Investment decisions play an important role in financial planning and capital budgeting; companies and investors utilize various financial metrics to evaluate the profitability of an investment. One such crucial financial metric is the discounted payback period formula, which helps assess how long it takes to recover an investment by recognizing the time value of money. The discounted payback period formula is given by the year before full recovery+(uncovered cost at beginning /discounted cashflow during the year)

This formula accounts for discounted cash flows to estimate the time required to recover an initial investment. Unlike the simple payback period, it incorporates the fact that money earns interest. The discounted payback period is a widely accepted method in financial analysis to arrive at sound investment decisions.

What is Discounted Payback Period?

The discounted payback period is the time required to recoup an initial investment by applying a discount on future cash inflows to the present value. In contrast to the simple payback period, which does not consider the time value of money, the discounted payback period uses discounted cash flows to ascertain the precise recovery time.

Valuation for discounted payback period calculation is preferred greatly by corporate houses and investors before attempting any capital budgeting decisions. Such a process ensures getting into projects that generate reasonable returns within an acceptable period and is to be used for long-term investments and capital-intensive projects.

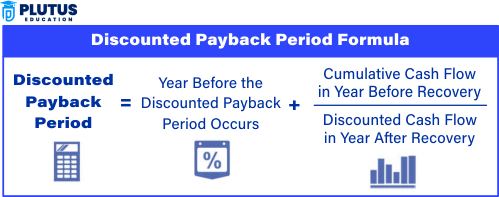

Discounted Payback Period Formula

The discounted payback period formula calculates the time taken for the sum of discounted cash flows to equal the initial investment. It is represented as follows:

The formula ensures that every future cash flow is discounted back to present value before summing it up as they are by date. This has implications because it gives a clear indication as to when the cash flows would recover an investment.

Decision Rules for a Discounted Payback Period Formula

The rule that determines when to approve or reject an investment, in other words, when it is convenient or acceptable to actually pay for an investment, is more clear in terms of the discounted payback period:

Accept the project if the discounted payback period is greater than the preferred recovery time.

- Reject the project when the discounted payback period has an exclusive acceptance limit.

- Corporate houses often define their standard payback limits according to risk acceptance level. If the payback period exceeds such limits, the investment may prove not worth the risk it runs. Thus, selection criteria will try to screen only viable investments.

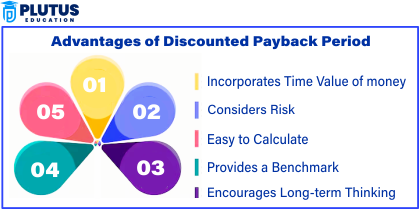

Advantages of Discounted Payback Period Formula

The discounted payback period formula has several advantages that make it appropriate for assessing investment projects. Some of these advantages include:

- Takes into Account Time Value of Money: The method is an improvement over the simple payback period in that it discounts the future cash flows and hence imparts credibility to the evaluation of the respective investments.

- Reduced Investment Risk: Due to its focus on the early recovery of investment, the formula aids in minimizing risk to investors by selecting projects that provide a rapid payback period.

- Good Decision-Making: The discounted payback method enables businesses to gauge project feasibility before capital is invested.

- Ideally Suited for Capital Budgeting: The widespread use of the method in business finance compares investment opportunities and optimizes resource allocation.

- Financial Stability: This ensures that investors will always favour projects that promise rapid recovery of their initial investment, thereby providing liquidity and economic stability.

Assumptions of Discounted Payback Period Formula

Numerous assumptions characterize the discounted payback formula and its resultant validity and reliability. They consist of the following:

- Constant Discount Rate: The assumption of a single discount rate is extravagant throughout the investment period.

- Uniform Cash Inflows: The computed value assumes the project’s cash inflows will remain constant annually.

- Investment Recovery Assumption: The whole method assumes that every project will recover the initial investment.

Limitations of the Discounted Payback Period Formula

The discounting payback period formula constitutes an essential tool. However, it comes with certain limitations:

- Complex Calculations – Discounting of cash flows for each year increases the level of complication in application compared to that of the simple payback period.

- Subjective Nature of the Discount Rate – The discount rate selection is subjective to a large extent, which influences the accuracy of this method.

- Inapplicable for Long-Term Projects – As this formula does not emphasize overall project profitability, it is unfit to be applied in assessing long-term investments.

How to Calculate Discounted Payback Period Using the Formula?

Calculating the discounted payback period involves several steps to maintain either measure of time for any possible error. The steps may include:

Step 1: Identify the Initial Investment

Once the original investment is decided on, ascertain the total cost of this investment to be recovered over time through future cash inflows.

Step 2: Estimate Future Cash Flows

Forecast cash flows that are likely to occur within every year of the project. Cash flows should, however, be based on realistic estimations.

Step 3: Choose the Discount Rate

Choose a discount rate, which may usually be either the cost of capital of the concerned company or the rate of return required.

Step 4: Discount Each Cash Flow

The present value of each of the future cash flows is determined separately by the discount rate. Discounting cash flow is given by: PV = FV/(1+r)^t

where PV is the present value, FV= future value, r is the discount rate, and t is the year.

Step 5: Sum the Discounted Cash Flows

Add all the discounted cash flows cumulatively until the total equals or exceeds the initial investment.

Step 6: Determine the Discounted Payback Period

Find the year the cumulative discounted cash flow equals the initial investment. If the cumulative discounted cash flow lies between two years, interpolation can give an exact period.

The above steps ensure that cash flows are treated fairly during discounting time.

Discounted Payback Period Example

Cash outlay of 50000, expected cash inflow of 15000 per annum over the next four years, and a discount rate of 10%.

| Year | Cash Flow (INR) | Discount Factor (10%) | Discounted Cash Flow (INR) | Cumulative Discounted Cash Flow (INR) |

| 1 | 15,000 | 0.909 | 13,635 | 13,635 |

| 2 | 15,000 | 0.826 | 12,390 | 26,025 |

| 3 | 15,000 | 0.751 | 11,265 | 37,290 |

| 4 | 15,000 | 0.683 | 10,245 | 47,535 |

Since 50,000 was not fully recovered in 4 years, it can be interpolated that the discounted payback period was just over 4 years.

Payback Period vs Discounted Payback Period

The payback period and discounted payback period are two different methods to analyze the time during which an investment is to be recovered. The main difference is that the discounted payback period considers the time value of money, making it a more realistic approach.

| Criteria | Payback Period | Discounted Payback Period |

| Time Value of Money | Ignored | Considered |

| Accuracy | Less accurate | More accurate |

| Decision Making | Less reliable | More reliable |

| Calculation Complexity | Simpler | More complex |

| Risk Assessment | Lower risk visibility | Higher risk visibility |

The discounted payback period is preferred because it is a much better representation of the real worth of an investment.

Discounted Payback Period FAQs

How often do you pay someone to work on your payback?

An amount that an investment completes the recovery of its cost is the payback period. This does not consider any time value of money.

How is the payback period defined?

Discounted payback period is the time required to recover the initial investment in a given project after discounting future cash flows for the time value of money.

What is the discounted payback period?

The period for recovery from an investment after adjusting future cash flows for the time value of money is called the “discounted payback period”.

What is the discounted payback period formula?

The discounted payback period formula sums discounted cash flows until they equal the initial investment.

What are the advantages and disadvantages of payback period?

Advantages: simplicity, fast decision-making; disadvantages: do not consider profitability, do not consider the time value of money.