The cost of capital serves as the benchmark return an organization should earn on its investments to maintain the market value and entice investors. It is the minimum return required by the debt holders and equity investors. It is an essential concept in business to make funding, expansion, and financial management decisions. The cost of capital becomes critical in analyzing an organization’s investment opportunities and economic strategies. Without it, the company may invest in projects that do not yield sufficient returns to meet the risk incurred. Various methods are employed, such as the cost of capital formula, WACC, cost of equity, and cost of debt, to establish the required rate on investments.

Understanding the components of the capital cost is critical for proper financial decisions. The cost of capital depends majorly on factors like market conditions, risk factors, and economic structure. Firms must take into consideration potential financing sources to be utilized or provided for achieving profit. The cost of capital, according to investment, relies on investment parameters, such as the right investment and financing strategy for a company in terms of its conditions. Cost of capital can be subdivided into different sections in financial management whereby this analysis looks into these possible forms such as WACC calculation, risk and cost of capital, marginal cost of capital, cost of capital vs discount rate, CAPM cost of capital, how to calculate cost of capital, and cost of capital example as a practical application.

Cost of Capital

The cost of capital in management finance is the yardstick for evaluating investment opportunities for companies. Every company has to earn at least its capital cost to sustain itself and stay short of competition. This affects pricing strategies, budgeting, and capital investments. Companies must be cautious when measuring the cost of capital to optimize financial performance.

Why Does Cost of Capital Matter?

The cost of capital manifests in such an enterprise as a beauty aid in strategic financial decisions for enterprises. It is found in investment analysis, project evaluation, and risk measurement. A company that earns less than its cost of capital will find it difficult to survive.

- Investment Decisions: Companies base their decisions on investment projects based on the results of the cost of capital formula. If a project is expected to return less than the cost of capital, the company rejects that project.

- Financing Choices: It gives the company the direction to raise funds, either by taking debt, equity, or retained earnings.

- Valuation of Firms: The cost of capital is a measure chosen by various companies’ investors to determine the companies’ financial capability.

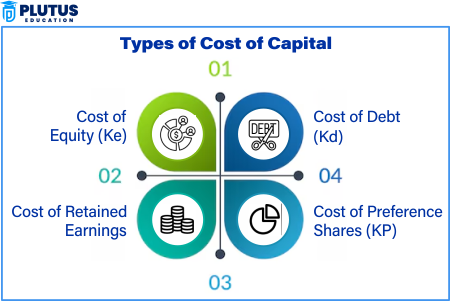

Components of Cost of Capital

The cost of capital can be divided into three components: cost of debt, cost of equity, and overall or weighted average cost of capital (WACC). Each component makes up a company’s financial obligations and determines its investment decisions, affecting it overall.

| Component | Definition |

| Cost of Debt | The interest rate a company pays on its borrowed funds. |

| Cost of Equity | The return required by shareholders to invest in the company. |

| Weighted Average Cost of Capital (WACC) | The overall required return on a company’s capital structure. |

The cost and risk of capital have a close relationship. The higher the risk, the greater the capital cost because investors demand higher returns for their risks.

How to Calculate Cost of Capital?

There are several ways to obtain the cost of capital, including the cost of capital equation, the WACC calculation, and the CAPM cost of capital. These formulas provide a mechanism for estimating the return investors expect in a business.

Cost of Capital Formula

The cost of capital equation depends on whether the company is calculating the cost of equity, cost of debt, or WACC.

Cost of Debt Formula

Cost of Debt = Interest Rate× (1−Tax Rate)

Where:

- Kd = After-tax cost of debt

- Interest Rate = Coupon rate or effective interest rate on debt

- Tax Rate = Corporate tax rate

Cost of Equity Formula (CAPM Approach)

Where:

- Ke = Cost of equity

- Rf = Risk-free rate (return on risk-free securities like government bonds)

- β = Beta (measure of stock’s volatility relative to the market)

- Rm = Expected market return

- Rm−Rf = Market risk premium (additional return expected from the market over risk-free investments)

Weighted Average Cost of Capital (WACC) Calculation

The WACC calculation determines a company’s overall cost of capital by weighing the costs of debt and equity based on their proportions in the capital structure.

