Statistical and non statistical sampling are methods for auditing and research. They help auditors and researchers draw inferences from a sample population and not a total population. Statistical sampling is taking samples based on mathematical and probabilistic techniques to get samples free from bias. Non-statistical sampling depends on a person’s judgment and experience when selecting samples.

Analysis of a larger population without sampling is impractical. Researchers and auditors’ samples save time and money without sacrificing accuracy. Eventually, both have their strategic importance in such scenarios, depending on the audit nature, objectives, and risk factors.

What is Audit Sampling?

Audit sampling is the procedure where a subset of data is selected from a larger population, and conclusions are made based on it. This is usually essential for auditors who must check financial records, transactions, or compliance without reviewing every item. It is efficient in auditing, keeping workload, and denying a great deal but sustaining accuracy and reliability.

Application audit sampling includes financial audits, compliance checks, and internal control evaluations. Sampling types used by auditors are to identify possible areas of errors, fraud, or deviations from compliance requirements. Well-done sampling guarantees auditors reasonable assurance on the financial statements.

To give meaningful insights, the samples selected should represent the whole population. If one picks an incorrect sampling method, it can lead to misleading conclusions. This is why statistical and non-statistical sampling are considered essential parts of auditing.

Types of Auditing

Audit types are different, as each has its particular objective and scope. Requirements vary from one audit type to another, and the sampling method also depends on the nature of the type of audit.

- Financial Audit – Audit for accuracy in financial statements and compliance to standards in accounting practice.

- Internal Audit – Evaluates internal controls, risk management, and operational efficiency.

- Compliance Audit – Determines compliance with laws, regulations, and policies.

- Operational Audit – Examines operational processes to boost the effectiveness and efficiency of the organization.

- Forensic Audit – Checks accounts against fraud, financial wrongdoing, or legal violations.

Statistical and Non Statistical Sampling in Auditing

Auditing employs several different forms of sampling, but most have been categorized into statistical and non-statistical sampling. These methods determine how the auditor will select samples and analyze the results. Statistical and non-statistical sampling are the two main types of sampling, both of which have their purposes within the auditing environment. Their choice depends on the risk assessment, audit objectives, and resources available.

Statistical Sampling

The auditor applies probability theory and mathematical techniques to select the sample in statistical sampling. All items in the population are known for being selected, while the method ensures objectivity and reliability in audit conclusions. It’s also helpful in minimizing bias and accurately estimating error rates within the dataset.

Features of Statistical Sampling

- Probability-Based Selection – Each item has a known probability of selection.

- Unbiased Results – Randomization removes certain biases from the auditor.

- Mathematical Accuracy – It uses statistical formulas for sample size and for evaluation.

- Objective Approach – Makes measurable assurance of sample reliability.

- Higher Reliability – Strong basis for conclusions.

Importance of Statistical Sampling

Statistical sampling is essential in audits, as it requires high accuracy. It minimizes error and provides a scientific basis for decision-making. Regulatory bodies generally prefer statistical sampling due to its reliability in it.

Auditors often used statistical sampling to study the results from tests in large populations and high-risk areas. It is also helpful in identifying fraud, errors, and irregularities. Furthermore, it allows auditors to calculate risk due to sampling and estimate the probability of material misstatements.

Standard Techniques

- Random Sampling – Picking a random grouping of items for equal representation.

- Stratified Sampling – Dividing the population into subgroups and selecting samples from each subpopulation.

- Systematic Sampling – Selection of every nth item from an ordered list. Non Statistical Sampling

Non Statistical Sampling

Non-statistical sampling is a technique whereby the auditor selects samples based on personal judgment rather than statistical probability. No mathematical formulas work in this method; rather, it depends on the auditor’s experience and the knowledge of associated risk factors. It is beneficial for targeted audits where specific areas of concern are considered.

Features of Non Statistical Sampling

- Judgmental development of selection– Auditors select samples from their experience.

- Subjectively used– No calculating formulas for sample selection.

- Flexible sampling– Adequate for some smaller audits relating to specific concerns.

- Inexpensive– Not as heavy a consumer of resources as are statistical methods.

- Dependent on Auditor’s Skill – Accuracy depends on their judgment.

Importance of Non-Statistical Sampling

Non-statistical sampling is helpful for auditors in a particular industry or a specific company to highlight significant risk areas, as opposed to pure random sampling.

- Small Audits- When one can see the population is small and does not warrant randomization.

- Fraud Examination– High-risk transactions or accounts.

- Compliance Tests– Important areas of consideration based on audit history.

- Haphazard Sampling– Sample selection without any structure.

- Block Sampling- Review of a continuous block of transactions.

- Judgmental Sampling- Sample by known risk factors.

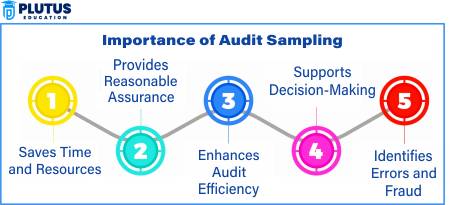

Importance of Audit Sampling

Audit sampling is an essential ingredient of productive and efficient auditing. It enables auditors to form judgments without examining each transaction.

- Saves Time and Resources- Sample reduces the number of items auditors must examine. Hence, it makes audits more cost-effective.

- Provides Reasonable Assurance- It allows the auditor to give an opinion on the financial statements’ freedom from material misstatement.

- Enhances Audit Efficiency– Helps auditors examine high-risk areas.

- Supports Decision-Making- This is for auditors and management alike in making the decisions they must make.

- Identifies Errors and Fraud- Detects financial irregularities in a very large set of data.

Purpose of Audit Sampling

It would achieve several objectives in financial and compliance auditing. It would bring the following to the auditor: misstatements in the work, control effectiveness tests, and compliance with laws and regulations.

- Finding Errors and Fraud – Sampling allows auditors to uncover misstatements and fraudulent acts.

- Assess Internal Controls – Considers the effectiveness of internal control systems within an organization.

- Compliance Verification – Checks compliance with accounting standards, laws, and regulations.

- Reduced Audit Risk – Loss of material misstatements is minimized.

- Reliable Conclusions – The auditor forms an opinion over the auditor’s financial statements.

Statistical and Non Statistical Sampling FAQs

1. What is the difference between statistical and non-statistical sampling?

Statistical sampling uses criteria of selecting samples using probability and resulting in unbiased results, whereas non-statistical sampling uses the auditor’s judgment, subjective in nature. Statistical sampling could provide measures of accuracy; non-statistical sampling will provide flexibility.

2. Why is statistical sampling the preferred sample with auditors?

It minimizes bias, reflects adequately the entire population under investigation, and allows auditors to measure sampling risk. Thus, regulators recommend this method for its reliability.

3. When can a non-statistical sampling be used?

Non-statistical sampling is best for simple audits, in targeted investigations, and when expert judgment is advised and provides areas that an auditor should focus on.

4. How does audit sampling benefit fraud detection?

It highlights transactions with errors, anomalies, and unusual activities. Hence, such sampling makes it easier to consider the high-risk areas and observe the tracked patterns by targeted analysis to detect fraud.

5. What methods are typically used for statistical sampling?

Some common methods are random sampling, stratified sampling, and systematic sampling, through which the auditors ensure fair as well as general representative results from audit exercises.