Calculate closing stock is an important aspect of accounting for any business because it affects the cost of goods sold (COGS) and the overall profitability. In simple words, closing stock refers to the value of the inventory that remains unsold at the close of a financial period. This includes raw materials, work-in-progress, and finished goods without the sale of these goods. Calculating closing stock is important to deriving proper financial statements and proper profit margins.

Closing stock not only assists with bookkeeping but also ensures that a business has enough stock of inventory to meet the demands of the future without overstocking, which ties up cash and increases the storage cost. There are multiple methods by which the closing stock can be calculated, and this method will affect the company’s financial outcomes and tax liabilities.

Methods to Calculate Closing Stock

The method chosen to calculate closing stock depends on the type of business and the inventory management system in place. The following are the most common methods:

1. First In, First Out (FIFO)

FIFO assumes that the first items purchased are the first to be sold. This method is best suited when prices are going up because it takes into account the older, cheaper stock sold first, thus representing lower COGS and higher profits.

Example: Assume that a firm bought 100 units at $10 each and then another 100 units at $12 each. By using the FIFO method, the first 100 units sold will be costed at $10 per unit.

Calculation:

FIFO Closing Stock = Latest Purchased Stock

2. Last In, First Out (LIFO)

LIFO assumes that the last items purchased are the first to be sold. It is useful in inflation because the higher cost of recent purchases is sold, which brings down taxable income.

Example: Using the same example mentioned above, if LIFO were to be applied, then 100 units sold would be valued at $12 each.

Calculation:

LIFO Closing Stock = Oldest Purchased Stock

3. Weighted Average Cost Method

This method calculates the average cost of all inventory purchased and uses this average cost to value both the goods sold and the closing stock.

Formula:

Weighted Average Cost = (Total Cost of Goods Purchased) / (Total Units Purchased)

Example: If you purchased 200 units (100 at $10 and 100 at $12), the weighted average cost would be:($1000 + $1200) / 200 = $11 per unit.

4. Specific Identification

The cost of every unit in the stock is accounted for in this method. Therefore it can determine the cost of every sold or remaining unit. This will heavily apply to high-value items or special products such as cars or designer merchandise.

Example: Once you sell a certain model of car, the actual cost of the model is subtracted, and the remaining units will reflect their true costs.

Pricing Method Impact on Closing Stock

The pricing method used to calculate closing stock has a significant impact on the business’s financial statements, profitability, and tax liabilities.

FIFO Impact

If prices are increasing, then FIFO would reduce the COGS and increase the closing stock value more than necessary, thereby increasing the profit reported. In some cases, it increases tax liabilities.

Effect: This means a higher closing stock value and, therefore a higher asset on the balance sheet.

LIFO Impact

LIFO generates higher COGS in inflationary times because the latest, higher-cost inventory is sold first. This reduces the taxable income but also decreases the value of the closing stock.

Effect: The reducing value for closing stock reduces assets reported on the balance sheet but can give tax benefits in the short run.

Weighted Average Method

The weighted average cost is a smoothening effect of fluctuating prices and provides a middle ground. It neither maximizes nor minimizes profits; however, it would keep on giving the same method for calculating closing stock across time.

Effect: Slight effect on both COGS as well as closing stock valuation.

| Method | Effect on Closing Stock (During Inflation) | Effect on COGS (During Inflation) |

