Net present value vs internal rate of return are two standard financial measures that assist companies in assessing investment opportunities. Net present value (NPV) identifies whether a project is profitable by using cash inflows minus net cash outflows to the present value. Internal rate of return (IRR) refers to the discount rate where the net present value of cash flows equals zero. Both approaches assist decision-makers in selecting the most suitable investment options but are distinct in methodology and interpretation.

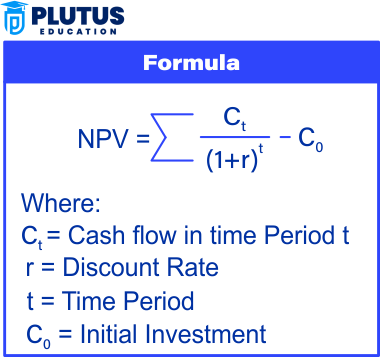

What is Net Present Value?

Net present value (NPV) is the financial analysis to evaluate the profitability of the investment project. It determines the present value of cash flows in and out and subtracts one from the other.

Net present value (NPV) finds the present value of cash inflows instead of outflows. It allows companies to define if an investment will be profitable in the long run. A Project with a positive NPV has a profitable outcome, whereas a negative NPV indicates a loss.

What is Internal Rate of Return?

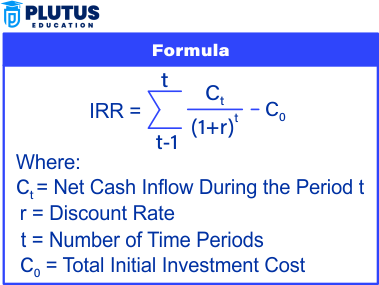

Internal rate of return (IRR) is the discount rate where the net present value (NPV) of inflows and cash outflows would be zero. IRR is the expected rate of return per year from an investment project.

We measure IRR because the discount rate makes NPV equal to zero. It is an annualised return expected from an investment. A greater IRR is a more appealing project. This IRR is compared with the cost of capital to decide if investment is feasible.

Net Present Value vs Internal Rate of Return

Net present value (NPV) and Internal Rate of Return (IRR) are fundamental investment appraisal methods in financial decision-making. Both techniques enable companies to assess project profitability, but their approach, complexity, and applicability vary. The following differences between NPV and IRR are based on critical financial factors.

Expression

NPV, expressed in monetary terms (₹) measures the real wealth a project creates for a business. This gives firms visibility into units of wealth created by investment in absolute terms. Which yields a better financial benefit?

Internal Rate of Return (IRR) is calculated as percentage (%) i.e. representing annualised returns. It allows for the comparison of different projects in terms of their profits. If a project has an IRR greater than the cost of capital, then, all other things being equal, you would want the project with the highest IRR.

Decision Criterion

For NPV, the rule of decision is straightforward, accept the project if NPV > 0 and reject it if NPV < 0. A positive NPV indicates that the project is likely to have more cash inflows than outflows and hence is financially feasible.

For IRR, the decision criterion is: accept if IRR > cost of capital and reject if IRR < cost of capital. If IRR > required return, the project is profitable. If IRR < required return, the investment will not be worthwhile.

Complexity

NPV involves an estimate of a discount rate, which may prove difficult. The validity of NPV is subject to the appropriate discount rate, which should capture the risk and cost of capital. Companies have to consider various scenarios to ensure that projections are realistic.

IRR requires an iterative solution of an equation, which may be difficult. Because IRR is calculated by trial and error or through financial software, it needs more significant calculation effort than NPV. Companies use spreadsheets or economic models to calculate IRR effectively.

Suitability

NPV can be used to compare projects of unequal size and length. It factors in the true financial effect, making it perfect for a business to decide between multiple investments. NPV enables long-term financial planning and decision-making.

The IRR method is one of the best ways to rank projects by percentage return. This is helpful when companies have limited capital and must rank their projects based on returns. While IRR can help identify a good project, it does not help compare projects with those with different investment sizes.

Multiple Rates Issue

NPV gives one actual value when judging an investment. It is impossible to have different NPVs so that they can be easily understood and used for decision-making. Companies can confidently compare projects by their NPVs.

IRR may provide more than one rate when cash flows alter signs more than once. This may lead to confusion in decision-making. When unconventional cash flows are involved, companies must be careful and employ other evaluation methods besides IRR.

| Feature | Net Present Value (NPV) | Internal Rate of Return (IRR) |

| Definition | Calculates the difference between present cash inflows and outflows. | Determines the discount rate at which NPV becomes zero. |

| Expression | Expressed as a monetary value (₹). | Expressed as a percentage (%). |

| Decision Criterion | Accept if NPV > 0, reject if NPV < 0. | Accept if IRR > cost of capital, reject if IRR < cost of capital. |

| Complexity | Requires estimating the discount rate. | Requires solving an equation iteratively. |

| Suitability | Best for comparing projects of different sizes and durations. | Best for ranking projects based on return percentage. |

| Multiple Rates Issue | No possibility of multiple NPVs. | Can yield multiple IRRs if cash flows change signs more than once. |

Relevance to ACCA Syllabus

Net Present Value (NPV) and Internal Rate of Return (IRR) are key topics in the FM and AFM syllabus. ACCA students must study capital budgeting techniques, project appraisal, and decision-making in the face of risk and uncertainty.

