Every business functions with funds and ultimately survives by growth. Companies raise capital by taking funds from various sources: debt, equity, and retained earnings. The components of cost of capital mean the multiple sources of financing and the expenses involved in raising them. It encapsulates debt cost, equity cost, and other avenues of financing, which together constitute the total cost of acquiring funds. Therefore, companies analyze capital costs to effectively choose where to make their investments and how to fund their activities while ensuring that such decisions are profitable.

The cost of capital is significant in financial management. It allows firms to evaluate projects, profit potentials, and long-term financial decisions. So, an improper estimation of the cost of capital may result in faulty financial planning and, hence, lower profitability and growth. Each business must understand the components of the cost of capital if it wants to work its capital structure to an optimal position.

Cost of Capital Definition

Cost of Capital is the price a corporate body pays to raise funds for business activities. The return the investors expect to earn from their investments in the particular company is the cost of capital. If the company cannot generate returns equal to or more than the cost of capital, it becomes financially unviable.

Cost of capital, therefore, becomes an essential factor for the company to decide whether or not an investment is to be pursued. The components of cost of capital include debt, equity, and preference shares, which all have their costs. Each element is vital for decision-making.

Funds can be raised by the company either from equity shareholders or debenture holders or through banks or retained earnings. All these sources of capital bear costs, thereby influencing the performance of the company financially. The cost of capital, if calculated and managed, can assist the companies in making profitable investments.

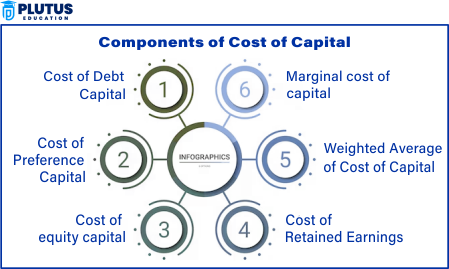

Components of Cost of Capital

The several components involved in the cost of capital. Each financing source contributes differently toward the computation of the total cost. The components of the cost of capital are given below:

Cost of Debt

Debt financing means loans, bonds and debentures. The cost of debt is the interest paid by a company on the borrowed funds. Debt financing is cheaper than equity since interest expense is tax-deductible, but a high debt burden increases financial risk.

Cost of Debt= Interest paid *( 1- tax rate)/Total debt

Cost of Equity

Equity financing means issuing shares with investments. The cost of equity indicates the return shareholders expect. The cost of equity can be computed as

Cost of Equity= Risk-free return + Beta(Market Return- Risk-Free Return)

Using the Capital Asset Pricing Model (CAPM). Higher risk increases the cost of equity and hinders financial performance.

Cost of Preference Shares

They have fixed dividends to shareholders. The formula to calculate the cost of preference shares

Cost of Preference Shares= Dividend/ Market price per share

Preference shares are riskier than debt but cheaper than equity. Companies use them to balance their capital structure.

Cost of Retained Earnings

Retained earnings are profits reinvested in the business instead of distributed as dividends. There may not be any expense for them, but opportunity cost is associated with retained earnings as shareholders expect returns.

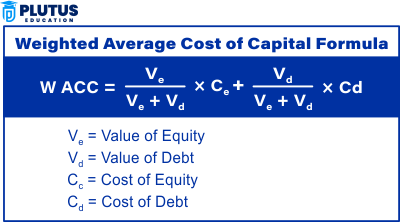

Weighted Average Cost of Capital (WACC)

WACC is the mean cost of the various capital sources, and the following formula can calculate it:

The lesser the WACC, the more financial efficiency is gained, and the more profitable the investments are.

Specific Cost of Capital

Each finance component has its own cost, termed the specific cost of capital. Companies compute their particular costs to find their effects on the comprehensive capital cost. This additional cost is incurred when raising fresh capital. Thus, the capital costs become high beyond a certain fundraising level.

Cost of Convertible Securities

Convertible securities provide investors the option to convert their holdings into equity. They generally have lower interest rates but cause higher dilution risk to shareholders.

Importance of Cost of Capital

Companies cannot make sound financial decisions without the cost of capital. It affects investment decisions, business expansion, and economic health.

Helps in Making Investment Decisions

The cost of capital guides companies in undertaking ventures for new projects. If the returns from a project exceed the cost of that capital, investment would likely occur; otherwise, no investment would occur. For example, if a company requires capital at 10% to support itself and a project has a return of rated 15%, this is a profitable investment.

Capital Budgeting

Cost of capital-based capital budgeting decisions. Systems like Net Present Value (NPV) and Internal Rate of Return (IRR) are now used in businesses to set investments with returns higher than the cost of capital.

Capital Structure Determination

The weighages between debt and equity depend on the cost of capital. An optimal capital structure minimises costs and maximises returns. Debt becomes cheaper than equity; borrowing becomes more affordable depending on how accessible it is to companies.

Measure of Financial Performance

The performance is measured by comparing the return on investment (ROI) to the cost of capital. Value is created if ROI exceeds the cost of capital; value is destroyed if it does not.

Defines Dividend Policy

The cost of capital determines the firm dividend policy. Costly capital meant that possible earnings retainment was higher than prior dividends’ costs, which would be retained for growth.

Relevance to ACCA Syllabus

The cost of capital is crucial in ACCA’s Financial Management (FM) and Advanced Financial Management (AFM) exams. It determines investment feasibility, capital structure decisions, and risk assessment. Understanding the cost of capital helps in strategic decision-making related to mergers, acquisitions, and financing options.

Components of Cost of Capital ACCA Questions

- Which component is NOT included when calculating a company’s Weighted Average Cost of Capital (WACC)?

