The difference between continuous audit and final audit is in their timing, frequency, and purpose. Continuous audits are still checks made throughout the year, while the final audit is the final audit should be made at the end of the financial period. These audits are used by companies to check accuracy and compliance with accounting standards. Periodic audits help in finding fraud in the early stages, whereas final audits are performed for the verification of financial statements. In this article, we will explain each of the types of audits, what they are, and differ in depth.

What is Continuous Audit?

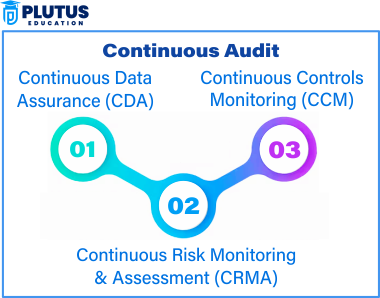

Continuous audit is an audit mechanism of debits performed at intervals across the years instead of a single year-end examination covering the entire year. Especially for businesses involved with vast and complex transactions, it assures monetary accuracy, clarity, and observing fluctuating financial data.

Continuous auditing provides regular monitoring, timely error detection, prevention of fraud, and concurrent updating in accounts. Auditors continually verify transactions, minimizing differences in finance and keeping accuracy unchanged. For larger organizations, it is beneficial since the financial statements are centralized, the internal controls are strengthened, and financial decision-making is more efficient.

Still, ongoing audits are expensive and can interfere with day-to-day business since auditors are there often. The auditors might have an intimate relationship with the employees, which may lead to bias. Nonetheless, continuous auditing provides a critical solution to the challenges faced with financial accuracy, fraud prevention, and adequate internal controls.

What is Final Audit?

A final audit is an audit of a company’s financial records at the end of the financial year. It helps to ensure that all transactions are accurately recorded and that financial statements meet legal and accounting standards. It allows businesses to get ready for taxes, regulatory obligations, and financial reports to stakeholders.

A final audit is characterized by its execution at the year-end, the comprehensive review of all financial statements, and a single approach to examination which minimizes the interruption of business. It helps companies remain in compliance, catch errors before reports are finalized, and provide investors with trustworthy financial data. It is time-saving because it is a one-time process.

But there are downsides to final audits, such as ensuring errors do not go unnoticed over the year when fraud is detected later. It can also be time-consuming because auditors need to review a full year’s transactions at a time. Moreover, auditors’ workload can also pose another significant challenge, as it is difficult to keep up with all the audits.

Difference Between Continuous Audit and Final Audit

Continuous audit & final audit are two types of audits that serve different purposes in financial management, each with its advantages and limitations. Continuous audits offer vigilant oversight and proactive identification of issues, while final audits deliver a thorough annual assessment and regulatory adherence. This comparison is based on their timing, purpose, fraud detection, cost, business impact, and is suitable for which kind of business.

Timing of the Audit

A continuous audit may occur at several points during the fiscal year. Such audits are conducted at periodic intervals, which helps in continuous monitoring of financial transactions and, as a result, improves accuracy throughout the year. Continuous audits are frequent and ensure businesses have an up-to-date view of their finances.

However, a final audit is made only once after a financial year has ended. Translate your time period audit, which can be an annual or half implementation or coverage if you are doing an ideal case. It is also done less often but provides accurate and complete results when year-end comes.

Purpose of the Audit

Continuous auditing is aimed at having accurate reporting throughout the year. Auditors regularly perform checks on financial transactions to identify issues early and fix them before they grow too large to handle. Continuously review and help businesses keep their financial records accurate.

A final audit, however, does offer a summary of the finances at the end of the year. It summarises all transactions, reviews discrepancies and ensures that the financial report complies with accounting standards. This audit provides stakeholders with a comprehensive view of the company’s financial health as of year-end.

Fraud and Error Detection

Continuous Audits aid in the early detection of fraud and errors. Audits are performed quite frequently, which allows businesses to catch any problems or issues in the early stages. Such early detection then helps reduce the potential impact of this fraud or error on the company’s financial statement.

Final audits, on the other hand, may not catch fraudulent activity or misstatements until a year-end review. At the year-end, whilst a final audit also will catch any issues, it does not give the chance to rectify errors or identify fraudulent activities earlier in this process, something that could have serious consequences if overlooked.

Cost and Resources

Continuous audit is more expensive since it need more resources. Since audits happen at regular intervals every year, organizations have to spare a lot of time and resources to conduct audits. This could lead to increased operational costs and strains on the company’s financial and human resources.

Final audits are cheaper, though, as they only happen once a year when the books close. Having one audit to prepare for can help a company reduce the time and resources spent on the audit process, making it a more cost-effective option for some organizations.

Business Disruptions

Continuous audits might violate business processes more often. Conducting these audits often means the business must suspend some work or afford time for auditors to conduct reviews of documents and processes. This will lead to some interruptions in the regular business process.

Year-end audits are final, reducing interruptions. By having one audit scheduled, businesses can prepare for it in advance and ensure that it does not disrupt daily operations. That way, final audits will be less disruptive to regular operations.

Reliability and Legal Acceptance

Continuous audits allow firms to monitor their finances on an ongoing basis and are not a legally required audit. They provide useful information about the company’s financial activities over the year, but they don’t have official recognition from regulation or tax authorities. These audits can be conducted on an ongoing basis to satisfy general assurances but will not meet the legal audit requirements.

Final audits are accepted for regulatory and tax needs. A final audit is the audit legally required on the financial statements of a corporation which supplies the necessary verification to comply with tax law and other regulations. Final audits are crucial for business legal and financial compliance.

Best Fit for Different Businesses

Continuous audits are useful with large companies and complex transactions. These are often high-volume businesses requiring ongoing monitoring. Continuous audits manage those complexities and also help assure the accuracy of the company’s financial records at all times.

Small businesses with minor transactions favour final audits. As there are fewer transactions to oversee, a concluding audit gives a full appraisal of the financial calendar year. This allows small businesses to meet tax obligations and preserve financial openness without constant auditing.

| Basis | Continuous Audit | Final Audit |

| Timing | Conducted at regular intervals throughout the year | Conducted after the financial year ends |

| Purpose | Ensures ongoing accuracy of financial records | Provides a final review of financial statements |

| Fraud Detection | Detects fraud early due to frequent checks | Fraud may remain undetected for a long time |

| Cost | More expensive due to frequent audits | Less costly as it happens once |

| Disruptions | May disrupt daily business activities | No frequent interruptions as it happens at year-end |

| Reliability | Useful for continuous financial monitoring | Provides a final, legally accepted report |

| Best Suited For | Large businesses with frequent transactions | Small and medium businesses with stable records |

Continuous Audit and Final Audit FAQs

1. What is the main difference between a continuous audit and final audit?

Continuous audit occurs several times during the year, whereas final audit is performed once at the end of the financial year.

2. Which audit is more suitable for fraud detection?

Continuous audit are more suitable for fraud detection early on, as financial accounts are examined regularly.

3. Why do organizations prefer final audit to continuous audit?

Companies prefer a final audit as it is economical, less intrusive, and mandatory for compliance.

4. Is continuous audit mandatory for businesses?

No, continuous audit is not mandatory, but businesses with high-frequency transactions can employ it for improved financial monitoring.

5. What is the most important advantage of final audit?

A final audit provides stakeholders with correct financial reporting, legal compliance, and credible financial statements.