Cost categorization is critical to financial planning, strategic pricing, and resource allocation. It offers a systematic method of grouping expenses so that companies can determine which costs are fixed, variable, and minimized or optimized. When companies understand the structure of their costs, they have more control over operations, make better financial decisions, and improve overall profitability. Whether getting ready for a cost audit, planning a budget, or overseeing a new project, knowing cost classification inside and out puts you ahead of the game.

What Is Cost?

Cost is the total expenditure incurred by a business to generate goods or services, covering everything from raw materials and labor to indirect overheads like rent and utility bills. It includes both tangible and intangible resources that are consumed during the production process. In accounting terms, cost is not just a number—it reflects the efficiency and effectiveness of resource use. Understanding cost helps a business assess profitability, manage working capital, and support financial reporting, taxation, and compliance functions.

Types of Cost in Accounting

Current identification and segmentation of different cost types are central to effective financial management. They impact profitability, production planning, and decision making differently

1. Fixed Costs

Fixed costs don’t vary irrespective of the volume of production or sales. They are incurred even when a firm produces nothing, like factory rental, full-time employees’ wages, or insurance premiums. Fixed costs keep the business infrastructure functioning, but must be managed well since they constrain flexibility in off-peak periods.

2. Variable Costs

Variable costs increase or decrease directly proportional to the production quantity. Examples of variable costs are raw materials, electricity used in equipment, and packaging. Variable costs increase with more production, which makes them easy to manage when there is little output. They play a crucial role in determining the contribution margin and the breakeven poin..

3. Semi-Variable Costs

Also referred to as mixed costs, semi-variable costs have a fixed and a variable element. For instance, the sales manager will have a fixed salary plus sales commissions (variable). They are more difficult to predict and control but provide companies with cost flexibility according to performance and size.

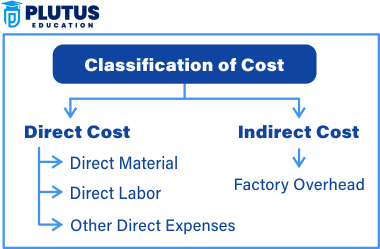

4. Direct Costs

Direct costs are allocated to individual products or services. Examples of these costs are raw materials, labor involved in manufacturing, and components involved in production. Direct cost measurement allows businesses to calculate product-level profitability, establish optimal prices for selling, and analyze cost efficiency by product line.

5. Indirect Costs

Indirect costs, or overheads, are not directly linked to a single cost object but are necessary to run the overall operation. Examples include HR department expenses, utility bills, and depreciation on equipment. These costs are typically allocated across departments and products using cost drivers or activity-based costing methods.

Classification of Cost by Behavior

Cost behavior analysis helps predict how costs will change with different activity levels. This classification is beneficial for cost-volume-profit analysis, budgeting, and operational planning.

- Fixed Costs: They remain constant irrespective of business output. These are usually recurring, like lease payments or insurance premiums, and are crucial for long-term planning.

- Variable Costs: It changes based on production volume. More units produced means more materials are consumed, and energy usage is higher.

- Mixed Costs: They fluctuate but not proportionally. A telephone bill may have a fixed monthly rental and a usage charge based on calls made.

By understanding cost behavior, businesses can better anticipate how expenses change with scaling operations, which is vital during expansion or downturns.

Classification of Cost by Function

Functional classification organizes costs based on the part of the business process they support. This method improves transparency and control over departmental spending.

- Production Costs: They are directly associated with creating goods or services, including labor, raw materials, and factory overhead.

- Administrative Costs: It refers to the general operations of the business, like office staff salaries, audit fees, and legal expenses.

- Selling & Distribution Costs: It includes marketing, sales commissions, transportation, and customer service expenses.

- Research & Development Costs: They cover product innovation, testing, and experimentation. These are critical for tech, pharma, or consumer goods companies.

Functional classification is widely used in managerial accounting to assign costs to cost centers and prepare internal financial reports.

Classification of Cost by Nature

Costs by nature categorize expenses based on what the business spends money on. This is one of the most basic and widely used methods of classification.

