The growth of commercial banks in India reflects the progress of the nation’s economy and its changing financial structure. From small beginnings under colonial rule to their position today as pivotal institutions for economic development, commercial banks have undergone transformative growth. Their journey mirrors India’s transition from an agrarian economy to an industrialized and service-driven one. Today, commercial banks are not only custodians of public savings but also drivers of investment, innovation, and financial inclusion. The story of their growth shows resilience, adaptability, and an unwavering commitment to supporting national aspirations.

What is Commercial Bank?

A commercial bank is a financial institute established mainly to accept deposits from the public and issue loans for various purposes: personal, corporate, governmental, and so forth. These are profit-oriented firms and represent an integral element of the financial system ensuring liquidity within the economy; they perform monetary operations between savers and borrowers.

Commercial banks serve large markets with different services, including deposit schemes, credit facilities, and advisory services. They also facilitate businesses with trade finance, working capital loans, and foreign exchange management. Beyond these services, commercial banks play important roles in developing national economies by allowing for the uninterrupted flow of credit and stabilizing financial activities.

Unlike cooperative banks or development banks, commercial banks operate on profit-making while simultaneously satisfying social and economic goals. Success for commercial banks relies on their ability to be financially prudent and innovative in terms of services offered.

Evolution of Commercial Banks

The evolution of commercial banks in India is a landmark in the socio-economic change of the country and a march toward modernization. Though their roots can be traced back to the colonial period, their significance and influence grew post-independence.

Pre-Independence Period

Commercial banking history in India dates back to the late 18th century with the founding of the Bank of Hindustan in 1770 in Calcutta (now Kolkata). Thereafter, during the British period, the Presidency Banks in Bombay (Mumbai), Madras (Chennai), and Calcutta were set up. The above-mentioned banks primarily served the interests of British traders and business enterprises.

In the early 20th century, Swadeshi movements rose, and the first indigenous banks were established, including the Punjab National Bank and the Bank of India. Early banks provided the foundation for the system we have today.

Post-Independence Period

After independence in 1947, India faced the monumental task of rebuilding its economy. The process of nationalizing commercial banks began with the incorporation of 14 major banks in 1969. Regional disparities, financial inclusion, and credit flows to priority sectors like agriculture and small industries became the motivations behind the decision.

The Reserve Bank of India was established in 1935, which further strengthened the banking infrastructure. It introduced regulations to ensure financial stability and promote systematic growth in the sector.

Liberalization and Modernization

The liberalization of the Indian economy in 1991 brought transformative changes in the banking sector. Private sector banks such as ICICI Bank, HDFC Bank, and Axis Bank came into the market with competition, efficiency, and customer-centric innovations. Further, the advent of technology revolutionized banking operations with the help of ATMs, internet banking, and mobile banking services. Hence making commercial banks a significant cornerstone of India’s economic development.

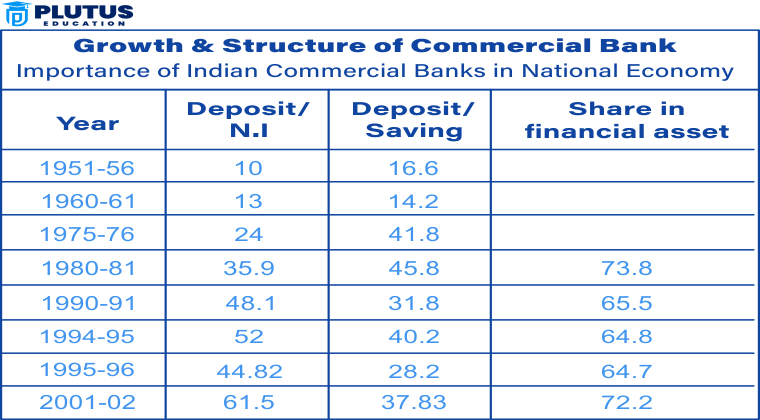

Growth of Commercial Banks in India (1951–1991)

The period 1951-1991 was a critical stage in the development of Indian commercial banks. It was one marked by nationalization, expansion of branches, and concerted efforts toward financial inclusion. It was during this period that commercial banks turned out to be instruments of economic planning and social transformation.

