The importance of detection risk and audit risk in auditing is paramount. The detection risk deals with the risk of an auditor failing to detect any material misstatement in financial statements. On the other hand, audit risk is when financial statements contain errors or fraud, thereby causing a misinterpretation of the whole situation by the stakeholders. By understanding these risks, auditors can thus develop compelling strategies to ensure accurate financial reporting.

Every audit carries risk, but proper planning for audits and risk assessment minimizes the chances of error. Detection risk and audit risk are interrelated since detection risk forms part of audit risk. No audit can ever be effective without distinguishing and thus minimizing the various types of risk involved.

What is Detection Risk?

Detection risk pertains to the possibility that auditors cannot identify material misstatements in the financial statements. This risk arises because of either the use of ineffective audit procedures or the misinterpretation of evidence. High detection risk indicates a higher chance of undetected error; low detection risk means auditors have sufficiently strong procedures.

Various factors influencing detection risk include auditor competency, audit procedure, sampling scheme used, and the complexity of financial statements. Auditors seek to mitigate detection risk by applying rigorous testing and maintaining professional scepticism. The higher the detection risk, the greater the likelihood that the financial statements have undetected errors or fraud.

How Detection Risk Can Be Minimized

All of these components interplay to determine the overall level of audit risk. The auditor can assure financial integrity and reliability if each element is correctly dealt with.

- Integrity: Increase the number of samples used in the audit. Review audit findings several times.

- Healthy risk assessment: Auditors’ knowledge of all three types of audit risks will also help them carry a more effective audit strategy. Identifying and managing Inherent risk, controlling risk, and detecting risk, therefore, finally allows the auditor to gain greater assurance of the correctness and reliability of the financial reports. Advanced audit techniques

Types of Detection Risks

Detection sort risks can be minimized by audit design, sampling, and human resource skills. Efficient audit documentation and supervision will also contribute to reducing errors.

- Sampling Risk: Sampling risk occurs when the auditors use sampling techniques that cannot select representative samples. Where materials are being tested based on a non-representative sample, they could be led to overlook material misstatements.

- Non-sampling risk arises from human errors, such as misinterpretation of audit evidence or failure to apply the proper audit procedures. It may happen because ofa lack of experience or carelessness during the audit.

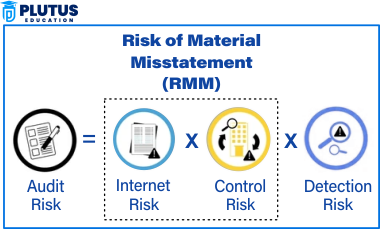

Audit Risk Meaning

Audit risk is the possibility that an auditor may misstate the audit opinion due to an error or fraud in accounting statements. When financial reports contain material misstatements, and the auditor does not detect them, this is a case where audit risk arises. It is a significant concern for auditors since it affects the credibility of all financial reports and their decisions.

Financial statements are prepared using accounting principles by the business, but errors, fraud, or misinterpretation can creep in. These can give the stakeholders almost false financial information if the auditors have lousy guesswork and fail to detect it. The business risk is heightened when an organization has weak internal controls or complex financial transactions.

Types of Audit Risk

To reduce the effect of audit risk, auditors adopt policies and procedures for risk assessment. They analyze the financial data, internal controls, and external factors that could affect the economic strength of an organization.

Inherent Risk

Inherent risk is the risk of errors or fraud in financial statements without considering the business’s internal control. Banking and finance occupy much higher risk because of fluctuating regulations and voluminous transactions.

Factors Influencing Inherent Risk

- The complex nature of transactions

- Industry regulations

- History of misstatements in the financial statements

- Management competence and integrity

Control Risk

Control risk is the risk that a company’s internal control systems will not prevent or detect material misstatements within a timely period. If the design or functioning of internal controls is weak, it is possible for errors and frauds not to be detected, thereby increasing overall audit risk.

Reasons for Control Risk

- Inadequate internal control

- Poor segregation of duties

- Lack of supervision or monitoring

- Human error in financial reporting

Detection Risk

Detection risk is when auditors cannot detect material misstatements in financial statements. Situations may arise whereby the audit procedures employed are not enough to detect the said errors or human error comes into play.

Some of how a detection risk can be lowered include

- Ensure that audit procedures are effective

- Increase the size of the sample in audit tests

Auditing Consideration of Audit Risk and Detection Risk

Almost anything concerning some factors that have been treated is an auditing risk. These include inherent risk, control risk, and detection risk, and each plays an important role in determining the level of risk for an audit.

