The theory of production and cost is a crucial concept in economics that explains the relationship between input factors, production processes, and the costs incurred in producing goods and services. This theory helps how a company is supposed to optimize its way of resource allocation, lower production costs, and be more profitable. One goes about it by checking interactions and how costs behave when changes are made at various output levels.

What is Theory of Production and Cost?

The theory of production and cost refers to the relationship between the inputs used in production and the resulting output, along with the costs incurred during this process. The theory emphasizes how firms use resources land, labor, capital, and entrepreneurship to produce goods and services, and it also explores how these inputs affect total costs.

If we just consider the theory of production focuses on the production function, which describes how different combinations of inputs lead to varying levels of output.

The theory of cost examines the behavior of costs as output increases. This includes both fixed and variable costs, and how they change depending on the scale of production. The theory helps businesses understand the most cost-efficient way to operate and scale their production.

Factors of Production

The factors of production are the resources or inputs that firms use to produce goods and services. These factors play a significant role in both the production process and the cost structure of a business. The four main factors of production are:

- Land: Land refers to all natural resources that are used in the production process. Examples: Fertile soil for farming, timber, water sources, and mineral deposits.

- Labor: Labor represents the human input required for production, including physical, mental, and intellectual efforts. Examples: Factory workers, engineers, office staff, laborers.

- Capital: Capital refers to the money, machinery, tools, buildings, and infrastructure needed for production. Unlike labor and land, capital is a man-made factor that requires investment. Examples: Factories, machinery, vehicles, computers, and office buildings.

- Entrepreneurship: Entrepreneurship involves the organizational and management skills required to combine the other three factors of production—land, labor, and capital—efficiently. Entrepreneurs bear the risk of the business and seek to maximize profits through innovation, market strategies, and decision-making. Examples: Business owners, innovators, startup founders.

Types of Cost

In the theory of production and cost, understanding the different types of costs is essential for businesses to analyze their financial performance and efficiency.

Fixed Costs

Fixed costs are expenses that do not change with the level of output. They remain constant regardless of how much is produced or sold. Fixed costs are incurred even if production is zero. These costs are usually associated with long-term investments and overheads.

Examples: Rent for factory space, salaries of permanent employees, insurance, and interest on loans.

Variable Costs

Variable costs fluctuate or change with the level of production. As output increases, variable costs rise, and as production decreases, these costs fall. Variable costs are typically linked to the direct production process, such as raw materials and hourly wages.

Examples: Raw materials, energy costs, wages for temporary labor, and transportation costs.

Total Costs

Total cost is the sum of fixed and variable costs. It represents the overall expenditure required to produce a given level of output.

Marginal Cost

Marginal cost refers to the additional cost incurred when producing one more unit of output. It is a crucial metric for firms because it helps determine the optimal level of production.

Average Cost

Average cost is the total cost per unit of output. It is calculated by dividing the total cost by the number of units produced.

Relationship Between Production and Cost

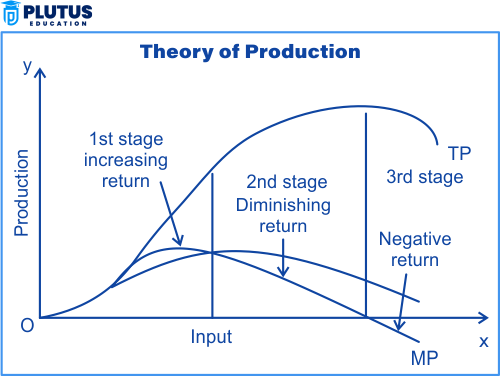

The relationship between production and cost is central to the theory of production and cost. As a firm produces more units of output, both its total costs and marginal costs behave differently. This relationship is influenced by the law of diminishing returns.

The Law of Diminishing Returns

The Law of Diminishing Returns is a key concept in production theory, stating that as more units of a variable input (e.g., labor) are added to fixed inputs (e.g., machinery or land), the additional output produced by each new unit of input will eventually decrease.

- Decreased Efficiency: As production continues, workers may become overcrowded or machinery may become overused, leading to lower productivity per unit of input.

- Cost Implications: Diminishing returns can increase marginal costs because additional inputs are less effective at increasing output. This phenomenon can lead to higher unit costs and reduced profitability at higher levels of production.

Understanding Cost Curves

The relationship between production and cost is often depicted through various cost curves:

- Total Cost Curve (TC): It Shows the total cost of producing a given level of output.

- Marginal Cost Curve (MC): Illustrates the cost of producing one additional unit of output.

- Average Cost Curve (AC): Shows the average cost per unit of output.

These curves help firms determine their optimal level of production, where marginal cost equals marginal revenue.

Conclusion

The theory of production and cost is fundamental for understanding how firms operate and make decisions regarding production and pricing. By analyzing the relationship between inputs, outputs, and costs, businesses can make informed choices to optimize production and minimize costs. The theory provides essential insights into the role of the law of diminishing returns, cost curves, and the interaction between fixed and variable costs. With this knowledge, firms can achieve greater efficiency, maximize profitability, and scale operations effectively.

Theory of Production and Cost FAQs

What is the difference between the theory of production and the theory of cost?

The theory of production focuses on how inputs are transformed into outputs, while the theory of cost examines the costs associated with production. The production theory explains the output process, and the cost theory deals with cost management.

What does the law of diminishing returns mean?

The law of diminishing returns states that as more units of a variable input are added to a fixed input, the additional output from each additional unit will eventually decrease.

How do fixed costs differ from variable costs?

Fixed Costs: Costs that do not change with the level of output, such as rent and salaries. Variable Costs: Costs that vary with the level of production, such as raw materials and labor.

What is marginal cost in the context of production?

Marginal cost is the additional cost incurred when producing one more unit of output. It helps firms understand how much extra cost is associated with increasing production.

What are the key factors of production?

The key factors of production include land, labor, capital, and entrepreneurship. These are the inputs that businesses use to produce goods and services.