Net present value (NPV) is the difference between the present value of outflows and inflows of cash, establishing whether an investment is profitable. Net present value advantages and disadvantages assist companies in comprehending the advantages and disadvantages of employing this method of investment appraisal. Net present value (NPV) is a financial measure employed to assess the profitability of an investment based on the present value of future cash flows. Though NPV is most commonly used because of its accuracy, it has some disadvantages, too. Companies employ this technique to make sound financial decisions by analysing the cost and returns of an investment.

What is Net Present Value?

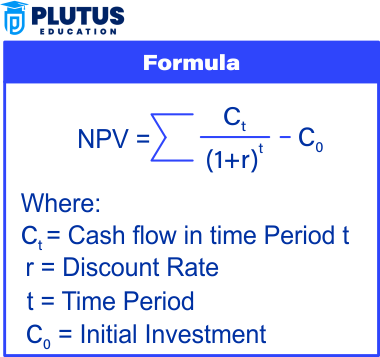

NPV is the difference between the present value of cash outflows and inflows over a period. It aids companies in determining the profitability of an investment project by considering the time value of money.

By considering the time value of money, net present value (NPV) allows for adjustment of future cash flows for inflation and risk. It considers the cost of capital by applying a discount rate that captures the opportunity cost of investment. NPV is an absolute measure a positive NPV means you will profit, and a negative NPV means you will incur a loss. It is also flexible it can be used to compare projects that have varying cash flow profiles, enabling businesses to make better decisions when investing.

Net Present Value Formula

Example of NPV Calculation

A company invests ₹1,00,000 in a project that generates ₹30,000 annually for 4 years. If the discount rate is 10%, NPV is calculated as:

If NPV is positive, the project is viable.

Net Present Value Advantages

Knowledge of net present value benefits enables companies to see the value of this financial analysis technique. Here are some Net Present value advantages:

- Considers Time Value of Money: NPV returns future cash flows to their present value. This yields a realistic profitability estimate. Businesses can analyse the effects of inflation and interest rates on cash flows. It provides appropriate pricing for long-term investment. NPV aids to take better financial decisions.

- Helps in Investment Decision-Making: A business can compare several investment alternatives. It helps to determine which projects have the best financial return. NPV makes sure we are putting money into profitable activities. It avoids losses by assessing future cash flows. NPV is a tool that companies use to assess and prioritize growth opportunities.

- Incorporates All Cash Flows: NPV considers both immediate and future cash inflows and outflows. It is a complete process of financial assessment. It helps to avoid miscalculations in investment planning. It prevents businesses from missing out on costs that might not be apparent. NPV provides full insight into financial viability.

- Improves Financial Planning: Accounting allows businesses to protect their future financial performance. NPV helps prepare a good budget and invest effectively. It helps manage cash flow better for sustainable growth. Companies can confidently plan capital expenditures. Helping achieve sustainable growth and profitability in a business.

- Accounts for Risk Factors: Organizations adjust their discount rate according to risk levels. Higher discount rates imply higher uncertainty in cash flows. It allows companies to account for market fluctuations. NPV is a valuable tool for estimating the risk in various investment options. It guarantees an equitable process in decision-making.

Net Present Value Disadvantages

Although it has advantages, NPV has some limitations. Knowing net present value disadvantages assists companies in overcoming potential pitfalls.

- Depends on Accurate Cash Flow Estimations: NPV needs accurate estimates of future cash flows. An error in estimating inflows can impact decision-making. Forecasts that may prove to be wrong can lead to bad investment decisions. The actual cash flows can be affected by unexpected changes in the market.

- Requires Selecting an Appropriate Discount Rate: If the seller rate is incorrect, it can appear to be a bad investment. When calculating the discount rate, businesses need to consider risks. At a discount rate that is too low, profitability might be overestimated. A higher rate can make a solid investment look unappealing.

- Not Ideal for Short-Term Projects: NPV tends to be better suited for long-term investments. It is not likely to effectively measure projects with fast paybacks. Evaluation Methods for short-term investments for those businesses that require immediate returns might choose payback period.

- Ignores Project Size in Comparison: NPV does not consider project scale when comparing investments. If the money amounts of the investments differ greatly, a project with a greater NPV is not necessarily superior. More commonly, large investments will lead to larger NPVs. In that case, you might find a percentage-based measure like IRR to be more helpful.

- Complex for Non-Financial Experts: NPV needs finance knowledge; for small businesses, this may be a direct conflict of interest in correctly implementing the formula. NPV is calculated using technical concepts like discounting. Errors can happen in calculation as they are not experts.

Relevance to ACCA Syllabus

NPV is a core capital budgeting technique adopted for investment appraisal under the ACCA Financial Management (FM) and Advanced Financial Management (AFM) syllabuses. NPV allows students to show how a choice maximizes or minimizes shareholder value and learn about its advantages and disadvantages, i.e. the reliance on discount rate assumptions. NPV is commonly used in financial decision-making, especially when considering long-term projects.

Net Present Value Advantages and Disadvantages ACCA Questions

Q1: What is the main advantage of using NPV for investment appraisal?

