Every business needs to record its sales in proper books. This helps to keep track of income and customers. The sales journal entry is the first and most important step to record a sale in accounting. It shows that goods or services have been sold to a customer and money is due or received. So, to answer the topic, a sales journal entry is the accounting entry passed when a business sells goods or services. It records revenue and increases the customer account or cash/bank account depending on the nature of sale.In real life, businesses sell on both cash and credit. In cash sales, the business gets money immediately. In credit sales, the customer pays later. Both types need different sales journal entries. If entries are not made on time or made wrongly, it can affect the profit, tax records, and business health.

Meaning of Sales Journal Entry

The sales journal entry is the accounting record made when goods or services are sold. This entry tells us how much was sold, who bought it, and what account gets affected. It is the starting point of revenue recording.

Every sale affects two accounts:

- Sales Account – which shows revenue

- Cash/Bank or Debtor Account – which shows money received or to be received

The business earns revenue, so we credit the sales account. If the customer pays in cash, we debit the cash account. If the customer pays later, we debit the accounts receivable or debtor’s account.

Why is it important?

Recording the sale keeps track of income. It helps in tax filing, checking profits, and handling receivables. The entry also helps in preparing the balance sheet and income statement correctly. It is a part of the double-entry system, which makes sure every transaction is complete and error-free.

Sales journal entries also help during audits. Auditors check if income is properly recorded. If entries are wrong, the business may face fines or tax issues.

In summary:

- It records how much the business sold

- It shows who owes money or how much was received

- It helps prepare financial reports

- It helps track sales trends and growth

This simple entry plays a big role in understanding and managing a business’s income.

Format of Sales Journal Entry

Sales journal entries follow a fixed format. This format follows the double-entry rule of accounting. Every transaction affects two or more accounts equally. The total debits must equal the total credits.

The format depends on whether it is a cash sale or credit sale.

1. For Cash Sales

The cash account is debited because the business receives money. The sales account is credited to show income earned.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| dd/mm/yyyy | Cash A/c Dr. To Sales A/c(Being goods sold for cash) | Amount | Amount |

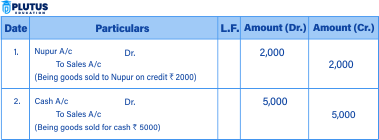

2. For Credit Sales

The customer (debtor) account is debited because the customer owes money. The sales account is credited to show the income.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| dd/mm/yyyy | Customer A/c Dr. To Sales A/c(Being goods sold on credit) | Amount | Amount |

Impact of Sales Journal Entry on Financial Statements

A sales journal entry directly affects the income and financial position of the business. It plays a key role in three main financial statements:

1. Income Statement (Profit and Loss Account): The sales account goes under the revenue section. It shows how much the business earned during a period. More sales mean more profit, but only if costs are low. Sales return reduces the net revenue.

2. Balance Sheet: In credit sales, the customer amount goes under accounts receivable in current assets. In cash sales, the amount increases cash or bank balance. It also helps in calculating working capital and liquidity.

3. Cash Flow Statement :Cash sales increase the cash from operating activities. In credit sales, cash comes later, so it is not shown until money is received.

Other impacts:

- Helps in GST calculations.

- Affects tax filings.

- Shows business performance to lenders or investors.

Wrong entries lead to wrong reports. That’s why it is very important to make correct entries and keep them up to date.

Relevance to ACCA Syllabus

Sales journal entry is a part of Financial Accounting and Financial Reporting in ACCA. It supports the understanding of revenue recognition, double-entry bookkeeping, and accurate recording of transactions. Students must apply this knowledge in paper F3 (FA) and advanced papers like FR and SBR. It helps in preparing proper ledgers, trial balance, and financial statements.

Sales Journal Entry ACCA Questions

Q1: What is the correct journal entry for a credit sale of ₹5,000 to Mr. X?

A) Sales A/c Dr. ₹5,000; To Mr. X A/c ₹5,000

B) Mr. X A/c Dr. ₹5,000; To Sales A/c ₹5,000

C) Cash A/c Dr. ₹5,000; To Sales A/c ₹5,000

D) Sales A/c Dr. ₹5,000; To Cash A/c ₹5,000

Ans: B) Mr. X A/c Dr. ₹5,000; To Sales A/c ₹5,000

Q2: In which section of the income statement is sales revenue recorded?

