The most basic terms in accounting can, therefore, become very important and useful in business or finance. Accounting is the backbone of any organization, providing it with insight into its financial health, performance, and even position. Accounting terms form the base of this system; they help one make sense of financial statements, reports, and transactions. Whether you own a business, aspire to become an accountant, or just study for a student, these terms are invaluable as they help in the communication and decision-making process of finance.

Basic Terms Used in Accounting

There exist several basic terms used in accounting that build on to form the bricks of financial analysis and reporting. These are major concepts that form the very foundation of how the accounting process records, classifies and sums up the transactions to obtain useful financial information.

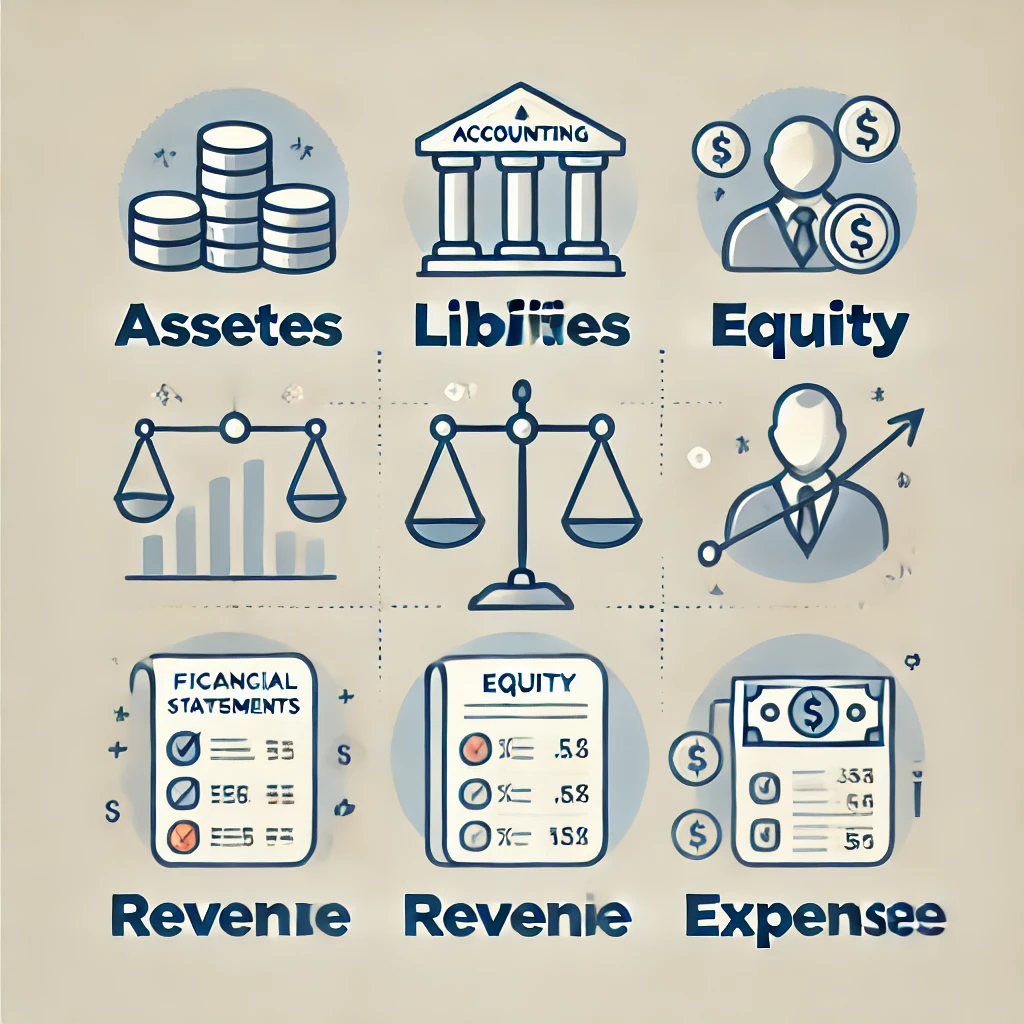

Assets

Assets Resources owned by a business with economic value and expected future benefits. They can be broadly categorized as

- Current Assets: These are the assets to be converted into cash within one year, comprising cash, accounts receivable, and inventory.

