An auditor is an expert who reviews and checks financial records for accuracy, regulatory compliance, and financial reporting integrity. The rights and duties are the right to access books of accounts, right to obtain information and explanations, the duty to examine financial statements, the duty to maintain confidentiality, and many more. An auditor ensures that financial statements are accurate, reasonable, and by the law. They have certain rights, including access to the company records and explanations from management. Their responsibilities include checking financial transactions, fraud detection, and reporting. In this article, we will discuss who is an auditor, the rights of an auditor, and the responsibilities of an auditor.

Who is an Auditor?

An auditor is a professional with qualifications who ensures that a company’s accounts are transparent, accurate, and regulatory compliant. Auditors assist in identifying fraud, evaluating risks, and ensuring financial integrity within an organization.

An auditor is an authoritative figure accountable for auditing an organization’s entries & statements. They determine whether financial statements are free of material misstatements and comply with regulatory requirements. So please remember auditors are the ones primarily responsible for keeping investors confident and avoiding the chance of financial fraud.

There are internal and external auditors. Internal audit pertains to persons working inside a company, measuring risks and optimizing procedures, whereas external audit works for independent evaluations for a third party, stakeholders. They review transactions and seek compliance with tax and accounting laws and potential errors or fraud. Good audit enhances corporate governance financial audit responsibility.

Rights of Auditor

The right of auditor is significant in bringing financial transparency and accountability. To do their jobs well, they have several rights to review records, interview people, and flag fraud. The following shows the important auditor rights explained in easy words.

Right to Access Books of Accounts

Auditors should have access to complete financial and transaction records, invoices, bank statements, accounting documents, etc. This enables them to check if the company is providing correct details about finances. For instance, say a company has declared that it has generated ₹10 crore of sales; the auditor can check sales invoices, bank deposits, and other documents to verify the same claim. This makes it possible for the auditor to ask management if no records are available.

Right to Obtain Information and Explanations

Auditors may request a company’s operations, directors, and employees to explain financial transactions. They are entitled to seek supporting documents and explanations if they see anything amiss. For instance, if an auditor spots that marketing expenses are unusually high, they can request receipts, contracts, and other evidence to ensure a company is not misreporting costs. Auditors can insist on investigating if explanations are not succinct.

Right to Visit Company Branches

Auditors can also go to any office or branch of a company where the company keeps its financial records. This is to ensure that all the branches follow the same financial rules and standards of reporting. For instance, If an organization has five branches throughout India, the auditor can visit everyone to verify its cash balance, inventory documents, and financial dealings. Thus, the auditor can report any incorrect or lacking records of any branch.

Right to Receive Notices and Attend Meetings

Auditors are entitled to notice of such meetings as are mentioned for the company i.e., Board Meetings, Annual General Meetings (AGM), and Audit Committee Meetings. They can also participate in these meetings to provide financial perspective and answer questions. As an illustration, when an auditor discovers an issue in a company’s financial statements, they must go to the AGM to explain their findings to shareholders. This shows investors the actual health of the corporation.

Right to Report to Shareholders

External auditors issue an audit report to shareholders in which they provide their opinion on whether the company’s financial statements are fair. They can mention it in their report if they find errors or fraud. For instance, When an auditor discovers that a specific organization’s financial records have been manipulated, they can provide a qualified audit report or even a negative opinion alerting shareholders to potential financial misstatements.

Right to Be Paid for Services

According to the contract, auditors are entitled to payment for their services. A company cannot pay an auditor once it has been undertaken. To illustrate, If an auditor agrees to ₹5 lakh audit, the company shall pay this amount after the work is accomplished. If the company defers payment, the auditor may file a lawsuit.

Right to Report Fraud to Authorities

An audit is also mandated by law to report financial fraud. Auditors may report the matter to regulatory authorities like SEBI, RBI, or the Ministry of Corporate Affairs (MCA) if they find financial fraud. This helps prevent fraud from hurting investors or the economy. For example, if a firm conceals its liabilities to appear financially stronger, the auditor can inform SEBI or MCA. Then, these authorities can take action against it.