Nationalization of Banks

The first nationalization occurred in 1969 by nationalizing 14 banks from the private sector. This was a landmark move to ensure credit was evenly distributed around regions and sectors. In this way, the government looked to open up banking opportunities to rural and semi-urban areas, which were generally excluded from private banking. A further six banks were nationalized in 1980. Thus, strengthening the hand of the government in this sector.

Nationalization enabled the government to channel credit into priority sectors like agriculture, small-scale industries, and exports. It also allowed the government to exercise greater control over economic resources and support developmental initiatives.

Expansion of Banking Services

After nationalization, the expansion of commercial banks was spectacular. By 1990, banks had developed an extensive network of branches spread all over the country, even to the remotest parts. This expansion helped savings among the rural people and mobilized funds for investment.

Deposit Mobilization and Credit Disbursement

The confidence generated by nationalized banks increased the deposits. Commercial banks initiated different savings schemes, making banking more appealing to the public. They also diversified their lending portfolios by offering credit for housing, education, and agriculture.

This period also marked the creation of Regional Rural Banks in 1975 that were specifically meant to focus on rural areas while still being cost-effective. The RRBs supported the role of commercial banks in achieving rural development.

Commercial Bank’s Growth During 1991-92 to 2003-04

The economic reforms initiated in 1991 ushered in a new era in the growth of commercial banks in India. This period was characterized by liberalization, privatization, and modern technology adoption. This changed the face of banking in the country.

Liberalization and Privatization

In place of entry barriers, it allowed opening access to private sector banks by entering the market, and it increased competition and efficiency because banks like ICICI, HDFC, and Axis also came into existence there with a customer-centric attitude and innovative financial products. Foreign banks also increased their inroads in terms of global best practices practiced in banking.

Technological Advancements

Technology became a game-changer during this era. Banks adopted core banking solutions (CBS), enabling customers to access their accounts from any branch. The introduction of ATMs, online banking, and mobile banking services enhanced convenience and customer satisfaction. This technological leap also improved operational efficiency and reduced transaction costs.

Financial Reforms and Regulation

The RBI introduced several regulatory measures to strengthen the financial health of commercial banks. Capital adequacy norms under the Basel guidelines ensured that banks maintained sufficient capital to absorb risks.

Expanding Services and Market Reach

Commercial banks diversified their offerings during this period, venturing into insurance, mutual funds, and wealth management. They also increased their focus on retail banking, offering home loans, car loans, and personal loans to cater to the burgeoning middle class.

Challenges and Opportunities

While the reforms brought numerous opportunities, they also posed challenges. The global financial crises highlighted the vulnerability of Indian banks to external shocks. Additionally, the digital divide limited the penetration of technology-driven banking services in rural areas. However, the resilience of Indian banks and their ability to adapt ensured steady growth.

Growth of Commercial Banks FAQs

Why did India nationalize banks?

Banks were nationalized to promote financial inclusion, direct credit to priority sectors, and reduce the concentration of wealth in private hands. It ensured equitable access to banking services across rural and urban areas.

What impact did liberalization have on Indian commercial banks?

Liberalization introduced competition, encouraged private and foreign banks, and facilitated technological adoption. It transformed banking services, making them more customer-centric and efficient.

How did technological advancements impact commercial banking in India?

Technological advancements like core banking solutions, ATMs, and online banking improved operational efficiency, enhanced customer convenience, and reduced transaction costs.

What do commercial banks in India face the main challenges?

Commercial banks face challenges like managing non-performing assets, complying with global regulatory standards, and addressing the digital divide in rural areas.

How do commercial banks contribute to economic development?

Commercial banks mobilize savings, provide credit for investment, support businesses, and promote financial inclusion, thereby driving economic growth and stability.