Modified internal rate of return (MIRR) is a metric that deviates from the ordinary IRR. However, with MIRR, cash flows would be reinvested at the firm’s cost of capital instead of the IRR itself. It makes MIRR a realistic sum of project profits. MIRR can address the IRR drawbacks while providing a simple, accurate value concerning its financing and reinvestment assumptions.

MIRR is one of the most widely used capital budgeting metrics because it enables comparison of investment alternatives. It allows a more reflective and effective decision-making procedure by ensuring the reinvestment of cash flows at a reasonable rate. Financial management on MIRR equips businesses to bolster their investment-efficient strategies. The article highlights the meaning of MIRR, the MIRR formula, the calculation mechanism, advantages, and comparatives with other investment-related metrics like IRR and NPV.

Modified Internal Rate of Return (MIRR)

Modified internal rate of return is a financial metric indicating the profitability of an investment, taking care of the constraints of traditional IRR. It is based on the principle that when the positive cash flow from the investment happens, it is reinvested at the firm’s cost of capital; when there is an initial cash outflow from the investment, such outflow would have been financed at the firm’s financing rate. Compared to IRR, wherein reinvestments are assumed at IRR, MIRR gives a more accurate measure of an investment’s return.

MIRR is an integral part of investment analysis because it provides a single rate of return reflecting both the financing cost and the reinvestment possibility. This approach avoids the obstacle of multiple IRR values that materialize in nonconventional cash flow projects and provides a more real-world profitability assessment. Hence, businesses use MIRR as a capital budgeting decision tool to determine which projects are the most profitable investments.

MIRR gives a single rate of return, which is indicative of the financing cost and the reinvestment opportunity, thus not leading to misleading results that arise from the use of the IRR. Therefore, a much-seeded portrayal of profitability can be given. Another reason for the preference of many investors and financial managers is the assumption of MIRR regarding reinvestment cost, which could better be a reality under economic conditions.

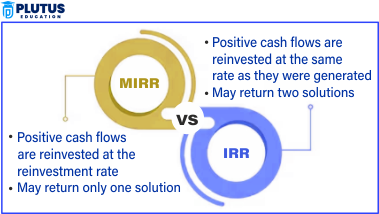

MIRR Vs. IRR

While MIRR and IRR can be used to measure the returns on investment, they contain various assumptions, implications, and levels of accuracy. Understanding MIRR Vs. IRR makes selecting the best financial analysis technique easy for any investor.

The fundamental difference between MIRR and IRR depends on the assumptions of reinvestment. An IRR reduces interim cash flows itself at that IRR. This can become highly unrealistic in the case of MIRR reinvesting at their respective firm’s cost. Thus, MIRR becomes a more realistic metric.

| Feature | IRR (Internal Rate of Return) | MIRR (Modified Internal Rate of Return) |

| Reinvestment Rate | Assumes cash flows are reinvested at the IRR. | Assumes cash flows are reinvested at the cost of capital. |

| Multiple IRRs | Possible in nonconventional projects, leading to confusion. | Eliminates the issue of multiple IRRs. |

| Accuracy | It can be misleading due to unrealistic reinvestment assumptions. | Provides a more realistic measure of return. |

| Capital Budgeting Use | Less reliable for ranking investment projects. | More reliable for investment ranking and decision-making. |

MIRR is preferred in financial analysis because it provides a single, realistic return rate, whereas IRR can give multiple values, making investment decisions complicated.

IRR can sometimes overstate profitability by assuming an overly optimistic reinvestment rate. This can result in erroneous investment decisions. The MIRR rectifies this by using a more realistic reinvestment tear-off, which indicates earning more accurate return results. Besides, it is firms that, apart from precise ranking of projects, derive maximum benefits from applying the MIRR rather than the IRR.

MIRR Formula

The Modified Internal Rate of Return (MIRR) improves upon the traditional IRR by addressing its limitations. It considers both the cost of investment and reinvestment rate, providing a more accurate measure of profitability.

Where,

- FVCF = Future cost of the positive cash flows after deducting the reinvestment rate or cost of capital:

FV = ∑

Here, Ci is the positive cash flow, and RR is the reinvestment rate

- PVCF = The present cost of the negative cash flows after deducting the finance cost of the firm:

PV = C₀ – ∑

Here, C0 is the negative cash flow, and FR is the finance rate

- n is the number of years

Calculating the Modified Internal Rate of Return manually using the formula could be difficult and result in errors. Therefore, financial firms and stock dealing companies use spreadsheet applications like Microsoft Excel to assess the return on investments. The MIRR Excel function is:

= MIRR (value_range, finance_rate, reinvestment_rate)

Where,

- Value range = The range of cells containing cash flow values from each period

- Finance rate = The cost of capital of the firm or interest expense during negative cash flows

- Reinvestment rate = Compounding rate of return on the reinvested positive cash flow

Examples of Modified Internal Rate of Return

Let us consider the following MIRR example with calculations to understand the concept better:

Example 1

A company invested $1,000 for a project, expecting returns in cash worth $300, $600, and $900 for three consecutive years. The cost of capital and the reinvestment rate was 12%. Hence –

FV = 300 * (1+0.12)2 + 600 * (1+0.12)1 + 900

= (300 * 1.25) + (600* 1.12) + 900

= 375 + 672 + 900

= 1947

PV = 1000

Using Modified Internal Rate of Return formula:

= 24.87%

Example 2

A company invests $1,800 and evaluates the return worth $500 to be consistent for the next three years with an additional profit of $500 at the end of the third year. What is the difference between the project’s IRR and the Modified Internal Rate of Return if the reinvestment rate is 10% and the IRR is 12%?