Right to Resign from the Audit

Auditors have the right to resign when the company doesn’t cooperate and prevents them from doing their work. The resignation should be notified in their official records as well. For example, suppose a firm refuses to provide its financial records to the auditor. In that case, the auditor may resign and notify shareholders that they cannot complete the audit due to a lack of cooperation.

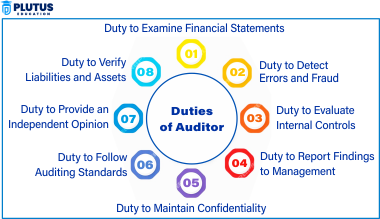

Duties of Auditor

An auditor is responsible for maintaining the accuracy and transparency of a company’s financial records. They review financial statements, identify fraud, and confirm that accounting rules are followed. Their duties also keep businesses on the right side of investors and regulatory bodies. The auditor’s roles and responsibilities are as follows:

Duty to Examine Financial Statements

Auditors must scrutinize a company’s financial statements, profit and loss accounts, balance sheet, and cash flow statements. They check if the firm accurately records revenue, expenses , and profits. In such cases, an auditor will verify sales records, customer invoices, and bank deposits and ensure that they add up to ₹50 crore when the company claims to have generated revenue of ₹50 crore.

Duty to Detect Errors and Fraud

They are expected to identify errors in accounting and investigate suspected financial fraud in the company. They scrutinize financial transactions for false statements, false entries, or fraud. For example, An auditor can find such entries if a company has made payments to fake suppliers by cross-checking their bank records and with supplier details.

Duty to Evaluate Internal Controls

Auditors have to evaluate whether the company has a sound internal control system to guard against financial mismanagement and fraud. They review the company’s approval and payment processes. On the other hand, all employees separate their duties if the same employee authorizes and processes payments to minimize the risk of fraud or error.

Duty to Report Findings to Management

Auditors must prepare a comprehensive audit report and communicate their findings to the company management. They flag risks, financial irregularities, and areas in need of improvement. For instance, if the company faces a problem of poor inventory tracking, the auditor can recommend an improved method of stock control to minimize losses and theft.

Duty to Maintain Confidentiality

Auditors should keep all company financial data and should never leak sensitive financial data. They have to ensure company records are secure and not shared with outsiders. For instance, When an auditor reviews a client’s financial statements, they cannot disclose that information to competitors or any third parties.

Duty to Follow Auditing Standards

Auditors have to adhere to the found financial principles such as GAAP (Generally Accepted Accounting Principles), IFRS (International Financial Reporting Standards), and the Companies Act, 2013. These are standards intended to ensure audits are performed accurately and fairly. For instance, Auditors need to ensure that revenue is recognized in the right result period according to commonly accepted rules.

Duty to Provide an Independent Opinion

The auditors are to give an impartial and balanced audit report. They should be independent from company management or external pressure. If they do find financial misstatements, they have to honestly report that they do exist. For example, If an auditor discovers that a company is manipulating financial statements, they should issue an adverse audit opinion rather than concealing the matter.

Duty to Verify Liabilities and Assets

Auditors must ensure that all company liabilities and assets are accurately recorded in financial statements. They confirm that bank loans, outstanding payments, and asset valuations are all in line with the company’s books. For instance, When a company claims ownership of property worth ₹10 crore, the auditor checks for the documents of ownership of the property as well as the market value of the property.

Rights and Duties Auditor FAQs

What are the duties and rights of company auditor?

The duties of company auditors are to examine statements, detect fraud, and ensure compliance, while their rights are to access financial records, attend board meetings, and report fraud.

What is the salary of auditor in India?

The salary of an auditor in India is ₹3 lakh to ₹15 lakh per annum, based on company size and experience.

What is the Comptroller and Auditor General of India’s role?

CAG audits accounts of government ensures transparency of finance in public sector enterprises, and submits findings to Parliament.

What are the company auditor rights?

The rights of the company auditor include the right to access books, get explanations, join meetings, and resign where necessary.

Can the auditor decline to sign the audit report?

Yes, an auditor can decline to sign if financial statements are deceptive or management fails to provide adequate audit evidence.