A HUF account is a special banking and taxation entity in India that allows a Hindu Undivided Family (HUF) to manage its financial affairs separately from individual members. Families can use this account to handle inherited wealth, run businesses, and enjoy tax benefits under Indian law. The meaning of the HUF account comes from Hindu law, which allows joint families to hold and perform financial activities as a single unit. HUF accounts have some features: they are subject to separate taxes and shared ownership and can operate independently of their members. Here’s what an HUF account is, how to open one, and the benefits offered by this account.

What is HUF?

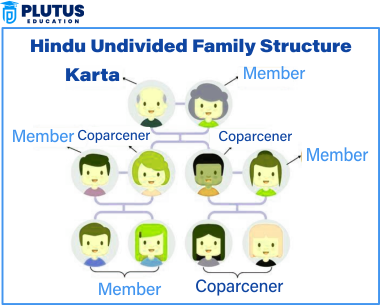

A Hindu Undivided Family, or HUF, is a legal body of common ancestry who own property together. A HUF is considered a separate entity in terms of financial books for tax purposes and the opening of separate accounts with banks. A HUF account is defined as the family being able to perform all its business activities under the name of HUF with a Karta at the helm of the family. The members of a HUF include the Karta, coparceners, and other family members.

HUFs can buy properties, invest in assets, and carry out business operations with special tax exemptions. The features of a HUF account differ from an individual account because it provides financial stability to families and helps them manage their wealth in a structured way. Many families prefer this system because it allows them to reduce tax liability while keeping wealth within the family.

Hindu families form the majority of HUFs. However, the Indian law permits Jains, Sikhs, and Buddhists to form a HUF too. A HUF exists until all the members decide to dissolve it. The HUF will continue functioning as a separate legal entity if no such agreement is reached. This legal structure helps the families pass down wealth through generations without complex inheritance issues.

Who are the Members of the HUF?

A HUF account in India consists of family members sharing ownership and financial responsibilities. The rights and roles of a family member depend on the family structure, which is why understanding the functioning of an HUF is crucial. Types of Members in a HUF:

Karta

He is the elder male member of the family. Technically, he heads HUF and makes all the monetary decisions. Karta also takes care of all the accounts running for the HUF. He behaves as a legal guardian for all the family members in the courtroom procedures. Yet again, control over assets and income is never an absolute holding of the personal property of HUF.

Coparceners

Coparceners include sons, daughters, grandsons, and great-grandsons who have equal rights in the ancestral property. They can demand the division of HUF property if necessary. Even though Karta manages the account, all coparceners share financial rights.

Members

The spouse of the Karta and other relatives are members of a HUF. They can have benefits from a HUF but do not own property rights. They cannot insist on partitions like coparceners.

HUF Account

The HUF account eligibility is based on the family’s birthdate. A new child automatically gets into the HUF, and daughters, even after marriage, can retain their coparcenary rights. However, a married woman can also be a part of her husband’s HUF. This structure makes sure that the financial burden falls upon the family members while the wealth remains in the family.

Documents Required to Open a HUF Account

Legal documents are required to prove the identity and existence of HUF when opening an account with the bank. This ensures the legal operation of HUF and all tax benefits. Proper documentation helps in smoother banking transactions as well as smooth taxation. The lack of such a document may even lead to the rejection of the bank’s application process. All paperwork ensures quick processing and, thereby, the activation of accounts without further delay.

HUF Deed

The HUF deed formally establishes the HUF and gives details of all members. It must state Karta’s role and confirm that all the family members agree to form the HUF. All coparceners and members of the family must sign the document. This is legal proof of HUF’s existence at the banking and tax levels; therefore, without this document, the banks and the tax authorities would not recognise HUF as an independent entity.

PAN Card of HUF

The HUF must have an independent PAN card to file income tax individually from its other members. In this case, the exemptions available under the Indian tax law can be availed by HUF, and, therefore, a PAN card will be issued after satisfying the Income Tax Department concerning the Deed of HUF and all other documents. A HUF cannot be legally enabled to earn income, make financial transactions, or invest in assets without a PAN. Furthermore, a separate PAN facilitates the HUF in deriving revenue advantages under different tax legislations through the allowance of deductions.

Proof of Identity of Karta

The Karta must present valid proof of identity, including an Aadhaar card, Passport, or Voter ID. Since Karta deals with all financial transactions, the bank verifies his identity before opening the account and allowing any operation. This document will ensure that only the right head of the family operates the account. It will also safeguard against fraud or misuse of funds by unauthorised people. Banks may demand additional identity documents if required.

Proof of HUF Address

The HUF should present valid address proof. This can be a rental agreement, utility bill, or property document that shows the HUF functions at a genuine place recognised by the tax authorities. Proof is required for communication purposes and tax returns. Banks will likely refuse to open the account if it is not submitted. Differences in address information might also delay approval.

Bank Statement of Karta:

Karta’s personal bank statement is required to verify financial history and credibility. It will help the banks verify Karta’s financial stability before opening his account. It validates a working banking relationship for the Karta. Additionally, it ensures responsible transactions on behalf of the HUF. At times, banks require statements for the last six months for proof.

HUF Seal and Stamp

Many banks require a HUF seal or stamp for all official transactions and documentation. The stamp is applied to financial documents and cheques issued from the HUF account. This way, the seal prevents fraud since only authorised signatures approve the transactions.

