Hedging techniques are financial means companies and investors apply to mitigate risks of price variation, currency fluctuations, and market volatility. These methods reduce probable loss while ensuring the stability of financial transactions. Hedging Techniques are frequently employed in stock markets, foreign exchange, commodities, and company operations. Various hedging mechanisms must be understood for efficient risk management and financial planning. The assets and profits of investors and companies can be safeguarded through internal and external hedging methods.

What is Hedging?

Hedging is a risk management tool in finance to guard against undesirable price fluctuations in assets, currencies, or commodities. Hedging is done by taking an opposite position in the market to cancel out losses. Companies, investors, and financial institutions employ hedging to guarantee stability and lower exposure to unpredictable market conditions.

Why is Hedging Important?

Hedging is an effective way to mitigate financial risks as it shields businesses from abrupt changes in the market or currency values. It also promotes price stability because it should make raw material and product costs predictable. Companies hedge to protect foreign investments from currency fluctuations and prevent these capital losses. It helps businesses plan for long-term growth with financial predictability, stability, and improved risk management.

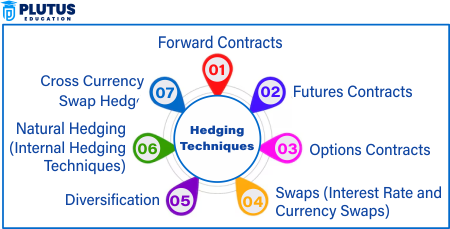

Hedging Techniques

Hedging techniques vary based on market conditions and financial goals. These techniques are important for each business. Below are seven widely used methods:

Forward Contracts

A forward contract is a customisable contract between two parties to exchange an asset for a specified price at a specified future date. Forward contracts are used by businesses to hedge against foreign exchange and commodity price volatility. This allows companies to plan their cash flows and avoid surprises with financial losses. Let’s say an importer in India is expecting to pay ₹800,000,000 in six months. An importer can lock in the exchange rate today for a forward contract so that he explicitly knows how much Indian rupees he will pay in the future, ensuring price stability and avoiding exchange rate risk;

Futures Contracts

A futures contract trades on an exchange and is a standardised financial contract that enables firms to hedge against price fluctuations in various stocks, commodities, or currencies. Futures are regulated, providing higher transparency and security in the financial markets. Futures hedge one of the biggest headaches for investment managers: uncertainty. This means, for example, that a wheat farmer can sell wheat futures to lock in a price and guarantee themselves stable income even if prices fall in the market later on.

Options Contracts

Options contracts give investors and companies the right but not the obligation to buy or sell an asset at a given price on or before a specific date. Options are flexible compared to forward and futures contracts. The two primary types include call options, which bestow the right to purchase, and put options, which bestow the right to sell. Put options are used by investors for protection against a possible drop in stock prices, which keeps losses minimal in times of a falling market.

Swaps (Interest Rate and Currency Swaps)

A swap is a monetary arrangement between two parties to exchange cash flows to protect against interest rates or currency movements. Swaps enable firms to control financial risks and lower borrowing costs. Interest rate swaps allow businesses to exchange fixed and floating interest rates, whereas currency swaps entail exchanging principal and interest payments in two different currencies. For instance, a US business with a euro-denominated debt can use a currency swap to prevent losses resulting from negative exchange rate changes.

Natural Hedging (Internal Hedging Methods)

Natural hedging is an in-house business strategy for managing currency risk, which relies on operational decisions rather than financial instruments. Such measures include aligning revenues and costs in local currency and setting up production capabilities locally to cut import costs. An example of this would be a US-based company selling products in Japan. To avoid the currency exchange risk, the original company would set up a manufacturing unit in Japan that would financially stabilise the business in a foreign market.

Diversification

Diversification is a risk management strategy investors use to spread their investments across various asset classes or sectors to reduce risk exposure. By limiting potential losses from such price drops, this method contributes to overall portfolio stability. For example, if you lose money over a period, an investor who holds a mix of stocks, bonds, real estate, or any other commodity would have reasons to be less concerned if one of those sectors is underperforming because they will still get returns from elsewhere.

Cross Currency Swap Hedge

A cross-currency swap hedge is a financial instrument that allows firms to exchange their debt obligations denominated in various currencies to alleviate exposure to fluctuations in exchange rates. Such a strategy enables companies to manage foreign currency exposure better. For example, a European company with US dollar-denominated debt can enter into a swap arrangement with a US company with euro-denominated debt. Both companies are lowering currency fluctuation risks and stabilising their financial positions by exchanging debt obligations.