A) Cost of Equity

B) Cost of Debt

C) Cost of Retained Earnings

D) Cost of Goods Sold

Ans: D) Cost of Goods Sold - Why is the cost of capital important in financial management?

A) It helps determine the company’s tax obligations

B) It acts as a benchmark for investment decisions

C) It determines the company’s daily cash flows

D) It is used only for calculating stock dividends

Ans: B) It acts as a benchmark for investment decisions - What is the most common method used to estimate the cost of equity?

A) Gordon Growth Model

B) CAPM (Capital Asset Pricing Model)

C) Cost-Plus Pricing Model

D) IRR Method

Ans: B) CAPM (Capital Asset Pricing Model) - Which of the following would lower a company’s WACC?

A) Increase in market interest rates

B) Increase in debt financing at a lower cost than equity

C) Decrease in retained earnings

D) Increase in equity financing

Ans: B) Increase in debt financing at a lower cost than equity - How does a higher WACC impact a company’s investment decisions?

A) More projects will be accepted

B) The company will issue more equity

C) Investment opportunities become less attractive

D) The company’s profits increase

Ans: C) Investment opportunities become less attractive

Relevance to US CMA Syllabus

The topic of cost of capital is an integral part of the US CMA syllabus, particularly in the Strategic Financial Management section. It helps evaluate investment decisions, assess financing strategies, and optimize the capital structure.

Components of Cost of Capital US CMAQuestions

- Which formula represents the cost of preferred stock?

A) Dividend per share / Market price per share

B) Dividend per share / Earnings per share

C) Market price per share / Dividend per share

D) Net income / Equity

Ans: A) Dividend per share / Market price per share - What happens when a company raises funds through debt rather than equity?

A) WACC decreases if the cost of debt is lower than the cost of equity

B) WACC increases regardless of debt cost

C) Cost of capital remains unchanged

D) The company faces no risk from leverage

Ans: A) WACC decreases if the cost of debt is lower than the cost of equity - Which of the following factors influences a company’s cost of capital?

A) The company’s dividend payout ratio

B) The company’s risk profile and market conditions

C) The firm’s product pricing strategy

D) The number of employees in the company

Ans: B) The company’s risk profile and market conditions - How does financial leverage impact the cost of equity?

A) It reduces the cost of equity

B) It has no impact on the cost of equity

C) It increases the cost of equity due to higher risk

D) It only affects the cost of debt, not equity

Ans: C) It increases the cost of equity due to higher risk - What is the primary reason firms use WACC?

A) To calculate gross profit margins

B) To determine the discount rate for project evaluation

C) To set product prices

D) To determine dividend policy

Ans: B) To determine the discount rate for project evaluation

Relevance to US CPA Syllabus

The cost of capital is essential in the US CPA exam, particularly in financial accounting, taxation, and auditing. It affects decision-making in capital budgeting, financial analysis, and mergers & acquisitions.

Components of Cost of Capital US CPA Questions

- How does a firm’s tax rate affect its cost of debt?

A) Higher tax rates reduce the after-tax cost of debt

B) Tax rates have no impact on the cost of debt

C) Lower tax rates increase the cost of debt

D) Higher tax rates increase the cost of debt

Ans: A) Higher tax rates reduce the after-tax cost of debt - Which of the following is why debt financing is typically cheaper than equity financing?

A) Interest on debt is tax-deductible

B) Debt holders have higher risk than equity holders

C) The cost of equity is fixed

D) Equity financing does not dilute ownership

Ans: A) Interest on debt is tax-deductible - What is the impact of issuing more equity on a company’s WACC?

A) WACC remains the same

B) WACC decreases if cost of equity is lower than cost of debt

C) WACC increases due to dilution effects

D) WACC increases if cost of equity is higher than cost of debt

Ans: D) WACC increases if cost of equity is higher than cost of debt - Which component of capital structure is generally the most expensive?

A) Debt

B) Preferred Stock

C) Equity

D) Retained Earnings

Ans: C) Equity - Which of the following statements about WACC is true?

A) It is used to determine a firm’s revenue

B) It is the minimum return a firm must earn on its investments

C) It is the same for all firms in an industry

D) It only applies to debt financing

Ans: B) It is the minimum return a firm must earn on its investments

Relevance to CFA Syllabus

The cost of capital is a fundamental concept in the CFA syllabus, especially in Corporate Finance and Equity Valuation. Understanding cost of capital is essential for investment analysis, portfolio management, and financial strategy.

Components of Cost of Capital CFA Questions

- What is the relationship between risk and cost of capital?

A) Higher risk leads to a higher cost of capital

B) Higher risk leads to a lower cost of capital

C) Risk has no effect on cost of capital

D) Cost of capital is determined only by company size

Ans: A) Higher risk leads to a higher cost of capital - Which of the following is NOT a component of WACC?

A) Cost of debt

B) Cost of retained earnings

C) Cost of liabilities

D) Cost of equity

Ans: C) Cost of liabilities - Which financial model is commonly used to calculate the cost of equity?

A) CAPM

B) Black-Scholes Model

C) Binomial Model

D) Gordon Growth Model

Ans: A) CAPM - What is the key assumption behind CAPM?

A) Investors have different risk-free rates

B) Investors require a risk premium for taking on more risk

C) The cost of capital is irrelevant to investment decisions

D) All investors have insider information

Ans: B) Investors require a risk premium for taking on more risk

What effect does an increase in financial leverage have on WACC?

A) WACC always increases

B) WACC always decreases

C) WACC initially decreases, then increases beyond an optimal level

D) WACC remains unchanged

Ans: C) WACC initially decreases, then increases beyond an optimal level