The cost of preference capital is the expected return the company should pay its preference shareholders to utilise the funds. The price is the remuneration to the investors for the risk they take while buying the preference shares. Companies issue preference shares as part of the capital without diluting ownership, but they have to pay dividends, making financing expensive. The costs associated with capital include equity cost, debt cost, and preference capital. Each type differentially affects the overall financing structure and profitability of an organization.

What is Cost of Capital?

The cost of capital represents the required return that a company must generate to justify using its financial resources. Regarding investment decisions, it is used as a benchmark: a company will compare the return on its investments to this cost, and when it is less, that investment will be made.

There are three primary components of the cost of capital:

- Cost of Equity: Expected returns by shareholders if they invest in the company’s stocks.

- Cost of Debt: Represents the interest given by a company on borrowed funds.

- Cost of Preference Capital: The fixed dividend must be paid to preference shareholders.

Funding the businesses is mainly done by the cost of capital for the valuable management. The cost of capital raises concerning financing becoming costly; on the other hand, it can heaper the cost of capital to better baby-growth opportunities.

Cost of Preference Capital

The cost of preference share capital is calculated based on whether the preference shares are redeemable or irredeemable. Thus, the price will be calculated using specific formulas. The cost of preference capital signifies the return an organization must guarantee to its preference shareholders for using their funds. Instead, it refers to fixed dividends on preference shares expressed as a ratio of the capital raised. Unlike equity capital, preference capital does not dilute ownership. Still, it is conceived as a most expensive source of finance since dividends on preference shares are not tax-deductible.

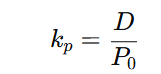

The formula to compute the cost of preference capital is

Kp= Cost of preference capital

D= annual preference dividend, and

Po = net proceeds from preference share sales.

Adjustments would be needed if the shares are sold at a premium or a discount. The costs associated with redeemable preference shares may also consider redemption value and tenure, thus making the calculations slightly more complex.

Factors of Preference Share Capital

Several factors affect the cost of preference capital. They contribute to whether a company has higher or lower preference costs.

- Conditions in the Market: Fluctuations influence the cost of preference shares in the WACC market. When interest increases, investors demand higher dividends, thus increasing costs.

- Credit Rating of the Company: High credit rating companies can raise capital at relatively lower costs. Investors may accept lower dividend rates if they reasonably feel the company is financially strong.

- Dividend Rates and Terms of Payment: The higher the dividend rate on preference shares, the higher the cost of redeemable preference shares will be. Companies with cumulative preference shares (where unpaid dividends accumulate) may have a higher cost than non-cumulative shares.

- Redemption features: If preference shares are redeemable, their cost will depend on the period before redemption and the price at which they will be repurchased.

- Taxation: Dividends on preference shares cannot be deducted for tax purposes like interest on debt. This means that preference capital becomes costlier in financial management.

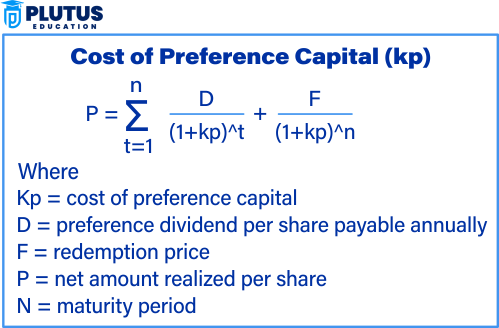

Formula of Cost of Preference Capital

The benefit preferred shareholders expect for their participation in the company is considered the cost of preference capital. This would be calculated using a formula that depends on whether the preference shares were redeemable.

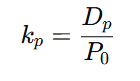

For Irredeemable Preference Shares

The formula for the cost of irredeemable preference capital is

Where:

Kp = Cost of preference capital

Dp = Fixed preference dividend (Dividend per share)

Po = Net proceeds from the issue of preference shares (Issue price – Flotation cost, if any)

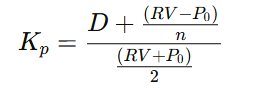

For Redeemable Preference Shares

The formula for the cost of redeemable preference capital is:

Where:

- Kp = Cost of preference capital

- D = Annual preference dividend (Dividend per share)

- Po = Net proceeds from the issue of preference shares (Issue price – Flotation cost, if any)

- RV = Redemption value of preference shares

- n = Number of years until redemption

How Do You Calculate the Cost of Preference Share Capital?