- Non-Current Assets: Those assets that do not have a short-term existence. These may include property, equipment, and patents for example.

Liabilities

Liabilities are obligations or debts that business owes to other parties. Like assets, liabilities also have two categories:

- Current Liabilities: These include liabilities that are currently due and have a period of less than one year: this is covered by all loans with less than one year term and accounts payable.

- Non-Current Liabilities: Long term debt such as bonds payable or mortgages that matures after a year.

Equity

Equity is the residual interest in the assets of a business after deducting liabilities. It represents the ownership interest held by shareholders or the owner in a business.

Revenue

Revenue is the total amount of money earned by a business from its operations, such as sales of goods or services. It is often referred to as “sales” or “income.”

Expenses

Expenses are the costs incurred by a business in the process of earning revenue. Common types of expenses include wages, rent, utilities, and the cost of goods sold.

Profit

Profit, also known as net income, is the amount left after all expenses have been subtracted from revenue. It indicates the financial success of a business.

Debits and Credits

These are basic terms that the double-entry accounting system uses. A debit increases an asset or an expense account, while a credit increases a liability, revenue, or equity account.

These basic accounting terms help one to trace transactions, then ensure keeping records accurate, plus being able to produce meaningful financial statements like a balance sheet, income statements, and cash flow statements.

What Is Accounting?

Accounting refers to the process of systematic recording, classifying, summarizing, and analyzing of financial transactions to provide useful information for decision-making purposes. It is said to be the “language of business” because it communicates the financial performance and position of an organization to such stakeholders as investors, creditors, and management. Functions of Accounting:

- Recording: Accounting involves documenting all financial transactions of a business in chronological order. This is often done using journals and ledgers.

- Classifying: Transactions are categorized into specific accounts (e.g., assets, liabilities, revenues) for better organization and clarity.

- Summarizing: At regular intervals, such as monthly or annually, these records are summarized into financial statements, including balance sheets and income statements.

- Analyzing and Interpreting: Accounting provides insight into trends and performance through analysis, helping management and other stakeholders make informed decisions.

The core objective of accounting is to have available and of sufficient quality financial information for making effective decisions and for compliance with legal and regulatory requirements.

What Are Three Fundamental Concepts Of Accounting?

The three fundamental concepts of accounting are principles that guide how financial transactions are recorded and reported. These concepts ensure consistency, accuracy, and reliability in financial reporting.

The Accrual Concept

Under the accrual concept, revenues are recorded and recognized as earned, while expenses, whichever they relate to, are recorded when incurred, irrespective of when the cash is exchanged. This method gives a fairer idea about the real financial status of the company.

For example, suppose a company sells its services in December but receives the money in January, then its revenue will be recorded in December under the accrual concept.

The Going Concern Concept

The going concern concept assumes that a business will go on operating in eternity with no impending liquidation or closing of the business. This will directly influence the valuation of assets and liabilities because the business is believed to continue generating revenue and hence give it some value.

For example, a business purchasing a piece of equipment assumes that it will be there to utilize for a long time and not to sell off straight away.

The Consistency Concept

This concept ensures the business uses consistent accounting methods and procedures in different periods. It gives comparability of financial statements over time.

Example: If a company depreciates one asset through the straight-line method, then for subsequent fiscal years, it should again use the same approach unless a change is warranted and disclosed appropriately.

What Are The Basics Of Accounting?

Basic accounting implies knowledge about how financial transactions are captured and reported in order to determine a clear picture of the financial position of a business. Accounting relies on a number of prime principles and procedures that assure accuracy and openness.

Double-Entry System

The double-entry system, of course, keeps the accounting equation in perfect balance because every transaction does affect at least two accounts. Hence, it posts a corresponding debit and credit.

Financial Statements

Some of the key financial statements that accounting yields are:

The balance sheet reflects the position of the finances at any point in time regarding the assets, liabilities, and equity of a business.