How Do Hedging Techniques Work?

Hedging strategies assist companies and investors in guarding against financial threats like market movement, currency fluctuation, and interest rate volatility. The journey starts with the recognition of risks and measuring levels of exposure. Organisations select an appropriate hedging strategy, like forward contracts, options, swaps, or natural hedging depending on financial objectives and market conditions.

Once the hedging approach is chosen, companies implement the hedge by acquiring fixed prices, rates, or exchange values to avoid risks. Effectiveness is achieved through frequent review and adjustments due to changing market conditions. For instance, a company importing raw materials from China might apply forward contracts in the Chinese yuan to hedge against adverse exchange rate movements.

Internal and External Techniques of Hedging

Hedging strategies are categorised into internal and external methods to assist firms in mitigating financial risks. Internal hedging involves mitigating risks by business operations, including diversification, cost management in local currencies, and establishing foreign manufacturing facilities. These strategies enable companies to minimise their exposure to currency fluctuations and market risks without depending on financial agreements.

Outward hedging refers to using financial instruments such as forward contracts, options, swaps, and futures to hedge against risks. Companies also utilise banking products, including loans in corresponding currencies, to prevent foreign exchange losses. These methods give companies structured cover from financial risks and assist them in stabilising cash flows in unstable markets.

| Hedging Type | Description | Examples |

| Internal Hedging Techniques | Reducing risk through business operations. | Natural hedging, diversification. |

| External Hedging Techniques | Using financial instruments to hedge risk. | Forward contracts, options, swaps. |

Foreign Exchange Risk Hedging Techniques

Foreign exchange risk hedging strategies protect investors and companies against exchange rate volatility. Businesses apply forward contracts to fix exchange rates, currency swaps to swap foreign currency liabilities, and options contracts to hedge against adverse rate fluctuations. The mechanisms guarantee constant cash flows and avert financial losses in international markets.

Another useful method is invoice currency hedging, in which companies make transactions in stable currencies to minimise risk. For instance, an exporter selling European products can use a forward contract to hedge against the euro’s depreciation and have predictable revenue. Effective hedging strategies enable companies to conduct international trade confidently without concern for currency volatility.

Relevance to ACCA Syllabus

Hedging strategies are integral to financial management within the ACCA syllabus, especially within the Financial Management (FM) and Advanced Financial Management (AFM) papers. Hedging strategies enable students to grasp how to hedge against foreign exchange, interest rate, and commodity price risks, which are vital for multinational companies. ACCA syllabus focuses on the practical use of derivatives, forward contracts, futures, options, and swaps to safeguard businesses from financial risk.

Hedging Techniques ACCA Questions

Q1: Which of the following financial instruments is commonly used in hedging foreign exchange risk?

A) Bonds

B) Forward contracts

C) Equity shares

D) Fixed deposits

Ans: B) Forward contracts

Q2: What is the primary purpose of a futures contract in hedging?

A) To speculate on asset prices

B) To eliminate the risk of price fluctuations

C) To increase portfolio leverage

D) To avoid accounting regulations

Ans: B) To eliminate the risk of price fluctuations

Q3: Which of the following best describes an interest rate swap?

A) A contract to exchange fixed interest payments for floating rate payments

B) A financial instrument used to acquire company ownership

C) A loan agreement between two parties

D) A stock market investment strategy

Ans: A) A contract to exchange fixed interest payments for floating rate payments

Q4: Under IFRS 9, which hedge accounting technique recognizes changes in fair value directly in profit or loss?

A) Cash flow hedge

B) Fair value hedge

C) Speculative hedge

D) Currency hedge

Ans: B) Fair value hedge

Q5: A company uses a put option to hedge against declining stock prices. What type of hedge is this?

A) Interest rate hedge

B) Equity hedge

C) Foreign currency hedge

D) Credit risk hedge

Ans: B) Equity hedge

Relevance to US CMA Syllabus

The US CMA curriculum addresses hedging in the Financial Management section, emphasising risk management techniques, financial instruments, and derivatives. It is essential for professionals dealing with corporate finance, treasury functions, and financial risk management in organisations to know about hedging methods. The CMA exam assesses students on how companies reduce risks through futures, options, swaps, and forward contracts to stabilise cash flows and guard against unfavourable financial market movements.

Hedging Techniques US CMA Questions

Q1: What is the primary goal of hedging in financial risk management?

