CPA fullform is a Certified Public Accountant. This is a professional certification in the fields of accounting and finance. As such, in this regard, one of the most important elements of the course is the subjects that comprise a CPA course. A CPA course subjects include accounting, auditing, taxation, business law, and ethics, which provide the necessary knowledge to be established for the role of a CPA. These subjects provide a base of knowledge and skills for the CPA to work effectively in accounts, audits, taxation, and even financial management. If you are interested in this course, then know about the course curriculum of the CPA, its structure, and all its relevance to your career path.

What is a CPA?

CPA is a licensed professional accountant with expertise in financial services, such as accounting, auditing, taxation, and financial consulting. A CPA will always be responsible for making sure a business complies with financial regulations while making sound financial decisions. A CPA is not only an accountant but an advisor trusted by organizations to effectively manage their finances. They can also represent a person or company on tax-related issues and financial matters.

The title of a CPA is recognized throughout the world, and people with this degree have numerous job opportunities in any industry: from auditing firms and investment banking to consulting and governmental agencies. To become a CPA, candidates would need to first undertake the course on CPA; secondly, qualify to sit an exam, and upon qualification, must pass the examination to become an official CPA. Needless to say, this is also the result of grasping topics taken in a CPA course.

CPA Exam Pattern

The CPA exam follows a multi-format format to test the candidates adequately.

- Multiple-choice questions (MCQs): These are objective-type questions with one correct answer.MCQs test the candidates on their theoretical knowledge and conceptual understanding.

- Task-Based Simulations (TBSs): TBSs are case-based, requiring candidates to apply knowledge to practical problems.Includes working with spreadsheets, preparing journal entries, or filling out tax forms.Example: You may be assigned to prepare a bank reconciliation statement, an adjusting journal entry, or analyze audit findings.

- Written Communication (Only in BEC): This component tests the ability of the candidate to communicate effectively in a professional setting. Tasks involve writing memos, reports, or business letters based on given scenarios. Example: You will be asked to write a memo on the effects of a newly enacted tax law on corporate earnings or suggest ways a client could run his operations more effectively.

- Adaptive Testing: This is a testing mode where the computer adjusts the questions according to how you have answered the previous set of questions. For example, in the first test, you are answering questions correctly; the following test will have more difficult questions.

- Time and scoring: Time for each section: 4 hours. The whole CPA exam takes 16 hours. Scoring: Scores ranging from 0–99A minimum of 75 should be achieved for one to pass any section. Written communication is the smallest percentage score, while the majority is the MCQs and TBSs (in BEC).

