Auditing is going through financial reports, operations, and systems to achieve accuracy, adherence, and efficacy. Limitations of auditing refer to the restrictions and limitations that the auditors encounter while inspecting the financial statements. Despite its effectiveness in ensuring correctness and conformity, certain demerits include reliance on samples, human errors, and management’s influence. All frauds can’t be traced through auditing, and auditing cannot verify total financial accuracy. Here, we will discuss what auditing is, its advantages and main limitations are, and in which form and how much auditing companies undertake.

What is Auditing?

Auditing regularly involves examining an organisation’s financial records, statements, and internal controls for accuracy, compliance, and transparency. They verify that monetary transactions are in order, test controls, and ensure that financial reports provide an accurate and fair view of the company. The audit process involves collecting evidence, reviewing finance records, and writing an audit report on conclusions.

For example, a manufacturing company utilises an external auditor to audit its accounting records to ensure that all financial statements are aligned with accounting principles and legal compliance.

The individual who performs this audit is referred to as the auditor. The auditor doesn’t ensure that the book of accounts is error-free. Instead, he expresses his opinion regarding the book’s accuracy. An Auditor does not predict or comment on the book’s performance, nor does he predict the next financial year’s performance.

Advantages of Auditing

The advantages of auditing render it an indispensable instrument for companies, investors, and regulatory agencies. It enhances the accuracy of finances, increases credibility, and enables organisations to identify and prevent fraud.

Ensures Accuracy of Financial Statements

Audits ensure that financial reports present a true and fair view of an organisation’s financial position. As a result of this process, all transactions will bring craziness in also to keep transparency in financial reporting. Audits provide credibility to statements that enhance the trust of stakeholders such as investors, creditors, and regulators. For this reason, it is imperative to issue clear and accurate financial statements to make informed decisions and to preserve reputation.

Detects and Prevents Fraud

Auditing helps to find frauds, errors and accounting irregularities. Audits allow one to scrutinise financial records and systems, helping to detect fraud or errors that could go undetected. The only thing stronger than a good audit is the fraud it prevents. Companies with intense audits are at lower risk for fraud and are better able to detect suspicious activity early, reducing the risk of substantial loss of revenue and reputation.

Improves Internal Controls

An internal audit evaluates the effectiveness of a company’s internal control mechanisms. They find weaknesses and recommend avoiding errors, fraud, and mismanagement. Implementing financial controls is just as relevant for companies handling advanced data, such as those in big tech or pharmaceuticals. Auditing secures the organisations to keep a sound monetary system which leads to securing their property and providing accurate reporting.

Boosts Investor and Stakeholder Confidence

Investors and lenders use audited financial statements to assist them in making investment and credit decisions. Companies that have regular audits are inherently more trustworthy and stable. Audits give credible information regarding the company’s financial sustainability, which boosts investors’ confidence. Acquiring this level of stakeholder trust leads to more significant investment opportunities for the company.

Ensures Compliance with Laws and Regulations

Audits ensure that a corporation abides by tax laws, fiscal policies, and corporate laws. They help ensure compliance with laws and regulations, minimising the risk of penalties and fines. Regular audits ensure that companies remain on the same path as everyone else, per industry standards and legal frameworks, meeting government requirements and avoiding catastrophic legal issues, leaving their operations humming, compliant and profitable.

Enables Business Expansion and Loans

A bank or financial institution helps arrange audited financial statements for loan or credit approval. A clean audit report signifies healthy finances, which boosts the company’s credit image. It’s critical in getting loans, the interest of an investor, and business development overall. Companies with verifiable finances are more credible and have a better chance of accessing appropriately priced loans and financing.

Helps in Decision-Making

The management utilizes the audit findings to make better-informed decisions that impact finances and operational efficacy. Audits highlight opportunities such as cost control, revenue opportunities, and realms for improvement. The steps taken in a full review of financial records enable businesses to identify trends and challenges that affect operations and yield insight that can refine strategic planning efforts and secure long-term sustainability.

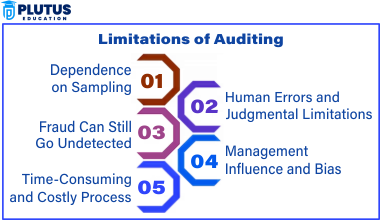

Limitations of Auditing

Though an audit is helpful, some limitations can affect the success of the process. These limitations derive from time constraints, sampling, and human error.

Dependence on Sampling

Auditors use sampling, not reviewing every transaction. Although sampling is an efficient way to examine financial data, there is the possibility that the selected sample does not completely capture the entire set of economic data. A sample selection that is not representative may cause errors or fraud to go undetected, affecting the overall accuracy of the audit results.

Human Errors and Judgmental Limitations

Particularly since audit is a judgement-based profession, mistakes are not uncommon. These decisions are made based on the auditor’s experience and interpretation of data. A misinterpretation of financial data or an error of judgment by the auditor may lead to inaccurate audit conclusions and affect the reliability of the audit report.

Fraud Can Still Go Undetected

Although this is audited in detail, fraud can remain undetected, mainly when it employs clever mechanisms, such as forged documents, or when two (or more) employees collude against the organization. Auditors look for discrepancies in financial records but do not look for criminal intent. Due to this limitation, more complex fraud schemes may avoid detection during the audit process.

Management Influence and Bias

Sometimes, management influences the audit process by withholding or manipulating financial data to mislead auditors. Auditors are vulnerable to bias because they often contextualise their review with management’s input. Missing or fabricating data, if done deliberately by management, could skew the results of the audit, which would skew the conclusion about the company’s financial health.

Time-Consuming and Costly Process

Auditing is a labour-intensive, time-consuming exercise requiring considerable financial and human resources. Auditors require time to scrutinize financial records, investigate transactions and evaluate controls properly. Hiring external auditors can be costly for small businesses and can be challenging to afford. That does not allow smaller companies to have periodic audits, which is vital to ensure financial accuracy and compliance.

Auditing FAQs

1. What is auditing?

Auditing is the examination of financial statements to verify accuracy, compliance, and transparency.

2. What are the primary limitations of auditing?

The primary limitations of auditing are sampling errors, fraud risks, management influence, human judgment errors, and high costs.

3. Why is audit of limited companies significant?

Audit of limited companies provides financial transparency, investor confidence, and legal compliance.

4. What are the various types of audit?

The audit categories are internal audit, external audit, tax audit, performance audit, and compliance audit.

5. How can businesses overcome audit limitations?

Businesses can enhance internal controls, embrace improved audit techniques, and employ technology to make audits more accurate.