- Material Costs include all raw materials and inputs required for production.

- Labor Costs refer to wages, benefits, and allowances given to employees involved in manufacturing or operations.

- Expenses/Overheads include non-direct costs like utilities, rent, fuel, and maintenance.

This classification is helpful when preparing cost sheets, financial statements, or conducting a cost audit.

Classification by Traceability

This classification method distinguishes between costs directly attributed to a product or service and those that cannot.

- Direct Costs: Directly linked to a product (e.g., steel for a car).

- Indirect Costs: Shared costs like electricity or management salaries that support multiple products or functions.

Traceability classification enables businesses to assign expenses appropriately and plays a key role in activity-based costing (ABC) and standard costing systems.

Classification of Costs Based on Time

Time-based classification is used in planning and long-term investment decision-making.

- Capital Costs are one-time investments in buildings, land, or machinery.

- Revenue Costs, such as maintenance or inventory, are operational and recurring.

- Deferred Costs are incurred now but recognized in future accounting periods (e.g., prepaid insurance).

This grouping helps one to comprehend the cost life cycle and improve long-term budgeting and resource planning.

Objectives of Cost Classification

The knowledge of the rationale behind the classification of costs is crucial to business managers and business students. The chief aim is to make it possible for organizations to better control their costs and make appropriate choices . Cost classification serves to:

- Effective budgeting and forecasting: Through knowledge of fixed or variable costs, companies can more accurately forecast future expenses.

- Effective cost control: Managers can detect areas of high cost and address them.

- Strategic pricing: Helps businesses to price according to cost structure to ensure competitiveness and profitability.

- Improved financial reporting: Cost classification based on a structured format enhances the transparency and reliability of financial statements.

- Resource allocation: Assists in guiding financial and human resources to those most profitable areas of the business.

As such, goals are kept to heart; cost classification is integral to strategic financial planning.

Role of Cost Behavior in Decision Making

Cost behavior gives useful insight into how costs react to varying business activities. For instance, when expanding production, one would want to know which costs would rise and which would stay constant to estimate cash flows properly. It also helps to set proper prices and maintain sustainable profit margins. Failing to do this can cause firms to overestimate their costs, leading to pricing mistakes and monetary losses.

Real-Life Examples of Cost Classification

Take the example of a bakery business:

- Direct Cost: Eggs and flour used in baking

- Indirect Cost: Electricity bills for light and refrigeration

- Fixed Cost: Bakery shop rent for a month

- Variable Cost: Sugar and cream used per cake

- Semi-variable Cost: Salaries of staff with sales-based incentives

Understanding and applying these classifications helps businesses identify where money is going and how to improve cost efficiency without compromising output quality.

How Cost Classification Impacts Profitability?

Correctly classifying costs allows a business to manage resources effectively and price products appropriately. It helps determine the contribution margin, establish target costing, and monitor department-wise performance. Businesses that understand their fixed and variable costs can also calculate the break-even point more accurately and make more strategic decisions about scaling operations or entering new markets.

Practical Benefits of Cost Classification

- Enables detailed cost analysis and identification of inefficiencies

- Supports budget formulation and variance analysis

- Aids in tax planning and cost allocation to departments

- Facilitates better internal audits and controls

- Helps in determining project viability and ROI

These benefits collectively lead to a stronger financial structure and support long-term business sustainability.

Classification Of Cost FAQs

Q1. What are fixed and variable costs?

Fixed costs don’t change with production volume. Variable costs increase or decrease with changes in output levels.

Q2. Why is cost classification significant?

It helps businesses control costs, forecast expenses, determine selling prices, and improve financial decision-making.

Q3. What are indirect costs?

Indirect costs are not tied to a specific product or service and include general expenses like office rent and managerial salaries.

Q4. What is cost classification by function?

This group’s costs are based on business operations such as production, administration, sales, and R&D.

Q5. How does cost behavior influence decision-making?

It predicts how costs will change as business activities fluctuate, allowing for better budgeting and profit planning.