The CMA Subjects will allow the prospective Certified Management Accountants to understand and apply the knowledge and skills needed in performing financial management, strategic analysis, and decision-making. The US CMA, which stands for Certified Management Accountant, is administered by the Institute of Management Accountants in two comprehensive parts: the first covering the essentials of management accounting and the second in finance strategy. Different topics compose each segment, which challenges the finance aptitude of a candidate in financial accounting, budgeting, cost management, and strategic financial decision-making.

US CMA Subjects

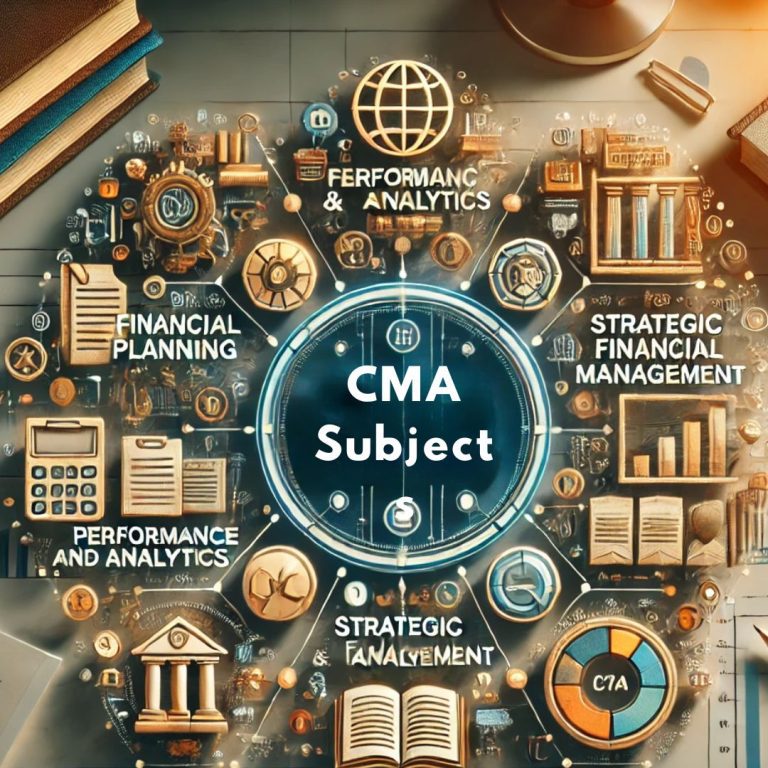

The syllabus for Certified Management Accountant (CMA) are divided into two main parts: Part 1: Financial Planning, Performance, and Analytics and Part 2: Strategic Financial Management. Part 1 covers the following topics: financial reporting, cost management, budgeting, performance evaluation, and data analytics, while Part 2 is concerned with financial decision-making, risk management, corporate finance, investment decisions, and professional ethics. Each subject is so structured to endow the candidate with the knowledge to analyze financial data, understand business performance, and make effective strategic decisions within a real business world.

- Financial Reporting: Covers the preparation and interpretation of financial statements.

- Cost Management: Focuses on costing techniques and cost control measures.

- Planning and Budgeting: Involves preparing budgets and forecasts to guide financial planning.

- Internal Controls: Discusses the framework for risk management and fraud prevention.

- Strategic Financial Management: Covers investment decisions, corporate finance, and risk management.

Mastering these subjects equips candidates with the analytical tools and technical knowledge required for high-level positions in management accounting.

US CMA Part 1: Financial Planning, Performance & Analytics

Key concepts of the US CMA exam include financial planning, cost management, and analytics. Fundamentally, part 1 of the exam essentially builds the foundation of financial reporting and analysis knowledge, along with applying such principles in business.

External Financial Reporting Decisions

- Financial reporting frameworks, such as GAAP and IFRS.

- Prepare financial statements, including income statements, balance sheets, and cash flow statements.

- Analysis of financial statements to assess profitability, liquidity, and solvency.

Planning, Budgeting, and Forecasting

- Techniques for preparing budgets, financial forecasts, and variance analysis.

- Understanding of operational and capital budgeting.

- Integration of strategic and tactical planning processes.

Performance Management

- Key performance indicators (KPIs) and balanced scorecard approaches.

- Variance analysis to compare actual results with budgeted figures.

- Performance measurement at different organizational levels.

Cost Management

- Concepts of costing include job order, process, and activity-based costing.

- Cost behaviour and classification (fixed, variable, and mixed costs).

- Methods of cost control and reduction.

Internal Controls

- Risk management frameworks and internal controls.

- Fraud prevention techniques.

- Compliance with regulatory requirements and ethical standards.

| Topics | Marks |

|---|---|

| External Financial Reporting Decisions | 15% |

| Planning, Budgeting, and Forecasting | 20% |

| Performance Management | 20% |

| Cost Management | 15% |

| Internal Controls | 15% |

| Technology and Analytics | 15% |

| Total | 100% |

US CMA Part 2: Strategic Financial Management

The second part of the CMA exam focuses on strategic financial management, corporate finance, decision analysis, and risk management. It helps candidates gain expertise in applying financial principles to guide business strategy and growth.

Financial Statement Analysis

- Advanced techniques for analyzing financial statements.

- Interpretation of ratios, trends, and comparative data.

- Understanding how financial performance impacts business strategy.

Corporate Finance

- Key capital budgeting concepts include net present value (NPV) and internal rate of return (IRR).

- Financing decisions, capital structure, and cost of capital.

- Dividend policy and corporate governance issues.

Decision Analysis

- Techniques for evaluating business decisions using cost-volume-profit (CVP) analysis.

- Marginal analysis and relevant costs for decision-making.

- Pricing strategies, including market-based and cost-based pricing.

Risk Management

- Identification and management of financial risks.

- Tools for managing currency risk, interest rate risk, and market risk.

- Use of financial derivatives such as options, futures, and swaps.

Investment Decisions

- Evaluation of long-term investments using capital budgeting techniques.

- Understanding mergers, acquisitions, and corporate restructuring.

- Strategic financial decisions aimed at business expansion and profitability.

| Topics | Marks |

|---|---|

| Financial Statement Analysis | 20% |

| Corporate Finance | 20% |

| Decision Analysis | 25% |

| Risk Management | 10% |

| Investment Decisions | 10% |

| Professional Ethics | 15% |

| Total | 100% |

Conclusion

The CMA Subjects ensure that the candidate takes well-rounded preparations toward the business of management accounting and finance careers. Therefore, the exam program extensively covers financial planning, cost management, strategic decision-making, and corporate finance. This will make candidates available with the learned knowledge to support them in their high-level roles concerning the financial management of an organization. The exam format in two parts guarantees that candidates are well sharpened on both technical and strategic skills required for making informed decisions related to the complex financial issues within the global business environment.

CMA Subjects FAQs

What does a CMA course cover?

The CMA course deals with subjects such as financial reporting, cost management, planning and budgeting, performance management, corporate finance, and risk management.

How many parts are there in the CMA exam?

The CMA exam consists of two parts. Part 1 is related to financial planning and performance, whereas Part 2 comprises strategic financial management.

What is cost management about in the CMA exam?

The cost management segment discusses job order costing, process costing, cost behavior analysis and techniques for controlling and reducing cost.

How much time will it take to prepare for each segment of the CMA exam?

It normally takes 3 to 6 months for each part, depending on your study pace and work schedule.

What skills do CMA subjects focus on developing?

CMA subjects focus on developing financial analysis, decision-making, cost management, strategic planning, and risk management skills.