Production and cost are two fundamental concepts in economics that help explain the relationship between input factors and the output produced in an economy. The production process is the conversion of inputs such as labor, capital, and raw materials into goods and services. Cost is the expenditures incurred in the production process. The study of the forces that guide production and cost is a critical aspect of business decision-making, policy-making, and just about anybody interested in the economic behavior of an economy.

What is Production and Cost?

Production and cost are tightly linked concepts in economics. Production refers to the process of using resources to create goods and services, whereas cost refers to the expenses that occur during this process.

These costs include both explicit costs (like wages and materials) and implicit costs (such as the opportunity cost of resources). The goal of any business or firm is to optimize production to generate maximum output while minimizing cost, which ultimately leads to maximizing profit.

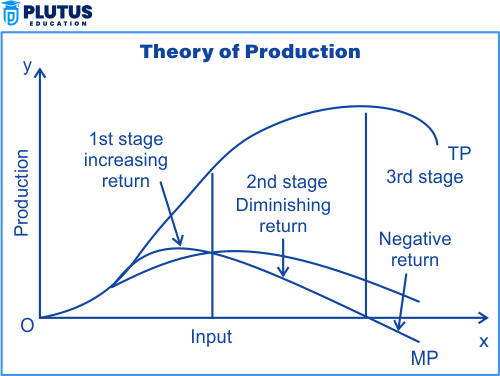

Production Function

The production function is a mathematical relationship that describes how input factors (like labor, capital, and land) are transformed into output. In simple terms, it shows the quantity of goods and services produced based on the amount of resources used. The production function can help firms understand how to efficiently allocate resources to maximize output.

- Example of Production Function: If a factory uses 5 machines and 10 workers to produce 100 units of goods, the production function shows the output produced for each combination of resources.

Cost Function

A cost function refers to the relationship between the cost of production and the level of output. It helps businesses calculate how much it will cost to produce different levels of output. It is critical for making decisions about production scale and pricing.

- Example of Cost Function: A company might determine that it costs ₹200 to produce 100 units and ₹300 to produce 150 units. The cost function helps the company understand the variable and fixed costs involved at different production levels.

Types of Production

Understanding the different types of production is crucial for grasping how businesses scale and produce goods or services. These types vary based on factors like the scale of operation, the nature of goods being produced, and the resources involved.

Short-Run Production

In the short run, some factors of production are fixed, while others are variable. Firms can only adjust the variable inputs (like labor and raw materials) to change the level of output, but cannot easily alter fixed factors (such as machinery or factory size).

- Example: A bakery might hire more workers during the holiday season (variable input) but cannot expand its bakery space (fixed input) in the short run.

Long-Run Production

In the long run, all factors of production can be adjusted. Firms can change the size of their production facility, adopt new technologies, and hire or lay off workers to optimize production.

- Example: A company planning to expand its business might invest in additional factory space, new machinery, or advanced technology to increase its production capacity.

Mass Production

Mass production involves the production of large quantities of standardized goods using assembly line techniques. It is typically used for products that require high levels of output at low costs, such as consumer electronics or automobiles.

- Example: Car manufacturers like Ford use mass production to build thousands of cars each month using automated systems and highly specialized workers.

Custom Production

In contrast to mass production, custom production focuses on creating tailored goods based on specific customer requirements. It involves producing unique products in smaller quantities but typically at a higher cost.

- Example: Custom furniture manufacturers or luxury car brands like Rolls Royce offer bespoke products designed specifically for individual customers.

Types of Cost

Understanding the different types of costs involved in production is essential for businesses to manage their finances and optimize profit margins.

- Fixed Costs: Fixed costs are costs that do not change with the level of output. These costs remain constant regardless of the quantity of goods produced. Examples of Fixed Costs: Rent for the production facility. Salaries of permanent employees. Insurance premiums. Depreciation on machinery.

- Variable Costs: Variable costs change in direct proportion to the level of output. These costs increase as production increases and decrease as production decreases. Examples of Variable Costs: Raw materials. Wages for hourly workers. Energy consumption (e.g., electricity used in manufacturing).

- Total Costs: Total costs refer to the sum of fixed costs and variable costs. This represents the total amount a business spends on producing a certain quantity of goods or services.

- Marginal Cost: Marginal cost refers to the additional cost incurred by producing one more unit of output. It is essential for firms to understand marginal costs because it helps them determine the optimal production level. Example of Marginal Cost: If it costs ₹200 to produce 100 units and ₹220 to produce 101 units, the marginal cost of the 101st unit is ₹20.

- Average Cost: Average cost refers to the cost per unit of output, calculated by dividing total costs by the number of units produced.

Functions of Production and Cost

The functions of production and cost are essential for firms to make informed decisions about how to optimize their operations. Here are a few functions of Production and cost:

Maximizing Output with Limited Resources

The production function helps businesses determine the maximum output that can be achieved with a given set of resources. By understanding the production function, firms can optimize the use of labor, capital, and raw materials to achieve the best possible output.

- Example: A firm may use a production function to calculate how many workers and machines it needs to produce the highest number of goods at the lowest cost.

Cost Minimization

The cost function helps businesses identify the most cost-effective way to produce goods. By analyzing variable and fixed costs, firms can find the optimal combination of resources to minimize costs and maximize profitability.

- Example: A company might analyze its cost function to determine whether it should invest in more labor or better machinery to reduce production costs.

Determining Pricing Strategy

Understanding the relationship between production and cost is essential for setting prices. A firm must ensure that the price it charges covers the cost of production and generates a profit margin.

- Example: If a company’s total cost of production per unit is ₹50 and it wants to make a profit of ₹10 per unit. It should set the price at ₹60.

Decisions About Scale of Production

Production and cost functions are essential for businesses when deciding whether to expand or reduce the scale of production. By understanding how costs change with different levels of output, firms can decide the optimal scale of operations.

- Example: A company might use cost and production functions to decide whether to expand its factory size to increase production and lower costs per unit.

Production and Cost Economics FAQs

What is production and cost?

Production and cost are complementary concepts in economics. Production refers to the creation of goods and services. cost describes the expenses that have been made in the process.

Provide examples of production and cost.

Examples of production may include manufacturing goods in a factory. Costs would include such things as, raw materials, and fixed costs.

What is the production function?

The production function is a mathematical relationship describing how inputs such as labor and capital are transformed into output, which refers to goods or services.

What are fixed and variable costs?

Fixed costs remain the same regardless of changes in output levels such as rent or salaries. Variable costs change with output volumes such as raw materials or hourly wages.

How do production and cost functions help businesses?

It helps organizations optimize their functions by determining how best to use different resources. With minimum cost, thereby maximizing production and profitability.