Net Present Value vs Internal Rate of Return ACCA Questions

Q1: What is the primary reason NPV is considered superior to IRR in capital budgeting decisions?

A) NPV considers the time value of money, while IRR does not

B) NPV provides a dollar value impact, whereas IRR gives only a percentage return

C) NPV ignores risk, while IRR accounts for risk

D) NPV is easier to calculate than IRR

Ans: B) NPV provides a dollar value impact, whereas IRR gives only a percentage return

Q2: If the IRR of a project is higher than the required rate of return, what should the company do?

A) Reject the project

B) Accept the project

C) Reduce the discount rate

D) Increase the project costs

Ans: B) Accept the project

Q3: Which of the following is a disadvantage of using IRR?

A) It does not consider the time value of money

B) It may give multiple values for projects with unconventional cash flows

C) It ignores cash flows beyond the payback period

D) It is less reliable than the accounting rate of return (ARR)

Ans: B) It may give multiple values for projects with unconventional cash flows

Q4: Which method assumes cash flows are reinvested at the company’s cost of capital?

A) Net Present Value (NPV)

B) Internal Rate of Return (IRR)

C) Payback Period

D) Accounting Rate of Return (ARR)

Ans: A) Net Present Value (NPV)

Relevance to US CMA Syllabus

Capital budgeting is a big topic in Part 2 (financial decision-making) in the US CMA exam. Candidates need discounted cash flow (DCF) techniques to make investment decisions and to derive NPV and IRR for investments. Knowing the pros and cons of these approaches is a critical component of strategically managing a business’s capital projects and investments.

Net Present Value vs Internal Rate of Return US CMA Questions

Q1: What is the main drawback of using IRR instead of NPV for evaluating mutually exclusive projects?

A) IRR ignores project size and scale

B) IRR is easier to calculate than NPV

C) IRR accounts for all project cash flows

D) IRR always leads to the same decision as NPV

Ans: A) IRR ignores project size and scale

Q2: If a company uses a discount rate higher than the project’s IRR, what will be the NPV?

A) Positive

B) Zero

C) Negative

D) Cannot be determined

Ans: C) Negative

Q3: Which of the following is a situation where NPV and IRR may lead to different project decisions?

A) When projects have conventional cash flows

B) When projects have different initial investments

C) When projects have equal payback periods

D) When projects have the same cost of capital

Ans: B) When projects have different initial investments

Q4: A project with multiple IRRs occurs when:

A) The project has conventional cash flows

B) There are multiple changes in cash flow direction

C) The NPV is positive at all discount rates

D) The payback period is longer than the project’s life

Ans: B) There are multiple changes in cash flow direction

Relevance to US CPA Syllabus

NPV and IRR are discussed in the BEC and FAR sections of the US CPA exam. This examination tests candidates with concepts relating to financial management also surrounding capital budgeting, cost of capital, and cash flows. In practical use, these calculations help decide whether or not to accept a project: NPV and IRR.

Net Present Value vs Internal Rate of Return US CPA Questions

Q1: If the discount rate increases, what happens to the NPV of a project?

A) NPV increases

B) NPV decreases

C) NPV remains unchanged

D) NPV becomes equal to IRR

Ans: B) NPV decreases

Q2: Which of the following correctly describes the IRR of a project?

A) It is the rate at which NPV becomes zero

B) It is the minimum required rate of return set by management

C) It is the project’s break-even sales growth rate

D) It measures how quickly cash flows are recovered

Ans: A) It is the rate at which NPV becomes zero

Q3: A company evaluating two mutually exclusive projects should primarily rely on:

A) The project with the higher IRR

B) The project with the shorter payback period

C) The project with the higher NPV

D) The project with the lower initial investment

Ans: C) The project with the higher NPV

Q4: If a project’s IRR is exactly equal to the required rate of return, what will be its NPV?

A) Positive

B) Negative

C) Zero

D) Cannot be determined

Ans: C) Zero

Relevance to CFA Syllabus

NPV and IRR are emphasised under Corporate Finance and Financial Statement Analysis in the CFA syllabus. These principles are fundamental in valuation investments, risk analysis, and project loans. CFA candidates need to be familiar with how to use these approaches to assess the attractiveness of investment opportunities and compare competing projects, among others.

Net Present Value vs Internal Rate of Return CFA Questions

Q1: Which capital budgeting method is most aligned with shareholder wealth maximisation?

A) Net Present Value (NPV)

B) Internal Rate of Return (IRR)

C) Payback Period

D) Profitability Index

Ans: A) Net Present Value (NPV)

Q2: A project with a higher IRR but a lower NPV than another project should be:

A) Selected because it provides a higher return

B) Rejected because NPV is the preferred method

C) Selected if IRR is above the cost of capital

D) Considered only if the payback period is shorter

Ans: B) Rejected because NPV is the preferred method

Q3: In capital budgeting, the reinvestment rate assumption of IRR is considered a disadvantage because:

A) It assumes cash flows are reinvested at the IRR, which may not be realistic

B) It assumes cash flows are reinvested at the company’s required rate of return

C) It ignores the effects of inflation

D) It does not consider capital structure

Ans: A) It assumes cash flows are reinvested at the IRR, which may not be realistic

Q4: If a project’s IRR is greater than the company’s weighted average cost of capital (WACC), what can be inferred?

A) The project will have a negative NPV

B) The project should be rejected

C) The project is expected to create value

D) The project’s cash flows are unreliable

Ans: C) The project is expected to create value