A) To increase potential returns

B) To reduce exposure to financial risks

C) To eliminate all market risks

D) To speculate on asset price movements

Ans: B) To reduce exposure to financial risks

Q2: Which financial instrument is most commonly used in hedging commodity price risks?

A) Mutual funds

B) Interest rate swaps

C) Futures contracts

D) Credit default swaps

Ans: C) Futures contracts

Q3: When a company uses a currency forward contract to hedge foreign exchange risk, what is it protecting against?

A) Inflation risk

B) Interest rate fluctuations

C) Exchange rate fluctuations

D) Credit risk

Ans: C) Exchange rate fluctuations

Q4: A company expecting to receive foreign currency payments in the future may hedge its exposure using:

A) Call options

B) Forward contracts

C) Long-term bonds

D) Equity investments

Ans: B) Forward contracts

Q5: In risk management, what is the purpose of a cash flow hedge?

A) To stabilize earnings volatility from variable cash flows

B) To speculate on future stock market movements

C) To improve financial leverage

D) To minimize capital investment

Ans: A) To stabilize earnings volatility from variable cash flows

Relevance to US CPA Syllabus

Under the US CPA syllabus, hedging methods are taught under Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC). Candidates must recognise how hedging influences financial reporting, specifically accounting for derivative instruments under US GAAP. Hedge accounting, fair value hedges, cash flow hedges, and foreign currency risk management with derivatives are tested in the CPA exam.

Hedging Techniques US CPA Questions

Q1: Under US GAAP, where are changes in fair value of a cash flow hedge recorded?

A) Profit and loss account

B) Other comprehensive income

C) Retained earnings

D) Notes to financial statements

Ans: B) Other comprehensive income

Q2: What type of hedge protects against fluctuations in interest rates affecting future borrowings?

A) Fair value hedge

B) Cash flow hedge

C) Currency hedge

D) Commodity hedge

Ans: B) Cash flow hedge

Q3: Which of the following instruments would a company use to hedge a fixed-interest loan?

A) Foreign currency swap

B) Floating-to-fixed interest rate swap

C) Stock options

D) Forward contract

Ans: B) Floating-to-fixed interest rate swap

Q4: If a company reports a derivative as a fair value hedge, how are gains and losses recognized?

A) Deferred until realization

B) Recognized in other comprehensive income

C) Immediately in profit and loss

D) Off-balance sheet disclosure

Ans: C) Immediately in profit and loss

Q5: Under US GAAP, hedge effectiveness must be assessed:

A) Once at the inception of the hedge

B) Annually

C) Only when financial statements are prepared

D) On an ongoing basis throughout the hedge duration

Ans: D) On an ongoing basis throughout the hedge duration

Relevance to CFA Syllabus

The CFA program thoroughly discusses hedging strategies in its portfolio management, derivatives, and risk management modules. Candidates are taught how to apply derivatives like futures, options, and swaps to hedge interest rate risks, currency risks, and equity market volatility. The CFA curriculum applies hedging strategies to maximise portfolio performance while reducing risk exposure.

Hedging Techniques CFA Questions

Q1: What is the main benefit of hedging options over forward contracts?

A) Options provide leverage with minimal risk

B) Options allow flexible hedging without an obligation

C) Options eliminate all risk exposure

D) Options are cheaper than forward contracts

Ans: B) Options allow flexible hedging without an obligation

Q2: A fund manager holds a large portfolio of stocks and wants to hedge against potential declines in stock prices. What instrument is most suitable?

A) Interest rate swaps

B) Put options

C) Forward rate agreements

D) Currency futures

Ans: B) Put options

Q3: What does a zero-cost collar hedge strategy involve?

A) Buying a call option and selling a put option at the same strike price

B) Buying a put option and selling a call option with different strike prices

C) Buying and selling futures contracts simultaneously

D) Using only forward contracts to hedge risk

Ans: B) Buying a put option and selling a call option with different strike prices

Q4: What is the primary use of a currency swap in international finance?

A) To speculate on exchange rate fluctuations

B) To hedge currency exposure from international borrowings

C) To increase foreign exchange reserves

D) To gain arbitrage profits in forex trading

Ans: B) To hedge currency exposure from international borrowings

Q5: If a company wants to hedge against a potential increase in interest rates, which strategy is most appropriate?

A) Buying a put option on bonds

B) Entering into an interest rate swap paying fixed rates

C) Buying stocks in financial institutions

D) Using an exchange-traded fund

Ans: B) Entering into an interest rate swap paying fixed rates