A) Operating Expenses

B) Cost of Goods Sold

C) Revenue

D) Equity

Ans: C) Revenue

Q3: What type of account is the sales account?

A) Asset

B) Liability

C) Income

D) Expense

Ans: C) Income

Q4: What happens to the balance sheet when a credit sale is recorded?

A) Only sales increase

B) Accounts receivable increases

C) Cash increases

D) Retained earnings increase

Ans: B) Accounts receivable increases

Relevance to US CMA Syllabus

In the US CMA Part 1 – Financial Planning, Performance, and Analytics, understanding sales journal entries is essential. It supports topics like revenue tracking, internal controls, and financial reporting. Candidates must apply the double-entry system to measure and control business performance effectively.

Sales Journal Entry US CMA Questions

Q1: When a company records a credit sale, which account gets debited?

A) Sales

B) Cash

C) Accounts Receivable

D) Bank

Ans: C) Accounts Receivable

Q2: What is the effect of a sales journal entry on profit?

A) Increases profit

B) No effect on profit

C) Decreases profit

D) Only affects liabilities

Ans: A) Increases profit

Q3: Which of these internal controls is most relevant to credit sales?

A) Payroll reconciliation

B) Sales approval process

C) Bank reconciliation

D) Petty cash policy

Ans: B) Sales approval process

Q4: Which document usually supports a sales journal entry?

A) Debit Note

B) Purchase Order

C) Invoice

D) Credit Note

Ans: C) Invoice

Relevance to CFA Syllabus

CFA Level I emphasizes understanding of financial statements and reporting mechanics. Sales journal entries are important in analyzing revenue recognition, working capital management, and account receivables. CFA candidates must know how revenue transactions affect the income statement and balance sheet.

Sales Journal Entry CFA Questions

Q1: What happens to revenue when a sales journal entry is recorded?

A) Revenue stays the same

B) Revenue decreases

C) Revenue increases

D) Only balance sheet changes

Ans: C) Revenue increases

Q2: In a credit sale, which asset increases?

A) Inventory

B) Cash

C) Property

D) Accounts Receivable

Ans: D) Accounts Receivable

Q3: Which of the following is part of the revenue recognition principle?

A) Record revenue when expense is paid

B) Record revenue when cash is received

C) Record revenue when earned and realizable

D) Record revenue when budget is made

Ans: C) Record revenue when earned and realizable

Q4: If a company records fake sales, which ratio will show misleading results?

A) Return on Equity

B) Inventory Turnover

C) Accounts Payable Turnover

D) Receivables Turnover

Ans: D) Receivables Turnover

Relevance to US CPA Syllabus

In the US CPA FAR (Financial Accounting and Reporting) section, sales journal entries support topics like revenue recognition under GAAP, internal control over receivables, and presentation in financial statements. Knowing the impact of these entries on financial health is essential for CPA candidates.

Sales Journal Entry US CPA Questions

Q1: Under accrual accounting, when should revenue be recognized?

A) When order is received

B) When cash is received

C) When service is rendered or goods delivered

D) When invoice is sent

Ans: C) When service is rendered or goods delivered

Q2: What is the correct double entry for a sale of $2,000 on credit?

A) Cash A/c Dr.; To Sales A/c

B) Sales A/c Dr.; To Accounts Receivable

C) Accounts Receivable A/c Dr.; To Sales A/c

D) Bank A/c Dr.; To Revenue A/c

Ans: C) Accounts Receivable A/c Dr.; To Sales A/c

Q3: Where are sales returns recorded?

A) General Ledger only

B) Sales Journal

C) Sales Returns Journal

D) Purchase Returns Journal

Ans: C) Sales Returns Journal

Q4: What happens if sales are overstated in financial statements?

A) Assets decrease

B) Net income is understated

C) Net income is overstated

D) Liabilities increase

Ans: C) Net income is overstated