Micro environment factors are significant in auditing as they impact financial evaluation, compliance, and risk assessment. Examples of such factors are clients, competitors, suppliers, regulatory agencies, and stakeholders directly affecting the auditing process. Recognizing these factors allows auditors to assess financial health, determine risks, and validate reporting accuracy. The micro environment is distinct from macro environmental factors in that it concerns internal and near external forces on an organization’s auditing system.

What is Micro Environment?

Micro environment in audit is the internal and external factors that directly impact an organization’s financial audit. They consist of company policies, competition in the market, client operations, relationships with suppliers, and legal rules. Auditors evaluate these factors to guarantee adherence to accounting principles and financial openness.

The micro environment in the audit consists of limited but related factors that serve its purpose specifically. Audit procedures are determined by internal company policies, and financial risks are determined by how the client does business. Regulatory burdens ensure conformity to economic guidelines. Companies’ valuations depend on competition between different platforms, and the reliability of transactions builds on relationships with their suppliers. Hence, auditors must examine these factors in-depth for the financial statements to be correct and the risk controls to function properly.

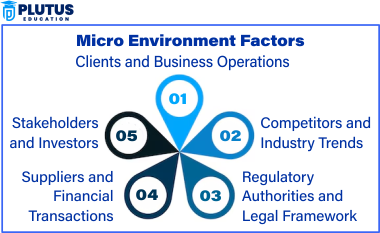

Micro Environment Factors

The micro environment factors in auditing directly impact financial reporting, risk assessment, and compliance. Several factors determine audit procedures: external clients, regulators, investors, and suppliers, and these shape the level of business transparency. Get to know the key micro environment elements auditors must scrutinize for accurate financial assessments.

Clients and Business Operations

It is essential to audit clients because they provide financial data and records. A company’s business model and financial transactions determine how complex an audit will be. A company’s financial position affects how an audit function operates. Risk and materiality judgments of its financials change as needed.

Competitors and Industry Trends

The sector’s competition is the main part of the environment in auditing. Auditors scrutinize a company’s financial performance against its industry peers to look for unusual trends or discrepancies. Market conditions and industry trends influence financial risks, eventually impacting how auditors assess materiality and financial stability or amend their compliance with financial regulations.

Regulatory Authorities and Legal Framework

Business regulations are what government agencies write on laws for financial reporting audits & Friedman and Goodman (1997). It is time to evolve with the latest rules, laws, regulations, and audit guidelines. After all, the accounting industry is no exception in this era. Upholding financial laws can help you escape penalties and legal repercussions, and added auditor scrutiny compliance is a central factor in financial audits.

Suppliers and Financial Transactions

The vendor relationships of a company impact the financial transparency, cash flow, and procurement audit. Auditors examine contracts with suppliers, pricing agreements, and outstanding liabilities. In fraud detection, one verifies procurement transactions, payment cycles, and suspicions between a business and its suppliers.

Stakeholders and Investors

Investors use these audited financial statements to make smart investment decisions. They maintain that auditors provide financial reporting transparency, accuracy, and accountability. Strong corporate governance is the backbone that creates stakeholder trust and makes the business credible by showing that what the company reports in its financial statements are its financial health and operations.

Impact of Micro Environment Factors

These micro environment factors are major in auditing, affecting financial reporting, risk assessment, and compliance. These elements influence the design of audit procedures and play significant roles in determining the actual cost of doing business and in ensuring transparency, stakeholder confidence, and operational efficiency. Micro environment Factors affecting the auditing process

- Audit Risk Assessment: The influence of the macro and then micro environment dimensions on marketing also impacts financial reporting. Recording and verification of financial transactions beforehand enhance reporting accuracy. Auditors check if financial statements conform to accounting standards.

- Industry Assessment: More competition and complex financial transactions lead to audit risk. The degree of financial analysis is affected by regulatory scrutiny. Assessing business operations identifies risks ahead of reporting.

- Regulatory Compliance: Auditors help businesses stay in line with their local laws. Updated regulatory frameworks have an impact on audit methodologies and reporting structures. Failure to comply could lead to reputational damage and legal repercussions.

- Stakeholder Confidence and Business Stability: Stakeholders rely on audited financial statements to make investment decisions. To build trust in business, auditors keep the financial disclosures as transparent as possible. Fraud risks are reduced with ethical audits and corporate governance strengthens.

- Operational and Financial Efficiency: Audits facilitate better financial control in businesses. Improve cost management through the detection of supplier transaction discrepancies. Auditors scrutinize the efficient allocation of financial resources.

Relevance to ACCA Syllabus

Micro environment factors include customers, suppliers, competitors, and stakeholders. And they directly impact financial management and corporate decision-making. So, in ACCA’s Strategic Business Leader (SBL) and Financial Management (FM) papers, they need to have an understanding of how companies examine these elements and how they play a part in the direction of the business, the evaluation of its performance and the financial decisions that it makes.

Micro Environment Factors ACCA Questions

Q1: Which of the following is NOT considered a micro environment factor affecting a business?

A) Customers

B) Suppliers

C) Political stability

D) Competitors

Ans: C) Political stability

Q2: Why are suppliers considered an important micro environment factor?