- Inherent Risk: Inherent risk can be understood as the possibility of error left to be accounted for at the point of unresolved internal controls aiming at rectifying such errors. Thus, this risk is high in industries involving elaborate transactions like financial services and manufacturing.

- Control Risk: Control risk exists when controls fail to prevent or detect material misstatements. Therefore, a company with weak controls will be open to fraud and financial reporting mistakes.

- Detection Risk: Detection risk is expected when the auditor has failed to detect misstatements or errors even after auditing. This risk is driven by the nature of audit procedures and the auditor’s experiences while executing them.

Detection Risk and Audit Risk Relationship

Audit risk is something auditors try to assess and minimize using various methods. These methods understand the environment of their client business, evaluate the internal controls, and perform substantive testing. The less audit risk there is, the more reliable the financial statements become, and further, this represents greater public trust in the system. include

Drain detection risk: Since it is one of the three elements of audit risk, it will affect the overall risk level of the audit.

- Higher detection risk increases audit risk: Failing to detect material misstatements increases the possibility of issuing incorrect audit opinions.

- Audit procedures affect detection risk: The quality and extent of audit procedures will directly contribute to the level of detection risk.

- Strong internal controls minimize detection risk and audit risk: Effective internal controls minimize control risk, reducing the need for extensive audit procedures and thus leading to an associated reduction in detection risk.

- Professional scepticism minimizes both risks: When auditors approach the audit assignments with a sceptical mindset, they lower both forms of risk i.e. detection and audit.

Difference Between Detection Risk and Audit Risk

The chance that auditors will not detect the material misstatements. Audit risk is the overall risk that financial statements contain errors despite conducting audits.

- Causes: Detection risk arises primarily from weak audit procedures or human errors. The three causes of audit risk are inherent risk, control risk, and detection risk.

- Impact: High detection risk increases the probability of erroneous audit conclusions. High audit risk renders financial statements unreliable.

- Control Measures: Detection risk will be controlled by establishing robust audit procedures. The control evaluation and risk assessment will manage audit risk.

- Relationship: Detection risk is part and parcel of audit risk. A high detection risk will also lead to an increase in the audit risk.

| Aspect | Detection Risk | Audit Risk |

| Definition | Risk of failing to detect errors | Risk of incorrect financial statements |

| Cause | Weak audit procedures | Combination of inherent, control, and detection risk |

| Impact | Leads to undetected misstatements | Misleading financial reporting |

| Control Measures | Strong audit procedures | Risk assessment and control evaluation |

| Relationship | Component of audit risk | Includes detection risk |

| Audit Procedures | Affects detection risk | Affects overall audit effectiveness |

| Professional Skepticism | Reduces detection risk | Reduces overall audit risk |

| Sample Selection | Important for reducing risk | Affects detection and audit risk |

| Risk Management | Requires effective audit steps | Requires comprehensive risk assessment |

| Financial Misstatements | Can remain undetected | Can affect financial reliability |

| Internal Controls | Strong controls reduce risk | Internal controls lower audit risk |

| Audit Quality | Enhances detection of errors | Enhances credibility of audit |

| Misstatement Impact | Material misstatements undetected | Incorrect audit opinions |

| Compliance Issues | Non-compliance leads to risk | Affects compliance audits |

| Fraud Identification | Higher risk of missing fraud | Affects fraud risk assessment |

| Audit Sampling | Small sample increases risk | Impacts overall audit risk |

| Business Complexity | Complex businesses increase risk | Higher complexity, higher risk |

| Regulatory Compliance | Audit procedures ensure compliance | Affects regulatory audits |

| External Factors | External changes affect procedures | Economic changes affect risk |

| Error vs. Fraud | Increases chance of missed fraud | Affects fraud detection |

Detection Risk and Audit Risk FAQs

What is detection risk?

Detection risk is when auditors fail to identify material misstatements in financial statements due to poor audit procedures or human error.

Describe the relationship between detection risk and audit risk?

Detection risk is a factor of audit risk. Failure of auditors to detect material misstatements increases audit risks. Hence, a more excellent prospect of mistakes in financial reporting may occur.

What is risk assessment in audit?

Risk assessment in audit denotes identifying and evaluating risks that may harm the credibility of financial statements and, hence, audit conclusions.

What is the perception of risk in audit?

The perception of risk in an audit is about how auditors perceive the likelihood of material misstatements and how internal controls detect and prevent errors efficiently.

What is the difference between risk audit vs. risk review?

A risk audit measures effectiveness in risk management within a project, while a risk review assesses the risk and its ongoing effects on the project’s objectives.