A) It provides the expected percentage return on investment

B) It considers the time value of money and shareholder value

C) It is simpler to use compared to other methods

D) It does not require discount rate assumptions

Ans: B) It considers the time value of money and shareholder value

Q2: A major disadvantage of NPV as a decision-making tool is that:

A) It ignores cash flows beyond the payback period

B) It requires an accurate estimate of the discount rate

C) It does not account for risk in project evaluation

D) It provides percentage-based results rather than absolute values

Ans: B) It requires an accurate estimate of the discount rate

Q3: Which project should be selected if two projects have positive NPVs but different investment amounts?

A) The one with the higher IRR

B) The one with the longer payback period

C) The one with the higher NPV

D) The one with the lower NPV

Ans: C) The one with the higher NPV

Q4: If the discount rate increases, what happens to the NPV of a project?

A) NPV increases

B) NPV remains unchanged

C) NPV decreases

D) NPV turns positive

Ans: C) NPV decreases

Relevance to US CMA Syllabus

The US CMA exam (Part 2 Financial Decision Making) includes capital budgeting techniques such as NPV. Candidates should also be able to evaluate an investment decision comparing NPV with the other methods of analysis such as Internal Rate of Return (IRR) and Payback Period. Knowledge of NPV and its limitations allows the management accountant to make a more informed financial decision.

Net Present Value Advantages and Disadvantages US CMA Questions

Q1: What is an advantage of using NPV instead of IRR for capital budgeting decisions?

A) NPV provides a clear dollar value for project profitability

B) NPV assumes reinvestment at the IRR rate

C) NPV ignores the cost of capital

D) NPV does not require estimating future cash flows

Ans: A) NPV provides a clear dollar value for project profitability

Q2: One limitation of using NPV is that it:

A) Does not consider the time value of money

B) Assumes cash flows are reinvested at the cost of capital

C) Ignores the initial investment cost

D) Overestimates short-term cash flows

Ans: B) Assumes cash flows are reinvested at the cost of capital

Q3: Which of the following factors affects the NPV of a project the most?

A) The number of decision-makers involved

B) The method used to calculate the payback period

C) The choice of discount rate

D) The size of the company evaluating the project

Ans: C) The choice of discount rate

Q4: What is a potential drawback if a company selects projects based solely on NPV?

A) The method favours short-term investments over long-term ones

B) It may overlook projects with higher percentage returns

C) It does not factor in capital constraints

D) The calculation is always inaccurate

Ans: B) It may overlook projects with higher percentage returns

Relevance to US CPA Syllabus

NPV is covered in financial management and capital budgeting within the US CPA exam (BEC and FAR). Joseph and Mary, meanwhile, will be expected to analyse the feasibility of projects using NPV calculations and understand how assumptions about discount rates and future cash flows influence decision-making.

Net Present Value Advantages and Disadvantages US CPA Questions

Q1: When comparing NPV and IRR, NPV is preferred because:

A) It considers all cash flows and the cost of capital

B) It ignores discount rate fluctuations

C) It provides a fixed percentage return

D) It does not consider external economic conditions

Ans: A) It considers all cash flows and the cost of capital

Q2: What is the disadvantage of NPV compared to the Payback Period method?

A) NPV does not consider profitability

B) NPV is more complicated to calculate and understand

C) NPV focuses only on the short-term cash flows

D) NPV is not used for capital budgeting decisions

Ans: B) NPV is harder to calculate and understand

Q3: A company with a higher discount rate will likely experience:

A) Lower NPV for projects

B) Higher NPV for projects

C) No change in NPV calculations

D) Positive NPV regardless of project costs

Ans: A) Lower NPV for projects

Q4: The assumption that cash flows are reinvested at the discount rate is a feature of which method?

A) Payback Period

B) Accounting Rate of Return (ARR)

C) Net Present Value (NPV)

D) Internal Rate of Return (IRR)

Ans: C) Net Present Value (NPV)

Relevance to CFA Syllabus

NPV is heavily featured under Corporate Finance and Investment Analysis in the CFA curriculum. CFA candidates are expected to know how NPV differs from IRR, how it’s used to make investment decisions, and how it’s used in practice to value long-term investments and acquisitions.

Net Present Value Advantages and Disadvantages CFA Questions

Q1: Why is NPV considered a superior method for evaluating investment projects?

A) It accounts for risk and cost of capital

B) It ignores the impact of cash flows beyond payback period

C) It is simpler to use than IRR

D) It provides a percentage return rather than a dollar value

Ans: A) It accounts for risk and cost of capital

Q2: What should be the primary decision rule when comparing two mutually exclusive projects?

A) Choose the project with the higher IRR

B) Choose the project with the higher NPV

C) Choose the project with the shorter payback period

D) Choose the project with the lower initial cost

Ans: B) Choose the project with the higher NPV

Q3: What is a key limitation of using NPV for investment decisions?

A) It does not account for inflation

B) It assumes a constant discount rate, which may not be realistic

C) It ignores the time value of money

D) It cannot be used for long-term projects

Ans: B) It assumes a constant discount rate, which may not be realistic

Q4: In which scenario would NPV and IRR provide conflicting results?

A) When the projects have different sizes and cash flow timing

B) When all cash flows are positive

C) When the discount rate is equal to the IRR

D) When evaluating a single project with no alternatives

Ans: A) When the projects have different sizes and cash flow timing