- Income Statement: Also referred to as a profit and loss statement, it reflects the revenues and expenses of the company over a given period, thus culminating in net profit or loss.

- Cash Flow Statement: This statement provides information on the inflow and outflow of cash of the business, to estimate liquidity and cash management.

Accounting Cycle

Accounting Cycle refers to the step-by-step process undertaken for identifying, recording, and summarizing financial transactions as:

Step 1: Identify and analyze financial transactions.

Step 2: Record transactions in journals using debits and credits

Step 3: Post journal entries to ledger accounts

Step 4: Draw up a trial balance to ensure all entries are balanced.

Step 5: Generate financial statements from the trial balance.

Thus, using the accounting cycle businesses would be able to post correct financial statements that have been under regulatory standards.

What Are the Fundamental Accounting Terms?

The fundamental accounting terms are essential for understanding how financial transactions are recorded, classified, and interpreted. These terms are widely used in both manual and computerized accounting systems.

Journal

A journal is often referred to as the primary book of accounting. Wherein all financial transactions are first recorded in chronological order. It lies at the very heart of the accounting cycle, which automatically becomes the “book of original entry,” where each transaction is systematically noted as it occurs. Journals help in maintaining actual records of financial positions. Since they provide information about the date, description, debit and credit amounts, and accounts involved in a particular transaction.

Ledger

A ledger is considered one of the most essential components of the accounting system because all transactions recorded in the journal will be classified and summarized here. It can also be known as the “book of final entry.” In a ledger, accounts are divided into various groups or accounts, showing an important aspect of the business, such as assets, liabilities, equity, revenues, and expenses. The ledger is therefore a tool that is used to track, over time, the balance of each account and provide business owners with the opportunity to assess their financial well-being. Thus, prepare crucial financial statements such as the balance sheet and income statement.

Trial Balance

A trial balance is a financial report that provides an overview of all ledger accounts, alongside their respective balances, at one point in time. It is a tool used by accountants to ensure that the double-entry bookkeeping system is accurate. This means that the total amount of debits equals the total amount of credits. This brings us to the trial balance, which represents one final check before the preparation of more formal financial statements such as the balance sheet and income statement.

Debit and Credit

The debits and credits are two of the primary concepts of accounting in recording transactions in the double-entry bookkeeping system. Every account is impacted with at least a debit on one hand and a credit on the other hand. This feature ensures that the accounting equation Assets = Liabilities + Equity is, as a result, preserved. Thus, the debits and credits are two opposed representations on the sides of accounts, which makes record keeping accurate.

- Debit: An entry on the left side of an account that increases assets or expenses and decreases liabilities, revenue, or equity.

- Credit: An entry on the right side of an account that increases liabilities, revenue, or equity and decreases assets or expenses.

Depreciation

Depreciation is the cost allocation process that spreads out the expense of a long-term asset over its useful life. This simply reflects the wear and tear or obsolescence of an asset over time.

Conclusion

With this in mind, mastering basic accounting terms is important for those who engage in business, finance, or accounting services. Understanding the use of the terms will therefore lead to an understanding of a company’s financial health, making informed business decisions. These ensure adherence to the proper understanding of financial regulations. Terms start with assets and liabilities to equity and profit. Therefore, understanding the basic core concepts of accounting is quite beneficial to an individual. It concerns his or her financial literacy and management or interpretation of financial information.

Basic Accounting Terms FAQs

What is accounting?

Accounting is the systematic process of recording, classifying, summarizing, and analyzing financial transactions to provide useful financial information.

What are the three fundamental concepts of accounting?

The three fundamental concepts are the accrual concept, going concern concept, and consistency concept.

What are the basics of accounting?

The basics of accounting include the double-entry system, financial statements (balance sheet, income statement, and cash flow statement), and the accounting cycle.

What is a ledger in accounting?

A ledger is a collection of accounts where financial transactions are summarized after being recorded in the journal.

What is depreciation in accounting?

Depreciation is the process of allocating the cost of a tangible asset over its useful life. It reflects the decline in value of the asset due to wear and tear or obsolescence.