Markets don’t crash by accident—they implode when ignored warnings meet unchecked greed. From the Great Depression to the 2008 meltdown and the economic shocks of COVID19, every financial crisis has exposed deep structural flaws in global capitalism. These events aren’t rare; they’re recurring consequences of predictable behavior in unpredictable systems. Crisis economics isn’t just a reaction to disaster—it’s a discipline that studies how modern economies break, who pays the price, and how future damage can be mitigated. This evolving field gives us the tools to forecast risks, design resilient systems, and rethink finance beyond growth charts and quarterly profits.

Crisis Economics: Crash Course in Finance

Crisis economics is a crash course in future finance that dissects economic collapse’s patterns, causes, and consequences. It reveals how global markets tend not to be inherently stable, and it has been established that crises are not rare accidents but regular, predictable events. Here, the emphasis is placed on identifying systemic structural weaknesses, tracking speculative bubbles, and proposing modes of sustainable economic governance. Nouriel Roubini’s concept of crisis economics treats financial crashes as structural outcomes, not unexpected freak events. His work explains why economic models often fail to predict crises and how global finance needs reform.

- Nouriel Roubini Predictions: Roubini, often dubbed “Dr. Doom,” accurately predicted the 2008 crisis. His models emphasized speculative bubbles, excessive debt, and loose regulation as key causes.

- Understanding Speculative Bubbles: The markets often ignore the background fundamentals, which inflate prices. Yet once the dawn of reality appears, the speculative bubbles burst, flattening everything in their wake.

- Crisis Causes: Income inequality, reckless lending, deregulation, and misguided economic models are the root causes of the financial crisis. The object of crisis economics is to name and fix those flaws.

- Preparing for Tomorrow: The book and the course advocate for proactive oversight, better financial regulation, and an early warning system for systemic threats. Other measures include closely monitoring debt levels and indicators of impending market collapse.

- Practical Implications: Crisis economics enable policymakers, investors, and students to see risks on the horizon and adjust economic policies to prevent or mitigate future collapses accordingly.

Course Breakdown: Key Themes & Learnings

The course is analytical and practical concerning the anatomy of economic crises. Hence, students, analysts, and policymakers will detect early warning signals and rebuild reforms. Each of the core modules is given more elaborate treatment as follows:

Understanding Systemic Risk and Market Fragility

To teach how financial systems become vulnerable, not from one-off events, but from interconnected risks that grow invisibly over time.

Key Concepts

- Too Big to Fail: Refers to huge financial institutions, whose collapse would lead to the destabilization of the whole economy.

- Example: Lehman Brothers, whose 2008 bankruptcy was the trigger for entire chain reaction.

Now these institutions become dangerous because governments are forced to bail them out, which leads to moral hazard.

- Shadow Banking: This encompasses entities like hedge funds, NBFCs, and asset managers which do not constitute banks. They’re at times not regulated (read: no oversight) but assume risks equivalent to banks-without deposit insurance or capital requirements. Classic case of shadow banking failure is India’s IL&FS crisis (2018).

- Debt Bubbles: A debt crisis occurs when households, companies, or governments borrow more than can be repaid. Once the repayment of debt stalls, liquidity dries up and markets seize. Seen in U.S. housing of 2008 and Greece’s sovereign debt crisis of 2010.

Learning Outcome

- Students will be so equipped to analyze macro-level risks like:

- Over-concentration in certain financial players

- Hidden leverage in markets

- Absence of safety nets in the informal banking sector

Causes of Economic Crisis: A Root-Cause Analysis

The 2008 financial crisis was not sudden—it was a perfect storm of multiple economic crash triggers, including unchecked lending, risky mortgage backed securities, and lack of oversight. This meltdown started in the U.S. housing sector but soon became a global recession, affecting nearly every major economy.

The Role of Subprime Mortgage Crisis

Banks issued highrisk loans to borrowers with low creditworthiness. These subprime mortgages were bundled and sold as safe investments, misling investors worldwide.

Housing Market Crash

Real estate prices skyrocketed due to speculative buying, but when borrowers began defaulting, the housing market crash triggered massive losses.

Debt Bubble Burst

Household and bank debts reached unsustainable levels. Once the bubble popped, liquidity vanished, and credit markets froze.

Shadow Banking & Too Big to Fail

The crisis spread rapidly through the shadow banking system—unregulated financial institutions operating like banks. Major firms like Lehman Brothers collapsed, exposing systemic risk.

