Audit evidence refers to the facts obtained by auditors to authenticate the validity and correctness of the financial statements. Methods of Obtaining Audit Evidence describes the procedure for gathering. Checking financial details to conclude an opinion about a business company’s accounts. Audit evidence plays a major role in helping ascertain whether books of accounts are valid and agreeable with GAAP. Auditors apply various methods to obtain consistent data, including inspection, observation, inquiry, and analytical procedures. This article will delve into audit evidence, its significance, and different ways of getting it.

What is Audit Evidence?

Audit evidence is the data that auditors gather to determine whether a firm’s financial reports are accurate, complete, and comply with accounting rules. It forms the basis for an auditor’s opinion.

Characteristics of Audit Evidence

An auditor relies on various forms of evidence to ensure that an element of a transaction is recorded correctly on a company’s financial statements.

- Sufficiency: The evidence is sufficient to support the auditor’s opinion on the financial statements. The evidence gathered is supposed to be done in all material areas and should provide a true and fair view of the company’s financial position. The auditor’s report is based on opinion, and if there is insufficient evidence, the auditor cannot reasonably form an opinion, which could impact the audit’s integrity.

- Relevance: To ensure that audit evidence is appropriate, it must be directly related to the items in the audited financial statements. The evidence must be relevant to the exact portions of the company’s financial records being investigated. Relevant evidence allows auditors to develop an accurate and fair opinion of the financial statements.

- Reliability: Audit evidence needs to be reliable, with external sources of evidence usually having higher trustworthiness than internal records. External evidence from suppliers, customers, and banks is more challenging to manipulate. Having reliable evidence gives certainty that the financial statements are free of errors.

- Timeliness: Audit evidence should be related to the period under review. However, any stale information may be misleading since it does not represent the company’s financial condition. So, the company maintains its information flow, and the accountant auditor can consider that to provide timely evidence.

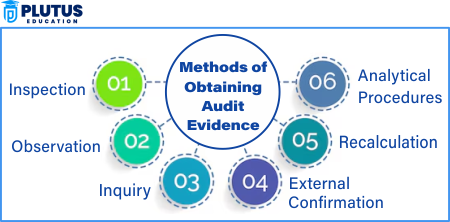

Methods of Obtaining Audit Evidence

The auditors use different methods to gather and assess the audit evidence. These practices help maintain accurate and reliable financial information reported by a company.

Inspection

Physical documents, assets, or records are inspected to determine their existence. Auditors go through invoices, contracts, bank statements, receipts, etc. See also physical verification of inventory, fixed assets, and cash balances. This enables auditors to identify mistakes, fraud , and misrepresentations in financial documents, revealing that the company’s financial records are complete and accurate. Examining invoices doubles-checking the revenue that is being reported to make sure it is correct, checking that the fixed asset register has everything in it.

Observation

Observation includes auditors directly observing how company staff performed particular processes or procedures. For example, during stock verification, auditors might be present to witness the process of counting the inventory or to observe staff receiving cash to ensure compliance with internal controls. This approach enables auditors to verify that employees follow the correct procedures and guidelines. Real-time actions allow auditors to see how effective the internal controls are and where weaknesses may lie. Adding to this are the checks and balances that are obvious, such as watching employees count inventory which keeps the inventory records accurate.

Inquiry

Inquiry means questioning and asking for explanations from employees and management within the company. Auditors then ask accountants, managers and staff to explain what certain transactions are and to identify any discrepancies. They can be oral or in writing, with inquiry letters where auditors ask to confirm unusual or suspicious actions. It helps auditors explanations for discrepancies in financial records and the reasons behind unexpected trends in current data..

External Confirmation

Confirmation from external parties, eg, banks, suppliers, and customers. This is why auditors ask for confirmation letters from banks when they want to confirm balances of cash on hand, as well as supplier statements when they want to confirm accounts payable. This approach yields highly reliable evidence that is independent of the financial statements. Confirmations include bank confirmation letters to verify cash balances, and supplier statement confirmations to verify outstanding liabilities.

Recalculation

Recalculation requires auditors to check that the numbers in financial records add up correctly. Auditors will recalculate key figures such as depreciation expenses, interest calculations, and payroll amounts to confirm they match supporting documents. This process ensures the accuracy of financial information, minimizing errors. Auditors verify that depreciation expenses have been set correctly over time by recalculating depreciation expenses. In a similar way, verifying for tax calculations helps ensure that tax coverage is calculated accurately.

Analytical Procedures

Analytical procedures are the process of analyzing financial data to discover patterns, trends, and ratios that may indicate irregularities or mistakes. Auditors review financial information from the current year with previous years for predictive variation and apply analytical procedures, such as gross margin and debt-to-equity ratios. This approach assists auditors in identifying certain unusual trends and potential misstatements in financial records. Auditors can detect inconsistencies in financial data period to period through comparison, which leads to further investigation and the identification of areas that need to be corrected or scrutinized further.

Types of Audit Evidence

Audit evidence refers to the information gathered by auditors to assess whether the financial statements are free of material misstatements. Evidence types include physical, documentary, testimonial, computational, and analytical evidence, each performing a critical function in achieving financial accuracy and compliance.

Physical Evidence

Examples of physical evidence are assets, inventory, and documentation that auditors are able to confirm through inspection. This evidence is collected by observation, for example, through observation of inventory counts or fixed assets. This confirms to auditors that the company’s assets both exist and are accurately recorded. Auditors visualize the physical evidence to ensure that no discrepancies exist and that financial reporting is correct.

Documentary Evidence

When auditors review, this angers documentation evidence regarding invoices, contracts, bank statements, and financial records. These forms are essential for transaction verification and building accurate financial statements. Auditors do this by verifying these records, ensuring reported activities such as sales or purchases are real. Backed up by appropriate documentation. A piece of documentary evidence is essential to detect any misstatement. error That occurred in the financial record.

Testimonial Evidence

Testimonial evidence information auditors obtain from employees, management, or third parties. This evidence assists auditors in understanding the workings of a company. Explaining any irregularities in financial statements. Interviews or written confirmations provide information about the company’s financial practices. Testimonial evidence can be instrumental in validating information and corroborating other audit evidence obtained.

Computational Evidence

Financial Analysis Auditors might recalculate figures for depreciation, interest, or payroll. Checking the accuracy of those data points. This evidence contributes to proving the mathematical accuracy of the financial statements. Auditors check these calculations to identify errors or discrepancies that could impact the overall accuracy of the financial records.

Analytical Evidence

Comparative, trend and ratio analyses yield analytical evidence. Compare performance to prior periods or industry benchmark. To analyze financial data for auditors. Such data points could be unusual patterns, changes or discrepancies that merit further analysis. With analytical evidence, auditors can not only evaluate a company’s financial condition. But also identify potential misstatements or fraud.

Audit Evidence FAQs

1. What is audit evidence?

Audit evidence is the information that auditors gather to confirm the fairness and accuracy of financial statements.

2. What are the characteristics of audit evidence?

Characteristics of audit evidence are sufficiency, relevance, reliability, timeliness, and objectivity.

3. What are the different types of audit evidence?

Types of audit evidence are physical, documentary, testimonial, computational, and analytical evidence.

4. How do auditors obtain audit evidence?

Auditors employ inspection, observation, inquiry, external confirmation, recalculation. Analytical procedures to obtain audit evidence.

5. Why is audit evidence important?

Audit evidence provides financial accuracy, assists fraud detection, affirms audit opinions, and establishes investor trust.