|---|---|---|

| FIFO | Higher Closing Stock | Lower COGS |

| LIFO | Lower Closing Stock | Higher COGS |

| Weighted Average Cost | Balanced Closing Stock | Balanced COGS |

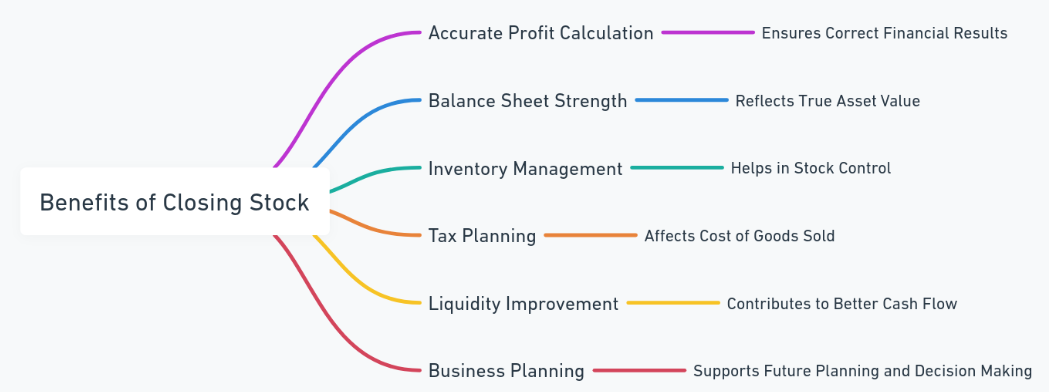

Benefits of Closing Stock

Accurate calculation of closing stock offers several advantages for businesses:

Accurate Profit Calculation

The closing stock value directly forms the COGS calculation that directly influences gross profit. Closing stock would often lead to different biases when overstated or understated, directly affecting profits- wrong calculations may lead to faulty financial decisions.

Inventory Management

There would be periodic measurement of closing stock, thereby maintaining the right amount of stock level. It would avoid overstocking situations because of increased storage costs as well as the danger of obsolescence. Conversely, it would keep away from stockouts, which would otherwise lead to lost sales.

Tax Benefits

Depending on the pricing method used, businesses can manage taxable income. For instance, using LIFO during inflationary periods lowers profits, thereby reducing the tax burden.

Financial Health Indicators

The closing stock value directly forms the COGS calculation that directly influences gross profit. Closing stock would often lead to different biases when overstated or understated, directly affecting profits- wrong calculations may lead to faulty financial decisions.

Strategies to Reduce Closing Stock

Managing and reducing closing stock effectively is essential for optimizing cash flow and minimizing storage costs. The following strategies can help:

1. Just-in-Time (JIT) Inventory: In a just-in-time inventory, the company orders the stock when it requires the stock. It decreases overstocked items. Subsequently, holding costs decrease.

2. Demand Forecasting: Demand forecasting accurately makes the businesses maintain a suitable level of stock that does not create an overstock, thereby avoiding excess buying and catering to their customers.

3. Promotions and Discounts: The discounted price or any promotion on a certain stock item helps it be sold earlier, thereby reducing close-out stock.

4. Inventory Turnover Ratio: The inventory turnover ratio tracks how fast the firm’s stock is getting sold. High turnover ratios are an indicator that the inventory is perfectly managed, but low turnover ratios indicate slow-moving stock.

Conclusion

The technique selected among FIFO, LIFO, and weighted average has implications for profitability and tax liabilities. An appropriate closing stock calculation ensures the right reporting of the cost of goods sold hence creating more creditable financial statements, but that effect spreads well beyond the accounting arena for proper stock management within techniques such as demand forecasting or JIT, which may reduce holding costs and optimize cash flows.

Calculate Closing Stock FAQs

What is the best method to calculate closing stock?

It depends on the business and market conditions. FIFO is preferable during inflation, while LIFO can reduce taxable income.

How does closing stock affect financial statements?

Closing stock is reported as an asset on the balance sheet and directly impacts COGS in the income statement, influencing profitability.

Can closing stock be negative?

No, closing stock cannot be negative. If a business sells more than its inventory, it is considered a stockout, not negative stock.

Why is accurate closing stock calculation important?

It ensures proper reporting of profit and tax liabilities and helps in maintaining optimal inventory levels for future sales.

How often should closing stock be calculated?

Closing stock is typically calculated at the end of a financial period, but businesses may also perform interim stock checks for better inventory control.