Let us consider an example to calculate the preference share cost.

Cost of Preference Capital Example: Suppose a company issued irredeemable preference shares at $100 per share with a fixed dividend of $10. Therefore, using the formula, the cost of preference capital for the company equals 10%.

For redeemable preference shares, let us assume a company issues shares at $90, having a face value of $100, and redeemable in 5 years, paying $10 every year as a dividend.

This means that the company has an effective cost of 12.63% that needs to be returned to its investors.

Preference Capital vs Equity Capital

Preference shares’ cost vs equity cost comparisons are significant when financing. The financial impact of each type of capital depends on its form.

| Feature | Preference Capital | Equity Capital |

| Fixed Dividend | Yes | No |

| Voting Rights | No | Yes |

| Repayment Obligation | Yes (if redeemable) | No |

| Tax Deductibility | No | No |

| Risk for Investors | Lower | Higher |

| Impact on WACC | Moderate | High |

Preference Shares Over Equity

- Lower Risks to the Investors: Preference shares are preferred by investors because they provide them with guaranteed returns.

- No dilution in Ownership: Subscription of preference shares does not cause a reduction in control among existing shareholders.

- Ease in the Issuance: Unlike equity, preference shares do not require extensive regulatory approvals.

Why is Equity Costlier?

Because equity investors experience uncertainty greater than preference shareholders, they demand higher returns. Shareholders expect an increase in capital; whereas preference shareholders are entitled to a fixed dividend, equity shareholders are entitled to the potential increasing value of shares.

Relevance to ACCA Syllabus

The cost of preference capital is a critical financial management component in the ACCA syllabus, specifically within Financial Management (FM) and Advanced Financial Management (AFM) papers. These concepts help ACCA candidates analyse the cost of raising finance, assess financial viability, and determine an optimal business capital structure. Understanding preference shares’ cost is crucial for investment appraisal and corporate financing decisions.

Cost of Preference Capital ACCA Questions

- Which formula calculates the cost of preference capital when dividends are fixed and perpetual?

A) Cost of Debt = Interest (1 – Tax Rate)

B) Cost of Preference Capital = Dividend / Market Price

C) Weighted Average Cost of Capital = (E/V) × Ke + (D/V) × Kd × (1 – Tax)

D) Dividend Growth Model = D1 / P0 + g

Ans: B) Cost of Preference Capital = Dividend / Market Price - Why is the cost of preference capital higher than the cost of debt?

A) Preference dividends are paid before interest on debt

B) Preference dividends are tax-deductible

C) Preference dividends are paid after corporate tax, unlike interest on debt

D) Preference shares do not have voting rights

Ans: C) Preference dividends are paid after corporate tax, unlike interest on debt - What happens if a company has cumulative preference shares?

A) Unpaid preference dividends accumulate and must be paid before ordinary dividends

B) Preference shareholders can convert their shares into equity

C) The company is not obligated to pay dividends

D) Preference shareholders receive a share of profits

Ans: A) Unpaid preference dividends accumulate and must be paid before ordinary dividends - Which of the following statements about the cost of preference capital is true?

A) It is calculated after considering corporate tax benefits

B) It is generally lower than the cost of equity but higher than the cost of debt

C) It fluctuates based on earnings per share

D) Changes influence it in retained earnings

Ans: B) It is generally lower than the cost of equity but higher than the cost of debt - If a company’s preference share has a market price of $80 and pays an annual dividend of $8, what is the cost of preference capital?

A) 8%

B) 10%

C) 12%

D) 6%

Ans: B) 10% (Cost of Preference Capital = 8 / 80 = 10%)

Relevance to US CMA Syllabus

In Part 2: Financial Decision Making of the US CMA syllabus, the cost of preference capital is essential for understanding capital budgeting, cost of capital calculations, and corporate financing decisions. It helps CMAs analyse financial risk and evaluate capital structure choices for maximising shareholder wealth.

Cost of Preference Capital US CMA Questions

- Which of the following is true about preference capital from a cost perspective?

A) It is considered a part of equity financing

B) It is cheaper than debt financing due to tax advantages

C) It is riskier for investors compared to common equity

D) Preference dividends are mandatory obligations

Ans: A) It is considered a part of equity financing - How does the cost of preference capital affect a firm’s Weighted Average Cost of Capital (WACC)?

