Auditing is the process that guarantees transparency, credibility, and reliability in the financial records of an organisation. It evaluates the financial operations of an organisation under a structured framework by which external stakeholders can demand accountability and accuracy. Audits include studying many issues, including economic systems’ ethics and how money works. Therefore, it is essential for commerce students and other professionals in the financial realm.

What is Auditing?

The term “Auditing” means the independent examination of reports resulting from an evaluation of evidence to form an opinion on the accuracy and correctness of financial statements in terms of the accounting standards and laws that govern it. Audits are conducted by trained persons-auditors—who do so by the examination of financial records, such as trial balances, profit and loss accounts, balance sheets, and ledgers, with the principal objective of expressing an opinion on whether or not such statements present an accurate and fair view of the financial status of the organization.

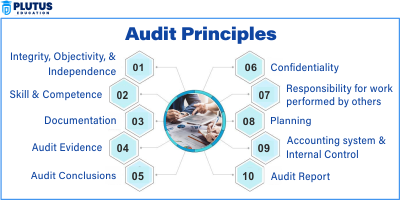

Principles of Auditing

The principles of auditing include the ethical and procedural foundations governing how audits must be conducted in the field. Auditors must follow universally accepted standards to maintain quality, fairness, and integrity in the audit process. Knowledge of these principles is essential in maintaining transparency in financial reporting. They also ensure that all approaches to audits, regardless of the type of organisation being audited, are done with a very high degree of professionalism, objectivity, and care.

Integrity

Integrity in auditing means carrying out work with honesty and moral uprightness. An auditor must not attempt to falsify outcomes or provide biased information. They should be expected to report their findings truthfully, no matter the cost to the client or audit firm. This principle is essential for maintaining trust in the profession. Bribes, pressure, or relationships cannot easily sway an auditor of integrity. They aim to deliver a fair opinion based on evidence and professional judgment.

Objectivity

The auditors must maintain their impartiality and have no conflicts of interest concerning the audit. Auditors will also continue to uphold this objectivity by not allowing any personal feeling or association to interfere with their professional judgment. Hence, objectivity enables audit conclusions to be determined based on factual evidence and is unaffected by external bias. Hence, this principle applies to planning and carrying out audits. For example, the auditor must not ignore client record discrepancies because of a long-standing relationship with management. Keeping objectivity helps maintain the credibility and acceptability of audit reports.

Confidentiality

Confidentiality entails an auditor not disclosing information acquired through the audit procedure to outsiders, not even long after the completion of the audit. This protects the organization because confidential information cannot be disclosed, nor can the auditor’s reputation be compromised. It also reassures companies that having an auditor would not expose them to data breaches or competitive disadvantages.

Professional Competence and Due Care

Auditors are expected to develop professional skills permanently and in keeping with the relevant technical knowledge. Professional competence enables auditors to handle even the most complicated audits and apply the latest standards. Due care involves executing duties diligently and attentively. Professional credibility can be lost because of incorrect audit opinions derived from the lack of this principle. Continuous learning is necessary, as laws, technology, and accounting standards keep changing.

Independent Examination

Independence is fundamental to every audit; no auditor should have ties to the audited company, not any personal, financial, or even other ties. Depending on this objectivity, which ensures an audit result is unbiased and can be relied upon by external parties such as shareholders, tax authorities, and regulators. Independence is more than avoiding conflicts; it carries a state of mind, professional skepticism. Auditors should learn to challenge and prove nearly every piece of financial information submitted to them, however credible it seems. Such vigilance enhances honesty and reliability.

Verification of Financial Data

Auditors bear the prime duty of verifying financial statements through any authentication that can be said to be an audit. Each transaction to be recorded in his books would have some form of a paper trail attached: invoices, bank statements, and contracts. Verification, for example, would ensure that what is said in the financial statements happened. Through verification, auditors would thus be able to detect either errors, discrepancies, or fraud, intentional or otherwise. Auditors may, for example, compare the financial reports with external evidence such as industry standards and/or historical data to check the reliability of the results. This last aspect would be essential to confirm the auditor’s opinion and recommendations.

Compliance Check

The compliance check shall verify that taxes are duly paid, employee benefits are appropriately managed, and financial disclosures meet legal requirements. This feature is the other significant role of the auditing activity, which determines whether the organization complies with laws, regulations, and legal accounting standards stipulated by the statutes. Penalty operations are damn sore and damage reputation. All statutory instruments and standards, such as GAAP or IFRS, keep updating. Conducive audits keep companies acting within the laws while minimising the country’s legal risk and showing accountability to stakeholders, especially in the highly regulated environment, as in the cases of banking and health care.