Bailout Packages and Central Bank Intervention

Governments stepped in with bailout packages and fiscal stimulus. The U.S. Federal Reserve and European Central Bank injected liquidity to save remaining institutions.

Learning Outcome

Learners will be able to:

- Identify the root drivers of crises, not just symptoms

- Distinguish between policy-driven vs. market-driven causes

- Propose regulatory safeguards and warning mechanisms

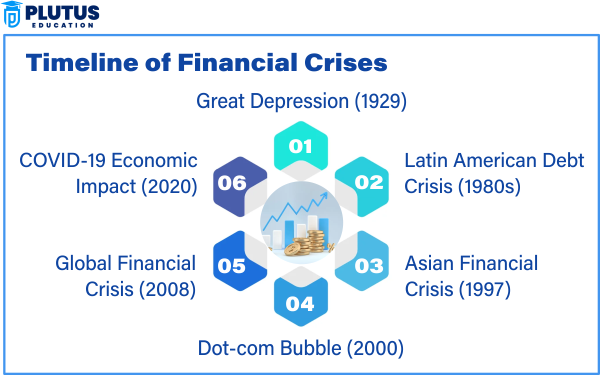

Case Studies: Global Financial Crisis Timeline

The modern financial history of the world has had regular recurring cycles of boom and bust. The great economies, great depressions, and postcertainty economic collapse in the year 2020 were merely similar areas of regular upheaval through thousands of lives and economies to demonstrate countless weakness in the systemic significance, speculative excess, and policy failure. Events such as these are reminders of how vulnerable economies collapse in debt bubbles and black swan events because of unchecked optimism, poor regulation, or geopolitical shocks. Too hastily, each crisis unfolds similarity to those that came before it, from the Asian Financial Crisis to the Global Financial Crisis, 2008 which display virtually the same rapid expansion followed by an equally sudden financial meltdown, and most of the time, require immense central bank intervention and fiscal stimulus. It gives us a sense of how to understand the causes of economic crises, how the governments react to them, and why it is essential to comprehend crisis economics in predicting and managing future spikes of disruption.

Great Depression (1929)

The Great Depression is often regarded as one of the worst economic crashes in modern history. It began with the stock market crash known as Black Tuesday on October 29, 1929, in the United States. Speculative investments in stocks and overleverage formed an unsustainable fattening. Millions of investors lost their savings when the bubble burst, and panic was spread through financial institutions.

Major causes:

- Marginal trading in huge amounts

- Weak banking regulations

- Imploding consumer confidence

- No central bank interference

Consequences:

- The U.S. GDP dropped by nearly 30%.

- Unemployment shot above 25%.

The collapse of trade at an internationally high level caused the overall financial collapse.

There are too many bank failures that are collapsing the system.

Recovery: The New Deal programs included massive fiscal stimulus and job creation schemes that would assist in the slow recovery of the U.S. Also, it had strong banking reforms, such as the Glass Steagall Act.

Latin America Debt Crisis: (1980s)

Due to their inability to service their external debts, Mexico, Brazil, and Argentina faced the Latin American Debt Crisis. Having borrowed heavily during the 1970s and carrying huge foreign debts, the onset of rising oil prices and U.S. interest hikes in the early 1980s made servicing the debt unsustainable.

Chief Causes:

- Rising global interest rates

- Inordinate dependence on foreign capital

- Poor fundamentals and governance

- Inflation and currency devaluation

Consequences:

- Panic in international banking with defaults across the spectrum.

- Halted foreign investment across Latin America.

- Structural changes imposed on them by the IMF and the World Bank.

Recovery: This crisis demanded debt rescheduling, austerity, and the Brady Plan. However, the growth did not turn sustainable before the beginning of the second decade.

Asian Financial Crisis: (1997)

The currency of Thailand was devalued and its foreign reserves drained, which were the catalysts for the Asian financial crisis that acted as a domino across Asia. Countries like Indonesia, South Korea, and Malaysia were successively losing their trade, their currencies, and their stock markets.

Key Causes:

- Heavy shortterm external debt

- Weak regulation and risky lending by the banks

- Unforgiving fixed exchange rate systems

- Decline of investor confidence

Consequences:

- Horrible crash of stock markets all over Asia

- Drastically reduced GDP of affected countries

- Currency value reduced between 30% and 30%70%

- Severe financial collapse together with a sudden upsurge in poverty percentages.

Recovery: Restructuring of economic activities has been applied with the assistance of the IMF and international partners. The country changed from a fixed exchange rate regime to a floating exchange rate system, and there were substantial alterations in banking systems.