Where:

- WACC = Weighted Average Cost of Capital

- E = Market value of equity

- D = Market value of debt

- V = Total capital (Equity + Debt) → V=E+D

- Ke = Cost of equity (calculated using CAPM or DDM)

- Kd = Cost of debt (after-tax)

- T = Corporate tax rate

A higher WACC means a higher risk and required return for investors. Companies aim to keep their WACC low to remain competitive.

Cost of Capital vs Discount Rate

The comparison of the cost of capital and discount rate is crucial in financial management. While both terms are similar, they serve different purposes:

- The cost of capital represents the minimum return needed to satisfy investors.

- The discount rate evaluates investment projects through Net Present Value (NPV) methods.

| Aspect | Cost of Capital | Discount Rate |

| Definition | Minimum return required by investors | Rate used to discount future cash flows |

| Purpose | Used for financing decisions | Used for investment evaluation |

| Formula Used | WACC (Weighted Average Cost of Capital) | It can be WACC, risk-free rate, or risk-adjusted rate |

| Application | Determines the company’s cost of funding | It helps calculate NPV and IRR |

| Risk Consideration | Based on the firm’s overall risk | Can be adjusted for specific project risk |

Relevance to ACCA Syllabus

Cost of Capital is essential for exams like ACCA Financial Management and Advanced Financial Management, as it affects investment appraisal, business valuation, and capital structure decisions. It also forms a basis for finding the cost of debt, equity, and weighted average cost of capital (WACC). It helps develop informed corporate finance decisions, risk considerations, and further capital budgeting strategies.

Cost of Capital ACCA Questions

Q1: What is the primary purpose of calculating the Weighted Average Cost of Capital (WACC)?

A) To determine the risk-free rate of return

B) To calculate the required rate of return for new investments

C) To assess the total amount of debt in a company

D) To determine the accounting profit of a company

Ans: B) To calculate the required rate of return for new investments

Q2: If a company increases its proportion of debt in its capital structure, what is likely to happen to its cost of equity?

A) It remains unchanged

B) It decreases due to lower financial risk

C) It increases due to higher financial risk

D) It is not affected by the debt ratio

Ans: C) It increases due to higher financial risk

Q3: Which of the following factors does NOT directly affect a company’s cost of debt?

A) Corporate tax rate

B) Credit rating of the company

C) The cost of retained earnings

D) Prevailing interest rates

Ans: C) The cost of retained earnings

Q4: When using the Capital Asset Pricing Model (CAPM) to determine the cost of equity, which of the following components is NOT required?

A) Risk-free rate

B) Beta coefficient

C) Expected market return

D) Dividend payout ratio

Ans: D) Dividend payout ratio

Q5: Which financing option is likely to have the highest cost of capital?

A) Debt financing

B) Retained earnings

C) Equity Financing

D) Preference shares

Ans: C) Equity Financing

Relevance to US CMA Syllabus

Cost of capital is integral to the US CMA (Certified Management Accountant) curriculum, particularly in financial decision-making. CMAs must understand WACC, debt and equity financing, and risk-adjusted discount rates to guide company investment and financial planning decisions. This knowledge ensures optimal capital budgeting decisions and risk management.

Cost of Capital US CMA Questions

Q1: According to the Modigliani and Miller theorem (without taxes), how does capital structure affect a firm’s value?

A) The value of the firm remains unchanged

B) Firms with more debt are valued higher

C) Firms with more equity are valued lower

D) Higher leverage reduces firm value

Ans: A) The value of the firm remains unchanged

Q2: How does an increase in corporate tax rates impact the after-tax cost of debt?

A) Increases the after-tax cost of debt

B) Decreases the after-tax cost of debt

C) does not affect the after-tax cost of debt

D) Increases the cost of equity

Ans: B) Decreases the after-tax cost of debt

Q3: A company has a debt-to-equity ratio of 2:1 and a cost of debt of 6%. If the tax rate is 30%, what is the after-tax cost of debt?