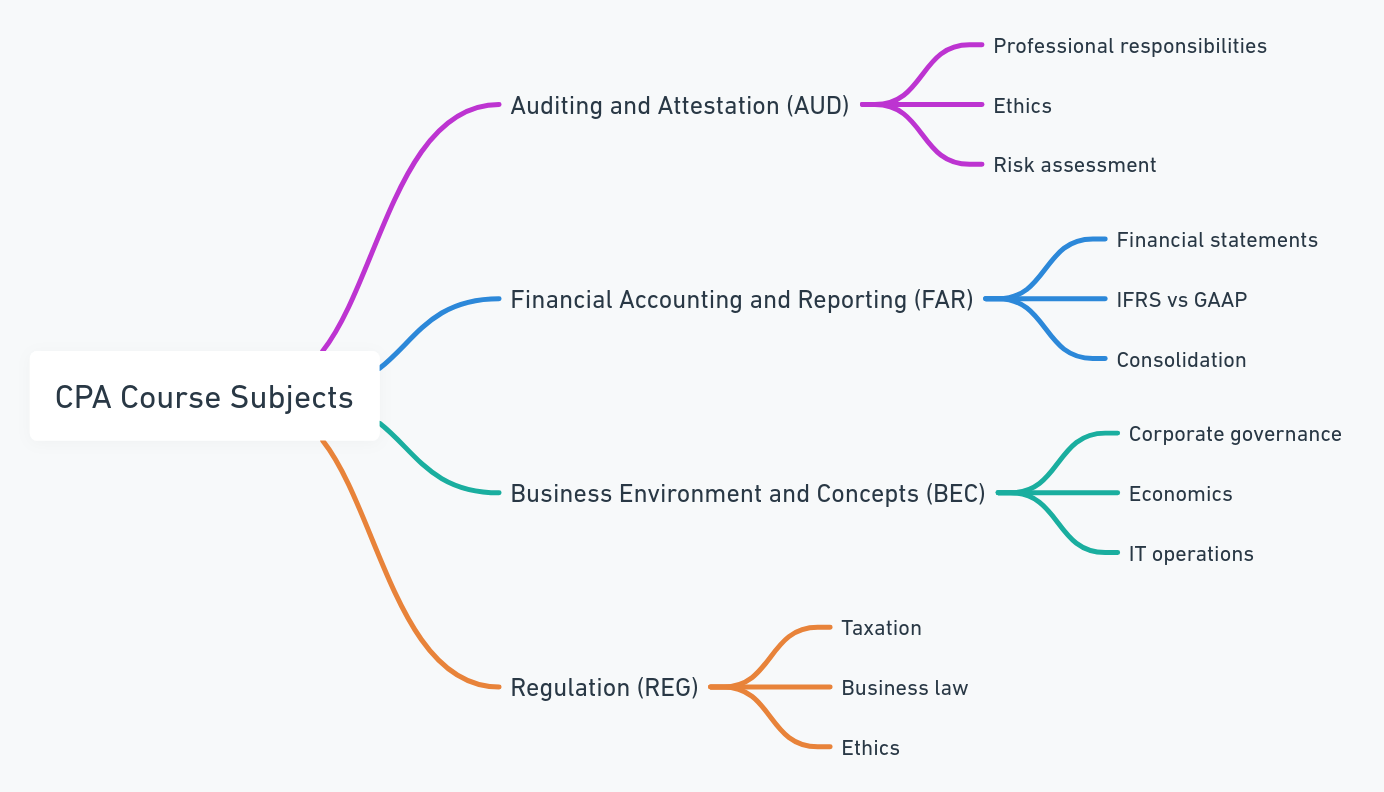

CPA Course Subjects

US CPA course ensures that every significant and critical information about accounting, finance, auditing, and other significant areas forms a significant part of the business. It provides candidates with every CPA subject kept to prepare a candidate at a CPA level. These make a base foundation in the study where candidates receive technical competence and analytical acumen to succeed in practice. Below, We discuss each major subject that comprise the CPA course with relevance and application in the CPA profession.

Auditing and Attestation (AUD)

Auditing provides exposure to auditing processes, ethics, and professional obligations. One’s skills and knowledge will be challenged for its application in the design of an audit, internal controls implementation, and evaluation; gathering and documentation of audit evidence; and finally in writing the findings of a report. Professional standards issued by bodies such as the American Institute of Certified Public Accountants and appropriate professional judgment over ethical dilemmas in accounting should well be appreciated. Main Subtopics in AUD are:-

- Planning the Audit Engagement: Scope Consideration and risk assessment to Level of materiality

- Knowledge of Controls: The internal control system is a determinant for assessing adequacy.

- Evidence evaluation: Gathering, analyzing, and evaluating evidence obtained in a systematic approach gives conclusions as to the accuracy of the Financial Report.

- Knowledge of professional Standards: Relating to either Auditing/ Attestation/ Independence.

- Report Findings: Preparation of a report that either has an unqualified, qualified or adverse opinion based on the finding.

- Ethical Responsibilities: Exercising ethical behavior and staying in line with the AICPA’s Code of Conduct.

| Topic Area | Weightage |

| Ethics, Professional Responsibilities, and Independence | 15-25% |

| Assessing Risk and Developing a Planned Response | 20-30% |

| Performing Procedures and Obtaining Evidence | 30-40% |

| Forming Conclusions and Reporting | 15-25% |

Business Environment and Concepts (BEC)

The BEC section tests the knowledge of the applicant on business operations, risk management, IT systems, and corporate governance. This is a written communication wherein applicants write memos or essays explaining complex business concepts. This would ensure that the applicants have a broad knowledge of the business environment and how the various factors determine organizational success. Key Topics Under BEC:

- Corporate Governance: This will majorly focus on the role and responsibility of boards, risk management, and controls in business operations.