Dot Com Bubble: (2000)

The DotCom Bubble is one of the first speculative bubbles in the digital age, which was like the dotcom cure for rising stock prices of tech startups, even including IPOs with poor fundamentals. After realizing that most companies were unprofitable, wide corrective pressure built up in the market.

Mainly causes for occurrence:

- Massive, excessive overvaluation of Internet based companies

- Herd behavior among retail and institutional investors

- Attention catching media, but no due diligence by investors.

Consequences:

- NASDAQ lost almost 80% from 2000 to 2002

- $5 trillion was in ashes about market valuation

- Some companies, such as Pets.com and Webvan, went bankrupt.

Recovery: Having proven that it could maintain a sustainable business model, tech companies such as Amazon and eBay rose up. The crash taught investors how to be more analytical in their valuation process.

Global Financial Crisis (2008)

The Global Financial Crisis has been in 2008, the worst economic crash since the Great Depression. It took its rise within the housing market in the United States; however, it was worldwide for interconnected banking systems that fell under that category.

Key Causes:

- Excessive lending caused the subprime mortgage crisis

- Construction and sale of toxic mortgagebacked securities

- Leverage of the shadow banking system

- Regulatory failure in identifying and stopping risks

Consequences:

- Not only did Lehman Brothers collapse, but also many major banks

- Global recession wherein millions bade goodbye to their jobs and homes in collusion

- Trillions worth of asset losses across markets

Recovery: Bailouts and massive fiscal stimulus could be seen in government undertakings. Unconventional tools such as quantitative easing were used, which several central banks like the Federal Reserve employed.

Economic Damage by COVID19 (2020)

The spread of COVID19 in 2020 was seen as a health crisis but quickly became a financial collapse. Lockdowns stopped the supply chain, caused a drastic decline in consumption, and were followed by a historical amount of job losses around the globe.

Main causes:

- Every trade and tourism stopped instantly across the globe

- Dropoff of consumers in demand

- Disruption in manufacturing and service industries

Consequences:

- The worst global recession since World War II

- Stock market and commodity price crashes, coupled with volatility

- Fast escalation of public debt arising from relief measures

Recovery: Record fiscal injections by governments and other central banks lowering rates to near zero, giving rise to remote work, ecommerce, and stronger digital finance.

| Crisis | Year | Main Cause | Key Impact | Recovery Strategy |

| Great Depression | 1929 | Stock market crash, speculation | Global economic crash, mass unemployment | Fiscal stimulus, banking reforms |

| Latin American Debt Crisis | 1980s | Excessive foreign borrowing | Sovereign defaults, inflation | Debt restructuring, IMF aid |

| Asian Financial Crisis | 1997 | Currency devaluation, external debt | Currency collapse, stock market crash | IMF bailouts, regulatory reforms |

| Dotcom Bubble | 2000 | Tech stock speculation | $5 trillion in losses, NASDAQ crash | Market correction, consolidation |

| Global Financial Crisis | 2008 | Subprime loans, shadow banking | Bank failures, global recession | Bailout packages, regulation |

| COVID19 Economic Impact | 2020 | Pandemic shock | GDP contraction, job losses | Fiscal stimulus, rate cuts |

Overall Learning Outcomes

By the end of the course, learners will be able to:

- Understand the fragility of modern financial systems and global interdependence.

- Identify systemic red flags such as excessive leverage, poor regulation, and asset overvaluation.

- Analyze real crises through case studies and timelines.

- Evaluate policy responses like bailouts, QE, and fiscal boosts.

- Apply crisis economics principles to Indian and global financial contexts.

Crisis Economics A Crash Course in the Future of Finance FAQs

1. What is crisis economics, and how is it different from standard economics?

Crisis economics focuses on the causes and patterns of financial crashes. Unlike traditional economics, it assumes that markets are unstable and crises are frequent, not rare.

2. How did Nouriel Roubini predict the 2008 crash?

Roubini analyzed debt levels, risky lending, and housing bubbles. His Nouriel Roubini predictions warned about a major economic crash driven by systemic financial weaknesses.

3. What is a black swan event in economics?

A black swan event is unpredictable and has severe consequences, such as the COVID19 pandemic. Crisis economics helps identify early signs of such risks.

4. Why is the concept of ‘too big to fail’ important?

Institutions labeled too big to fail are so critical to the economy that their failure would cause a market collapse. This makes regulation and crisis planning essential.

5. How do boom and bust cycles affect everyday people?

These cycles lead to job losses, inflation, and housing foreclosures. Understanding the boom and bust cycle helps people and policymakers prepare for downturns.