A) It has no effect since it is not a part of WACC

B) It lowers WACC because of its stability

C) It increases WACC if its cost is higher than debt financing

D) It does not affect WACC because preference shares do not have voting rights

Ans: C) It increases WACC if its cost is higher than debt financing - Why do firms issue preference shares instead of debt?

A) To take advantage of tax benefits

B) To maintain financial flexibility while avoiding additional debt

C) Because preference shares are cheaper than debt financing

D) To increase the financial risk for common shareholders

Ans: B) To maintain financial flexibility while avoiding additional debt - What is the primary reason preference capital is more expensive than debt financing?

A) Preference dividends are tax-deductible

B) Preference shareholders have higher voting rights than equity holders

C) Preference dividends must be paid even if the company has a loss

D) Preference dividends are paid after tax, making them costlier than tax-deductible debt interest

Ans: D) Preference dividends are paid after tax, making them costlier than tax-deductible debt interest - Which financial decision is affected by the cost of preference capital?

A) Investment in long-term projects

B) Daily working capital management

C) Foreign exchange transactions

D) Employee compensation planning

Ans: A) Investment in long-term projects

Relevance to US CPA Syllabus

The Business Environment and Concepts (BEC) and Financial Accounting and Reporting (FAR) sections of the US CPA syllabus cover capital structure and financing decisions. CPAs must understand the cost of preference capital when assessing financial statements, corporate finance policies, and investment valuation.

Cost of Preference Capital US CPA Questions

- How is the cost of preference capital typically calculated?

A) Using the Capital Asset Pricing Model (CAPM)

B) By dividing the preference dividend by the market price of the preference share

C) Using the Modigliani-Miller theorem

D) Based on earnings before interest and taxes (EBIT)

Ans: B) By dividing the preference dividend by the market price of the preference share - What impact does issuing preference shares have on a company’s debt-equity ratio?

A) It decreases the debt-equity ratio

B) It increases the debt-equity ratio

C) It does not affect the debt-equity ratio

D) It eliminates the need for equity financing

Ans: A) It decreases the debt-equity ratio - Why might a company choose cumulative preference shares over non-cumulative preference shares?

A) To reduce dividend payments

B) To attract investors by ensuring unpaid dividends are carried forward

C) To lower the cost of preference capital

D) To avoid regulatory issues

Ans: B) To attract investors by ensuring unpaid dividends are carried forward - What factor does NOT directly impact the cost of preference capital?

A) Market price of preference shares

B) Preference dividend rate

C) Tax rate of the company

D) Number of common shareholders

Ans: D) Number of common shareholders - Which of the following best describes a hybrid security?

A) Common stock

B) Preference stock

C) Bonds

D) Treasury bills

Ans: B) Preference stock

Relevance to CFA Syllabus

The CFA program’s Corporate Finance and Equity Valuation sections emphasise the cost of preference capital in determining a company’s required return on capital and valuation techniques. Understanding the capital cost structure is crucial for investment analysis and portfolio management.

Cost of Preference Capital CFA Questions

- In which financial analysis is the cost of preference capital most relevant?

A) Liquidity analysis

B) Capital structure analysis

C) Employee performance evaluation

D) Revenue forecasting

Ans: B) Capital structure analysis - Which preference share type provides the lowest cost of capital for a firm?

A) Cumulative convertible preference shares

B) Non-cumulative preference shares

C) Redeemable preference shares

D) Perpetual preference shares

Ans: C) Redeemable preference shares - Why is preference capital considered a hybrid security?

A) It combines features of both debt and equity

B) It is risk-free, like government bonds

C) It has no impact on a firm’s financial leverage

D) It is not recorded on the company’s balance sheet

Ans: A) It combines features of both debt and equity - Which of the following factors affects the cost of preference capital the most?

A) Dividend payout ratio

B) Market interest rates

C) Company’s operating cycle

D) Tax savings on debt

Ans: B) Market interest rates

What happens when a firm issues new preference shares?

A) The cost of debt decreases

B) The cost of equity remains unchanged

C) The overall WACC may increase

D) The dividend payout ratio declines

Ans: C) The overall WACC may increase