How to Form an HUF?

A HUF account must be formed before being activated as a financial body. This process, followed by the family, must be legal, along with all legal documents and tax registrations.

1. Formation of HUF

HUF enables families to maintain ancestral property and benefits from tax relief. This, in turn, ensures that HUF is identified in law and follows banking and taxation regulations. After this, the HUF can carry on its financial negotiations, such as purchasing properties or investing in any business.

2. Obtain PAN Card

The HUF should obtain a PAN card from the Income Tax Department to file taxes. Through PAN cards, the Income Tax Department can differentiate income between that of the HUF and its respective individual members. Tax authorities would need to trace the tax liabilities and benefits of the HUF. A PAN will ensure that the HUF can generate, invest, and thus conduct legitimate business. Taxes without separate PAN will attract penalty charges.

3. Open HUF Bank Account

It has to have an account in a bank to execute its transactions, investments, and business income. The Karta operates the account but operates in the name of the HUF. The bank requires identity and tax documents before opening the account. Using a HUF bank account helps families accumulate and administer rental income, profit from businesses, and other types of monetary inheritance. The HUF cannot maintain its financial accounts properly if a specific account in a bank does not exist for it.

4. Commence Transactions

With such a HUF account opened it would undertake all types of financial operations, from buying immovable property to trading in securities to handling the income of its business. Such a HUF account would get gifts and inheritances, and that money, too, may be preserved for growth with time. All transactions were to be accounted for by Karta, but every advantage would reach each group member. All such transactions would ensure the keeping of detailed records, which would ensure tax compliance.

5. Recording

The family must keep all income, expenses, and tax filings in the name of the HUF. Proper recording helps to be ready in case of tax audits and avoids potential legal wrangles. Well-maintained records help ensure that succession is not problematic if the Karta retires or dies. Proper bookkeeping can ensure smooth operations legally and discipline their finances. Failure to keep records will send them to a world of tax penalties and complexities.

How to Save Tax by Opening an HUF Account?

The savings for the family come in with a HUF account taxation strategy through income splitting and making deductions. Because it is treated as an independent legal entity, the HUF qualifies for exemptions and benefits under Indian tax laws. A family can strategise on using HUF accounts to minimise taxable income and maximise wealth. It will provide proper planning to the HUF so that it is tax-effective and strictly complies with all laws.

1. Separate Tax Identity

As HUF is treated as a different legal entity, it is allowed for other tax relief exemption limits. It means that HUF has an exemption from income tax just like individual taxpayers. Such benefits can be placed on a family, which is recovered by lowering their overall tax amounts. This ensures that a person can adapt the slab by keeping family income under the head of HUF. It helps in reducing taxes and does not violate the provisions of income tax laws.

2. Income Division

A Huf can divide its income between its members, which reduces tax liability on a person. The tax rates would be higher when the family’s total income is taxed in individual accounts.

This way of splitting income through a HUF lowers the effective tax rate. This will work best in families with more than one earning member. The correct splitting of income will maximise tax savings.

3. Section 80C Deductions

For taxes, the HUF can invest in tax-saving instruments like PPF, ELSS and life insurance. All these investments decrease the HUF’s tax liability. With 80C deductions, the tax burden can be legally reduced for families. It provides a good way of saving with growth in financial assets. Suitable planning does help in the adequate utilisation of all the available deductions.

4. Rental and Business Income

Now, if the profit is generated from any type of business and rental property if owned by HUF, that profit is separately charged. Due to this, personal income is low; hence, the total tax rate is also lower. The same HUF, registered for rental properties, can even earn regular incomes, which is tax-free. The section of the HUF also claims exemption under Income Tax. Through an HUF, financial activities can be maintained to manage wealth correctly.

5. Gifts and Inheritance

A HUF can receive tax-free gifts from family members. The investments are allowed for long-term growth. Gifts by direct family members are not subject to tax. The HUF continues to generate wealth without adding any extra tax liability. HUF rules cover the inheritance, too. This is the reason family wealth remains there for generations. But only when all these advantages are taken full care of by proper tax planning.

HUF Account FAQs

1. What is a HUF account?

A HUF account is a bank account opened in the name of a Hindu Undivided Family. It allows a family to manage its financial transactions separately from individual members. The Karta, the head of the family, operates the account on behalf of all members.

2. How do you open an HUF account?

The steps to open a HUF account are as follows: A HUF deed needs to be drafted, a separate PAN card is to be obtained, and Karta’s identity and address proofs will be submitted. All members have to agree to form the account. Once all documents are verified, the bank activates it.

3. What are the tax benefits of a HUF account?

An account under the HUF offers various benefits. The HUF is considered a separate legal entity and is not tax-chargeable as it would have been if an individual’s account had been opened. Family incomes can be distributed among family members; one can invest in schemes that save tax and avail deductions under 80C. This reduces the overall incidence of tax.

4. Can a HUF account be closed?

A HUF account can be closed if all members agree to dissolve the Hindu Undivided Family. The members must distribute the assets, and the HUF’s PAN card must be surrendered. The bank account should also be formally closed after settling all transactions.

5. How is a HUF account different from an individual account?

Compared to an individual account: a HUF is a joint financial entity, whereas an individual account relates to a single individual. A HUF accounts for tax benefits and shared ownership. A separate account provides greater flexibility and personal control. A HUF is perfect for family wealth management, while an individual account suits personal finances.