A) They determine the company’s tax obligations

B) They affect the cost and availability of raw materials

C) They establish internal control policies

D) They regulate business operations

Ans: B) They affect the cost and availability of raw materials

Q3: How can competitors influence a company’s micro environment?

A) By setting international trade policies

B) By affecting pricing strategies and market positioning

C) By determining the country’s GDP growth rate

D) By enforcing financial reporting standards

Ans: B) By affecting pricing strategies and market positioning

Q4: What is the role of customers in the micro environment of a business?

A) Customers regulate financial reporting requirements

B) Customers impact demand, revenue, and market trends

C) Customers set labor laws and employment policies

D) Customers control the company’s inventory levels

Ans: B) Customers impact demand, revenue, and market trends

Relevance to US CMA Syllabus

Analysis of micro environment is part of its syllabus in Strategic Management and Performance Management topics for US CMA. Management accountants must comprehend how internal and external stakeholders, industry competition, and market dynamics influence budgeting, cost control, and business sustainability.

Micro Environment Factors US CMA Questions

Q1: How do suppliers impact cost management in a company’s micro environment?

A) By controlling government taxation policies

B) By influencing production costs and supply chain efficiency

C) By determining exchange rate fluctuations

D) By approving the company’s financial statements

Ans: B) By influencing production costs and supply chain efficiency

Q2: A company faces strong competition in its industry. What strategic decision should management consider?

A) Increasing financial reporting regulations

B) Implementing competitive pricing and product differentiation

C) Reducing internal audit procedures

D) Ignoring customer feedback

Ans: B) Implementing competitive pricing and product differentiation

Q3: Why should a company consider its customers in micro environment analysis?

A) Customers dictate company laws and tax policies

B) Customers impact sales, brand loyalty, and market share

C) Customers decide on the company’s dividend policy

D) Customers regulate employee performance reviews

Ans: B) Customers impact sales, brand loyalty, and market share

Q4: What should management do if a company’s main supplier increases prices?

A) Increase product prices, seek alternative suppliers, or negotiate better terms

B) Reduce the quality of products without informing customers

C) Delay financial reporting to avoid recognizing higher costs

D) Close down business operations immediately

Ans: A) Increase product prices, seek alternative suppliers, or negotiate better terms.

Relevance to US CPA Syllabus

Micro environment factors play a central role in risk management and business strategy, which fall within the Business Environment and Concepts (BEC) segment of the US CPA exam. CPAs must assess how regulators, competitors, customers, and suppliers affect corporate governance, business performance, and financial reporting.

Micro Environment Factors US CPA Questions

Q1: Which of the following is a key characteristic of the micro environment?

A) It includes uncontrollable external factors like inflation and currency fluctuations

B) It focuses on the immediate operational factors affecting business decisions

C) It excludes customer and competitor analysis

D) It determines long-term government policies

Ans: B) It focuses on the immediate operational factors affecting business decisions

Q2: What is the potential risk of supplier dependency in a company’s micro environment?

A) The company may have increased pricing power

B) The company may face supply chain disruptions if the supplier fails

C) The company will have to comply with international labor laws

D) The company’s financial reports will no longer be required

Ans: B) The company may face supply chain disruptions if the supplier fails

Q3: How can a company respond to a shift in customer preferences?

A) By maintaining its current product offerings without change

B) By adjusting product features, marketing strategies, or pricing models

C) By ignoring customer feedback and focusing only on financial performance

D) By reducing supplier costs without affecting product quality

Ans: B) By adjusting product features, marketing strategies, or pricing models

Q4: Why are competitors important to a company’s micro environment?

A) Competitors influence business decisions by creating market competition

B) Competitors control government regulations and tax policies

C) Competitors have no impact on business operations

D) Competitors dictate a company’s internal financial decisions

Ans: A) Competitors influence business decisions by creating market competition

Relevance to CFA Syllabus

CFA candidates learn micro environment variables under financial analysis and Corporate Finance. Knowledge of customer behavior, competition in the industry, and supplier dynamics is essential for investment decision-making, economic modeling, and equity valuation.

Micro Environment Factors CFA Questions

Q1: How does a company’s micro environment impact financial performance?

A) It affects costs, revenue, market competition, and consumer demand

B) It has no impact on financial decision-making

C) It determines global interest rates and exchange rates

D) It influences only external economic factors

Ans: A) It affects costs, revenue, market competition, and consumer demand

Q2: A financial analyst evaluating a company’s stock must consider micro environment factors such as:

A) Interest rate policies set by the Federal Reserve

B) The company’s customer base, suppliers, and industry competition

C) The country’s inflation rate and GDP growth

D) International currency fluctuations

Ans: B) The company’s customer base, suppliers, and industry competition

Q3: If a company loses its largest supplier, what financial risks might it face?

A) Higher production costs and potential supply chain disruptions

B) No financial risks, as suppliers do not impact financial performance

C) Immediate government intervention to control prices

D) A decrease in global GDP

Ans: A) Higher production costs and potential supply chain disruptions

Q4: Why is competitor analysis important in micro environment evaluation?

A) It helps a company identify market trends, pricing strategies, and potential risks

B) It eliminates all business risks associated with market fluctuations

C) It prevents a company from expanding its operations

D) It forces competitors to reduce their market share

Ans: A) It helps a company identify market trends, pricing strategies, and potential risks