in scale compared to commercial banks and cater to specific needs like agriculture and housing. They provide loans at lower interest rates, making them affordable for farmers and small business owners. Examples include Primary Agricultural Credit Societies and Urban Cooperative Banks, which focus on improving local development and supporting the livelihood of rural communities.

Regional Rural Banks (RRBs)

Regional Rural Banks (RRBs) focus on promoting rural development and supporting small communities. They combine the features of commercial and cooperative banks to serve the needs of rural areas. RRBs provide essential financial services to small farmers, artisans, and rural entrepreneurs, helping them grow and contribute to the rural economy.

RRBs aim to provide low-interest loans to support agriculture, small businesses, and rural industries. Their affordable credit helps rural people build sustainable livelihoods and develop local economies. For example, Punjab Gramin Bank is a well-known RRB that focuses on uplifting rural communities through financial assistance.

Development Banks

Development banks are financial institutions that provide long-term capital to support large-scale economic activities. They focus on funding infrastructure projects, industrial development, and other initiatives that boost the economy. These banks help create jobs, improve public services, and strengthen industries, making them essential for a country’s progress and development.

Development banks play a key role in sectors like agriculture and industry. For instance, the Industrial Development Bank of India (IDBI) supports industrial growth, while the National Bank for Agriculture and Rural Development (NABARD) helps improve agriculture and rural development. These banks provide loans and financial support to ensure sustainable economic growth.

Central Bank

The Reserve Bank of India (RBI) is the central bank that oversees and manages the country’s banking system. It ensures financial stability by regulating all banking institutions in India. The RBI plays a crucial role in maintaining trust in the banking system and supporting the economy through its policies and actions.

The RBI issues and manages the currency in India, ensuring adequate money supply. It controls the country’s monetary policy to manage inflation and economic growth. Additionally, it supervises and regulates other banks to ensure they operate efficiently and follow rules. These functions make the RBI vital to India’s financial system.

Objective of Banking Institutions in India

Banks play a crucial role in driving economic growth by mobilizing savings, providing credit, promoting financial inclusion, and ensuring stability in the financial system. They support individuals, businesses, and the government in achieving economic development goals.

- Mobilization of Savings: Banks encourage individuals and businesses to save money, ensuring it is productively used for loans and investments. Increased national savings rate. Availability of funds for economic development.

- Credit Facilitation: Banks provide loans to various sectors like agriculture, industry, and services. This helps promote entrepreneurship and economic activity. Types of Loans: Short-term loans for working capital. Long-term loans for infrastructure projects.

- Financial Inclusion: One of the key objectives is to bring unbanked sections of society into the formal financial system. Initiatives are opening zero-balance accounts under the Pradhan Mantri Jan Dhan Yojana (PMJDY). Offering microfinance services to rural and semi-urban areas.

- Economic Growth: Banks support the government’s economic policies by funding public infrastructure projects and implementing monetary measures. The role is financing national development projects like roads and power plants. Supporting small businesses and startups.

- Ensuring Stability: By regulating credit flow and monitoring inflation, banks help maintain economic stability. Methods: Controlling money supply through interest rates. Monitoring financial institutions under the RBI’s guidance.

Banking Institutions FAQs

What are banking institutions?

Banking institutions are organizations that provide financial services like accepting deposits, granting loans, and facilitating transactions.

What are the types of banking institutions in India?

Types include commercial banks, cooperative banks, regional rural banks, development banks, specialized banks, and the central bank.

What is the objective of banking institutions?

Their objectives include mobilizing savings, facilitating credit, promoting financial inclusion, ensuring economic growth, and maintaining stability.

What is the role of the Reserve Bank of India?

The RBI acts as India’s central bank, regulating monetary policy, supervising banking institutions, and maintaining financial stability.

What is the National Institute of Bank Management?

It is an institute that provides training and research in banking and finance, helping improve the efficiency of banking institutions.