FV = 500 * (1+0.10)2 + 500 * (1+0.10)1 + 1000

= 605 + 550 + 1000

= 2155

PV = 1800

= 6.18%

The difference between the IRR and Modified Internal Rate of Return is equal to = (12 – 6.18) %

= 5.82%

MIRR gives a clearer picture of project profitability by considering the cost of financing and reinvestment assumptions.

This example shows how MIRR corrects IRR’s unrealistic assumptions. If we used IRR, the reinvestment rate assumption would likely be much higher, leading to an inflated return percentage. Businesses can make investment decisions using MIRR based on a more achievable return expectation.

Advantages of MIRR

The modified internal rate of return (MIRR) is one of the most popular means of evaluating capital budgeting projects because it provides a more accurate and reliable gauge of the profitability of a given project. The IRR assumes that all cash flows occurring before the final cash flow are reinvested at the IRR. Instead, MIRR is more realistic, using the firm’s cost of capital as its reinvestment rate, which makes it more practical from the point of view of financial decision-making. By eliminating multiple IRRs and doing away with irrational reinvestment assumptions, the MIRR gives greater assurance to firms in evaluating and comparing investment projects. The most essential advantages of MIRR are:-

100% Surety of Not Having Multiple Solution Values

One of the disadvantages of the internal rate of return is that, in the case of projects with unconventional cash outflows, it may calculate multiple IRR figures. This sometimes makes understanding the actual profit such a project can generate difficult. MIRR does not have this issue because it guarantees a single unambiguous return on the project, significantly simplifying business decision-making. This applies very well to sectors such as construction, infrastructure, and long-term investments where there is nonconventional cash flow.

Considers Cost of Capital

MIRR is a far more realistic return expectation by factoring in the firm’s financing cost and the reinvestment rate of cash flows. Since firms generally reinvest their cash flows at a rate equal to or near their weighted average cost of capital (WACC), MIRR produces a much more realistic profitability estimation. Because of this adjustment, there is no danger of inflating the actual returns, and investment decisions are genuinely anchored on the present financial conditions of the business. By factoring in financing and reinvestment costs, MIRR smoothly outlines the whole picture regarding a project’s viability.

Affords Much Better Investment Ranking

While assessing investment opportunities in a business, a foolproof method of ranking investments must be in place. Projects with high IRRs are sometimes considered superior when making lesser total profits. In contrast, MIRR avoids this situation by applying a more realistic reinvestment assumption, ensuring that all decisions favour the most profitable alternative. This would provide considerable assistance to large organizations and investors dealing with diversified portfolios and ensure their decision is based upon actual value creation and not shadowy rates of return.

Decision-Making Improves in Financial Management

Due to its exactness in measuring profitability, MIRR has always been accepted in corporate finance and financial management. Financial managers adopt MIRR in vocational projects because of its ability to estimate the actual returns of the project better. By discounting the financing cost and the reinvestment rates, MIRR thus aids firms in the best structuring of their investments. MIRR, therefore, becomes an essential instrument in strategic planning, capital budgeting, and investment anticipation for the above properties. Utilization of the MIRR guarantees the flow of financial resources toward those projects that provide maximum shareholder value.

More Reliable Metric for Capital Budgeting

Capital budgeting is selecting projects that promise the highest return in the long run. IRR can often be fallacious, inducing decisions, especially when comparing projects of different sizes or lengths. MIRR is more reliable when capital budgeting is at stake since it provides a clear picture of the return from whichever angle you view it, factoring in all financial aspects of the investment. This guarantees that a company will not incur huge mistakes by ensuring its long-term investments align with its economic goals.

Modified Internal Rate of Return FAQs

1. Why The Preference Of Using MIRR Over IRR?

This is due to MIRR’s resolving of the multiple IRR problem, the realistic assumption of cash reinvestment, and the accurate measure of profitability rendered.

2. How Is MIRR Applied in Capital-Budgeting?

MIRR is a return rate that permits a company to rank investment projects, thereby helping to compare different opportunities.

3. What Are The Distinctions Between MIRR And XIRR?

While XIRR is the modified IRR that can accommodate irregular intervals of cash flows, MIRR changes based on the reinvestment assumption.

4. What Is The Role Of MIRR In Financial Management?

MIRR plays a vital role in financial management because it assists a business in making well-informed investment proposals based on the financing cost and the reinvestment rates.

5. What Is Better: MIRR Or NPV?

While MIRR is better suited for comparing project returns, NPV helps know the absolute value an investment contributes. Both metrics have their importance in financial analysis.