A) 1.8%

B) 4.2%

C) 6.0%

D) 5.2%

Ans: B) 4.2%

Q4: Which of the following statements about the cost of capital is true?

A) A firm should always finance new investments using the cheapest source of funds

B) The cost of capital is only relevant for equity financing

C) The cost of retained earnings is generally lower than the cost of new equity

D) The cost of capital is independent of capital structure

Ans: C) The cost of retained earnings is generally lower than the cost of new equity

Q5: In calculating WACC, the proportion of each component in the capital structure is determined based on:

A) Book value weights

B) Market value weights

C) Historical cost of capital

D) Retained earnings only

Ans: B) Market value weights

Relevance to US CPA Syllabus

The cost of capital inthe US CPA exam is primarily tested in the Business Environment and Concepts (BEC) and Financial Management sections. CPAs must understand capital structure, financing decisions, and valuation techniques to assess how companies manage funding sources and make investment choices.

Cost of Capital US CPA Questions

Q1: Which of the following correctly describes the relationship between leverage and cost of capital?

A) Higher leverage always reduces the overall cost of capital

B) An optimal level of leverage minimizes WACC

C) Debt financing does not impact a firm’s cost of capital

D) More equity financing always lowers the firm’s WACC

Ans: B) An optimal level of leverage minimizes WACC

Q2: In determining the cost of common equity, which formula represents the CAPM approach?

A) Cost of Equity = (Dividends per Share / Market Price per Share) + Growth Rate

B) Cost of Equity = Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)

C) Cost of Equity = Net Income / Shareholders’ Equity

D) Cost of Equity = Operating Profit / Total Assets

Ans: B) Cost of Equity = Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)

Q3: A firm has a before-tax cost of debt of 7% and a tax rate of 25%. What is the after-tax cost of debt?

A) 5.25%

B) 4.75%

C) 6.50%

D) 7.00%

Ans: A) 5.25%

Q4: What happens to the cost of equity when a firm takes on more debt?

A) It remains constant

B) It decreases due to a lower WACC

C) It increases due to higher financial risk

D) It is unaffected by debt levels

Ans: C) It increases due to higher financial risk

Q5: The marginal cost of the capital curve is:

A) A downward-sloping curve

B) A straight horizontal line

C) An upward-sloping curve

D) A U-shaped curve

Ans: C) An upward-sloping curve

Relevance to CFA Syllabus

The cost of capital is a key topic in CFA Level 1 and Level 2, forming part of corporate finance and investment decision-making. Candidates must understand CAPM, WACC, and how capital structure affects firm valuation and financial strategy.

Cost of Capital CFA Questions

Q1: Which of the following factors affects a firm’s cost of equity?

A) Bond yield spreads

B) Inflation rate

C) Systematic risk (Beta)

D) Market share growth

Ans: C) Systematic risk (Beta)

Q2: What is a common assumption of the Gordon Growth Model for the cost of equity estimation?

A) Constant dividend growth rate

B) No corporate taxes

C) Risk-free return equals the market return

D) Leverage has no impact on WACC

Ans: A) Constant dividend growth rate

Q3: The CAPM approach assumes that:

A) Investors are risk-seeking

B) Market returns are irrelevant to firm valuation

C) Risk-free rate has no impact on required return

D) Investors are compensated only for systematic risk

Ans: D) Investors are compensated only for systematic risk

Q4: If a company has a beta of 1.2, a risk-free rate of 3%, and an expected market return of 8%, what is its cost of equity using CAPM?

A) 9.0%

B) 7.5%

C) 6.5%

D) 10.0%

Ans: A) 9.0%

Q5: What is the key assumption of Modigliani and Miller’s Proposition I (without taxes)?

A) Capital structure is irrelevant to firm value

B) Debt financing is always cheaper than equity

C) WACC increases with higher leverage

D) Firms should aim for 100% equity financing

Ans: A) Capital structure is irrelevant to firm value