- Economic Concepts and Analysis: Microeconomics and macroeconomics theories, market trends, and impacts of monetary policies are included

- Information Technology: This centers around IT systems, cybersecurity, and the role of technology in business processes

- Financial Management: The concepts most commonly covered include capital budgeting, cost of capital, working capital management, and financial decision-making.

- Strategy Planning: It develops a business strategy; operational planning; and goal setting.

- Written Communication: Develops professional drafts of memos or reports that may explain technical or strategic business concepts.

| Topic Area | Weightage |

| Corporate Governance | 17-27% |

| Economic Concepts and Analysis | 17-27% |

| Financial Management | 11-21% |

| Information Technology | 15-25% |

| Operations and Strategic Planning | 15-25% |

| Written Communication | Tests integrated into other areas |

Financial Accounting and Reporting (FAR)

FAR is the most demanding of them all in the CPA exam. It is about the preparation and presentation of financial statements under US GAAP and IFRS for the areas of financial accounting and reporting. This section is very broad, covering a wide range of topics from the book basics to the more complex financial transaction

- Financial Statements: Deals with income statements, balance sheets, and cash flow statements with disclosure.

- US GAAP and IFRS: Discloses the Difference between US generally accepted accounting principles and International financial reporting standards.

- Preparation of Consolidated Financial Statements: Sets guidelines for consolidating financial statement preparation for the parent and subsidiaries.

- Government Accounting: Deals with state and Local government accounting as well as reports.

- Nonprofit Accounting: Covers detailed accounting related to nonprofit organization accounting including contributions and grants.

- Complex Transactions: Includes accounting for leases, revenue recognition, pensions, and derivative instruments.

| Topic Area | Weightage |

| Conceptual Framework, Standard-Setting, and Financial Reporting | 25-35% |

| Select Financial Statement Accounts | 30-40% |

| Select Transactions | 20-30% |

| State and Local Governments | 5-15% |

Regulation (REG)

This section of regulation specializes in the area of federal taxation, the law of business, and professional responsibilities. Important areas of regulation include application of tax regulations by the candidate, legal implications of a business, and ethical responsibilities. Major Areas of REG

- Individual Taxation: It focuses on the essentials related to income tax filing requirements, deductions, exemptions, and credits about an individual’s income.

- Corporate Taxation: This includes the taxing of corporations, partnerships, and corporations

- Estate and Gift Tax: Estates, Gifts, and Inheritance Planning from a tax perspective

- Business Law: This contains the principles of law regarding business agreements, agency, and compliance with the statute of business activities.

- Ethics and Professional Responsibilities: This contains professional ethics and AICPA Code of Conduct

| Topic Area | Weightage |

| Ethics, Professional Responsibilities, and Federal Tax Procedures | 10-20% |

| Business Law | 10-20% |

| Federal Taxation of Property Transactions | 12-22% |

| Federal Taxation of Individuals | 15-25% |

| Federal Taxation of Entities | 28-38% |

Choosing a CPA Specialisation

The right specialization will depend on your career goals, interests, and industry needs. Specializations are tailored to specific career paths. This also opens up opportunities to work in various roles and industries. Temporary:

- If you want to reveal financial irregularities Forensic accounting is your field.

- If you are interested in a leadership role Management accounting is considered the most suitable option.

- International accounting can be an exciting career for global business professionals.

A CPA is an expert in a specific field. They can enhance their expertise and career level in a highly competitive industry. Specialization also increases employability as it involves the development of higher knowledge in a specific field of study. This leads to popular professionals in their interested industries.

CPA Course Subjects FAQs

What is CPA?

CPA is an abbreviation for Certified Public Accountant. This is a global certification for accountants involved in auditing, taxation, and financial management.

What topics does the CPA course cover?

The CPA curriculum includes accounting, auditing, and taxation. Financial management, business law, and ethics

How long does it take to complete the CPA course?

It typically takes candidates 12-18 months to complete the CPA program, depending on preparation time and exam schedule.

How much does the CPA course cost?

The total cost of a CPA course is between $3,000 and $4,000, including registration and exam fees, and study materials.

What is the format of the CPA exam?

CPA has four modules: Auditing and Attestation (AUD), Business Environment and Concepts (BEC), Financial Accounting and Reporting (FAR), and Regulation (REG).