An audit assures an organization of financial visibility and accountability. It serves in detection of fraud, errors, and misstatements of financial records. However, though audits are effectively useful, these audits may also have certain restrictions in the way they can be performed, which limitations can be considered as inherent limitations of audits. No audit will ever be able to provide absolute accuracy since audits, rather than verify transactions, rely on evidence and judgment. Fraud risks, reliance on management information, and constraints of time and cost constitute the inherent limitations of audit. These conditions will not allow the auditor to give an assurance of 100 per cent accuracy in financial reports; thereby, businesses must maintain very strong internal control.

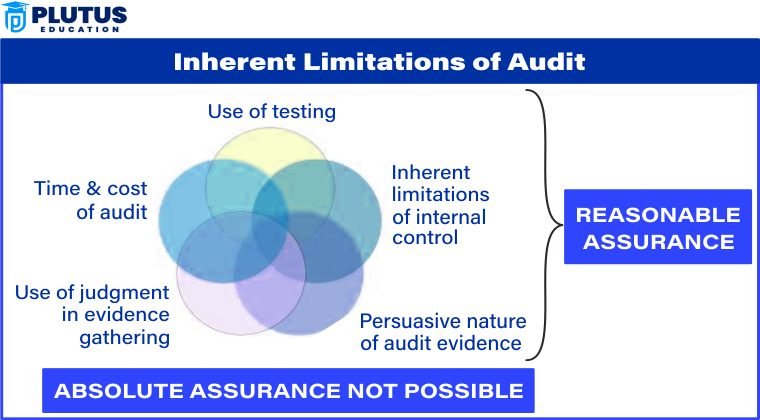

Inherent Limitations of Audit

Every audit has built-in limitations that make it not foolproof. Such audit limitations arise from sampling, estimates, and human judgment instead of total verification of every transaction. These limitations govern the extent to which audit reports may be relied on by businesses and investors alike.

Why Do Audit Limitations Exist?

Due to time, cost, and practicality constraints, audits cannot verify every transaction. Instead, sampling methods are used, which comprise selected proportions of transactions that stand for the whole. This technique is efficient, but it obviously cannot ensure the detection of all errors or fraud. Some irregularities would be present, which would not be detected since they were not included in the sample.

Further, auditors rely on management-provided data and estimates as financial sources. If the management misrepresents or delivers incorrect information on records, auditors are more likely to miss such deception. Therefore, this dependence on internal sources gives rise to crucial limitations in audit accuracy since auditors cannot verify every entry in financial statements themselves.

How Audit Limitations Impact Businesses and Investors?

There are restrictions to an audit that must lead an investor or business to not place full credibility on audit evidence in making its decision. Audits may provide reasonable assurance, but some risks of fraud and misrepresentation cannot be fully mitigated. Hence, such stakeholders should treat the audit report as one of several aider instruments on which to base their acceptance of financial integrity, rather than as the ultimatum.

Investors should realize that an audited financial statement is not a promise of future profitability or success in a business. Likewise, companies should set up good internal controls in addition to the audit process to create a more accurate and reliable financial report. Such controls may help mitigate risks not captured by audits relating to fraud and errors.

Significant Cons of Audit Every Business Has to Know

Although audits increase the financial credibility of an organization, the costs also accompany some disadvantages. The different disadvantages that exist regarding audits must be learned by businesses to know their limitations in managing financial risks perfectly.

Limited Scope of Verification

The audit’s most significant setback is that it relies entirely on sample testing rather than complete verification. Auditors select only a portion of the transactions to be reviewed and assume that it would consider the total financial data; however, in case of fraud happens beyond such selected sample, it cannot be detected. For example, discrepancies will go unnoticed since the company manipulates whole transaction areas not being audited.

Hence, this is just an audit which breaks its efficiency in identifying prominent fraud schemes. Thus, never believe that every financial anomaly is detected by an audit because, like magic, it never replaces an entire forensic investigation.

Management Dependence Representations

Generally, auditors take the financial records, documents, and explanations the management provides. Suppose management fakes such data or provides misleading information on it. In that case, the auditors do not verify such a significant risk as they do not have unlimited access to verify each transaction independently.

For example, a company suffering financial distress may overstate its revenue to appear more profitable. If auditors cannot cross-check every revenue source independently, they may accept these figures as accurate. This dependence on data management may compromise audit quality, which is why businesses need ethical financial reporting practices.

Cost and Time Constraints

Audits usually require huge funds and human resources. Small firms have external costs that might be difficult to cover when hiring outside auditors. They take a long time, thus delaying financial reporting and keeping the whole business moving.

For example, an external audit will require an organization to allocate some of its employees to assist auditors, thus halting normal operations for some time. These costs and delays may result in operational inefficiencies, making audits financially and administratively burdensome. Nevertheless, they need an audit to maintain transparency and compliance with the law.

Why Are External Audits Limited?

Independent professionals do external audits to ensure unbiased financial reporting. Yet with independence, the limitations of external audits still exist, which can never make them a hundred percent foolproof.

External Audits are Not Foolproof

External auditors would work with a limited timetable and budget. Hence, they can’t get to verify every single transaction. They would rely on what management gave them as available and accurate financial records. If these records were incomplete or manipulated, the audit would not discover them. Additional limitations include confirmations from banks and other third parties, as they pay to confirm the veracity of transactions. If an external auditor then had garbled misleading information from such confirmations, the audit would not “see” discrepancies outside of them. This renders said audit less reliable and more biased toward missing financial frauds that can hide quite well.

Challenge of Detecting Fraud and Errors

Fraudulent transactions are usually attempted to be put to look stingingly real; thus, they don’t find these easily. For the most part, they wouldn’t know that there’s a fraudulent scheme going on, are past financial data rather than current examples for an external auditor.

For instance, a company may create fancy ways to show more profit without breaching an accounting standard. External auditors may have trouble differentiating between acceptable financial tactics and dishonest ones. Hence, such audits are not efficient in finding sophisticated frauds.

Limited Scope of Responsibility

External auditors are to see that the financial statements are accurate and by accounting standards; that role does not extend to anything else regarding the financial statements. External auditors are interested in anything outside the economic picture, such as operational efficiency, business risk, or future financial performance.

An example is that an auditor might show that a company’s financial records satisfy legal standards but will not want to guarantee whether the company will be profitable. This reduces the overall usefulness of external audits for long-term business decision-making.

Inherent Limitations of Audit FAQs

1. What are the intrinsic limitations of audit?

Inherent limitations of an audit include dependence on sampling, management representation, and time constraints; auditors can’t look into and examine every transaction or predict future financial conditions. Though the audit will never be perfect, it is valuable for financial transparency.

2. What other limitations have an external audit?

These limitations of external auditing result from limited access to internal data, time constraints, and third-party confirmation. External auditors can provide reasonable assurance, but they cannot ensure the nonexistence of some fraud or misstatement.

3. How do audit risk factors affect accuracy?

Audit risk factors such as inherent risk, control risk, and detection risk affect the reliability of financial reports. These risks may lead to undetected errors, misstatements, and incorrect conclusions in financial regarding the company.

4. What is an audit disadvantage for organizations?

The disadvantages of audits include high costs with top time consumption, dependence on information provided by management, and the inability to detect every financial fraud. Audits are critical and valuable to the extent that they impart credibility to the financial statements.

5. What are some common audit challenges?

Complex financial transactions, changing fraud techniques, regulatory pressures, and limitations in detecting well-concealed financial misstatements may also pose challenges for an auditor. Therefore, auditors should constantly upgrade themselves to make auditing more accurate.