Importance of Auditing

Auditing plays a key role in maintaining credible and transparent financial systems. It helps bring ethics and principles among corporations to the core, as well as openness and adherence to related regulations. Auditing, being a provider of quality in verifiable financial statements to all those involved, ensures that their stakeholders will make the right financial decisions concerning the corporation.

Builds Stakeholder Confidence

An audit report assures stakeholders that the company’s financial health is adequately represented. Such reports are used by investors, creditors, and government agency officials to make crucial decisions, such as which investments to go for, on the terms of a loan or upon which law or regulation shall be implemented. Trusting in a company’s business and financial statement would inspire more investment capital, encouraging better financing terms and increasing the community’s perception of the firm. This trust is an asset; its absence at a critical juncture could affect the company’s sustainability in the long run and its position in the market.

Avails Transparency

Furthermore, an audit brings additional transparency by allowing all recorded financial transactions to be honest and trustworthy, thereby decreasing chances for manipulation and fraud and creating a culture where transparency, honesty, and accountability are fervently embraced by management. With so much transparency in financial reporting, financial transparency interferes with the internal governance role in the organisation. It enhances interdepartmental communication, fosters the provision of better decisions, and promotes integrity.

Factors that Detect Fraud and Errors

The training initiatives for auditing professionals have been geared toward recognising the flaws, irregularities, and signs of fraud in financial documents. Such detailed examination enables auditors to detect errors in the records that misrepresent what the financial statements should show. Unintentional mistakes- simply misclassifying expenses or making an outright faulty calculation gain considerable weight if not corrected in the fullness of time. Audits ensure that such inaccuracies do not get lost for companies to correct at later stages.

Encourages Compliance

One of the most notable benefits of auditing is compliance with laws and tax regulations, which are also followed by the internationally accepted accounting standards. This way, organisations may be relieved entirely from the possible consequences of statutes such as punishment and termination of business. Regular audits will usually inform the authorities of the extent to which a company can be considered compliant with rules regarding accounting. Such proactive engagement by an organisation garners goodwill among regulators, creating in them a sense of trust that lasts for quite a while concerning the corporate governance architecture of the company.

Auditing Standards & Regulations

Auditors will perform their work according to universally accepted auditing standards. These standards indicate the mode of planning, execution, and reporting of an audit. This provides a facility for uniformity and transparency in every audit and gives rightful justice to professionalism in auditing. Adherence to auditing standards would enhance the reliability of audit outcomes and ensure acceptance within legal and financial circles. These powers form part of the standards set by the ICAI in India or the IAASB worldwide.

International Standards on Auditing (ISA)

The ISA, issued by the International Auditing and Assurance Standards Board (IAASB), is a globally accepted standard that guides auditors on best practices. They cover every audit aspect—risk assessment, evidence collection, and audit reporting. These standards promote a uniform approach to auditing worldwide. ISA compliance is essential for multinational corporations, facilitating consistency across different jurisdictions.

Indian Auditing Standards (SA)

In India, audits are carried out by the Standards on Auditing (SA) issued by the Institute of Chartered Accountants of India (ICAI). These standards are consistent with international norms but tailored according to India’s law, custom, and business practices. Observing SAS ensures that Indian auditors create locally compliant and globally respected work. These standards enhance audit quality and comparability in the Indian market.

GAAP and Other Frameworks

Generally Accepted Accounting Principles (GAAP) form the basis of financial statement preparation. Auditors must ensure that their clients prepare statements in compliance with GAAP or other relevant frameworks like IFRS. An audit that confirms compliance with GAAP boosts the authenticity of the financial statements. It also ensures that users of these reports—investors, banks, or regulators—make decisions based on standardised and reliable data.

Principles of Auditing FAQS

1. What are the basic principles of auditing?

Integrity, objectivity, confidentiality, competence, and an evidence-based approach guide auditors in performing ethical and accurate audits.

2. Why are auditing principles important?

They ensure audits are fair, transparent, and trustworthy, helping build stakeholder confidence and meet legal requirements.

3. What is the difference between internal and external auditing?

In-house teams do internal audits for control checks, while independent firms conduct external audits for statutory validation.

4. What are the limitations of auditing?

Audits may miss hidden fraud, rely on provided data, and are limited by time, scope, and sampling techniques.

5. What is materiality in auditing?

Materiality is the threshold above which errors or omissions can impact financial decisions and audit opinions.