Capital structure includes the trade off theory of finances and debts used by firms to determine the optimal mix of debt and equity financing by balancing benefits and financing costs. According to this theory, companies incur debts to benefit from the tax shield provided by the state, but too much of it creates financial distress and bankruptcy costs. The firm must achieve a balanced state in these aspects to successfully develop an optimal capital structure that minimises the cost of capital and maximises value. The trade-off theory differs from the pecking order theory, in which firms prefer internal funds against externalisation.

What is Capital Structure?

On the other hand, capital structure indicates financial capability, which is the part of debt and equity used to run and develop a company. It generally determines financial leverage, risk profile, and total cost of funds. Therefore, companies seek optimal capital structures, which assist the organisations in growing while keeping the risks in check.

Components of Capital Structure

It shows how much debt can secure a firm with equity. In financial terminology, the ‘debt-equity ratio’ indicates how much debt a firm uses relative to its equity, thus providing an understanding of how a firm handles its capital mix. High financial leverage is understood to offer higher returns but increases the chances of a distressed financial position. Thus, companies need to exercise careful capital structuring to maintain a healthy balance in this context. Two broad components constitute the capital structure:

- Debt: Borrowed funds, meaning bonds, loans, and other borrowed capital asset tax shields that reduce the total taxable income of the company.

- Equity: It is the fund raised from the shareholders through common or preferred stock. Equity does not require repayment but dilutes ownership.

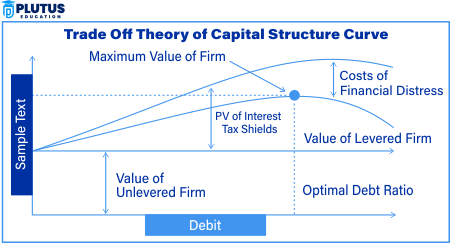

Trade-Off Theory in Capital Structure

According to the trade-off theory of capital structure, firms determine their levels of debt and equity by weighing all the benefits and drawbacks of debt. Potential corporate financing methods include debt: Companies use them to take a tax benefit but avoid unrestrained use, which will trigger bankruptcy costs.

Key Aspects of the Trade-Off Theory

All of these must be balanced so that an enterprise is financially stable and can have sustainable growth opportunities.

- Tax Shield – interest paid on debt is tax-deductible, causing an overall decrease in taxable income and tax expenses.

- Financial Distress Costs – High debt levels increase the risk of bankruptcy, which induces financial instability and decreases firm value.

- Agency Costs – W.R.t “profit maximisation”, debt may be an effective means of controlling managers, but excessive debt leads to conflicts between shareholders and creditors.

- Static Trade-Off Theory states that firms are trying to reach an ideal level of indebtedness and would adjust to weigh against the tax benefits with distress costs.

- Dynamic Trade-Off Theory – Firms would adjust their capital structure as circumstances evolve.

Balancing Debt and Equity in Trade-Off Theory

An optimal capital structure maximises a firm’s value and minimises the cost of capital. Optimality is subject to the type of industry, conditions in the market, and risk variables internal to a firm.

Factors Influencing Optimal Capital Structure

- Industry Norms – Different industries have various levels of acceptable financial leverage.

- Market Conditions – Interest fixed above market cost will change occasionally due to economic fluctuation.

- Staging of Growth of the Firm- Startups rely much on equity, while matured firms may resort to debt because they have stable earnings.

- Risk Tolerance- Several companies have relatively stable cash flows to afford high debt levels without the risk of financial distress.

- Regulatory Environment – Government policies shape tax rates in addition to borrowing conditions.

Strategieforof Attaining Optimal Capital Structure

- Maintenance of Debt and Equity Ratios – It is recommended that firms keep track of their debt-to-equity ratios to ensure they are well-balanced.

- Minimising Cost of Capital – A combination of debt and equity has to lower overall financing costs.

- Managing Financial Distress– Reduce debt levels to avoid liquidity and its resultant business failures.

Trade-Off Theory Vs Pecking Order

The trade off theory of capital structure often compares with the pecking order theory, which extensively explains the choices made for financing with the cost and the ease of obtaining such. Differences between the theories are as follows:-

| Feature | Trade-Off Theory | Pecking Order Theory |

| Decision Basis | Balances tax benefits and bankruptcy costs | Prefers internal financing first |

| Debt vs. Equity | Chooses debt based on cost-benefit analysis | Uses debt only when internal funds are insufficient |

| Flexibility | Adjusts debt levels over time | Hierarchical financing preference |

| Managerial Implication | Encourages maintaining a target debt-to-equity ratio | Prioritises financial flexibility |

From the point of view of the theory relating to hierarchy in pecking orders, it advocates that by using minimal retained earnings, a firm has to resort to debt and, finally, equity, which is here. However, the trade off theory on capital structure argues for maximising the possible use of debt and equity in assigning benefits and costs.

Relevance to ACCA Syllabus

The trade-off theory of capital structure is highly relevant to ACCA as it is integral to financial management, risk assessment, and corporate finance decision-making. ACCA students must understand how firms balance debt and equity financing while considering the costs and benefits, such as tax shields and bankruptcy risks. This knowledge is applied in financial strategy, risk management, and corporate reporting, making it crucial for exam success and real-world financial decision-making.

Trade-Off Theory of Capital Structure ACCA Questions

Q1: According to the trade-off theory of capital structure, why do companies prefer a balanced mix of debt and equity?

A) To maximise operating efficiency

B) To achieve an optimal balance between tax benefits and bankruptcy costs

C) To ensure maximum shareholder dividends

D) To eliminate financial leverage

Ans: B) To achieve an optimal balance between tax benefits and bankruptcy costs

Q2: Which financial management decision is most directly influenced by the trade-off theory?

A) Investment decision

B) Financing decision

C) Dividend policy

D) Working capital management

Ans: B) Financing decision

Q3: According to the trade-off theory, what is a key advantage of debt financing?

A) It avoids dilution of ownership

B) It reduces financial risk

C) It eliminates bankruptcy risk

D) It increases operational efficiency

Ans: A) It avoids dilution of ownership

According to the trade-off theory, what is the main downside of excessive debt?

A) Higher corporate tax payments

B) Increased risk of bankruptcy and financial distress

C) Lower financial flexibility

D) Decreased equity financing

Ans: B) Increased risk of bankruptcy and financial distress

Q5: In the trade-off theory, which of the following represents a cost of financial distress?

A) Increased market share

B) Decreased interest expenses

C) Legal and administrative costs of bankruptcy

D) Reduction in the debt tax shield

Ans: C) Legal and administrative costs of bankruptcy

Relevance to US CMA Syllabus

The trade-off theory is critical in the US CMA syllabus as it helps management accountants understand how financial leverage affects a company’s profitability and risk. The CMA syllabus covers financial decision-making, risk management, and corporate finance, where students learn how firms choose between debt and equity while balancing financial risks and benefits.

Trade-Off Theory of Capital Structure US CMA Questions

Q1: According to the trade-off theory, what is the primary reason firms take on debt despite financial distress risks?

A) To reduce capital costs by taking advantage of interest tax shields

B) To increase operational flexibility

C) To maintain high liquidity

D) To avoid issuing new shares

Ans: A) To reduce capital costs by taking advantage of interest tax shields

Q2: Which of the following best represents a company’s capital structure decision under the trade-off theory?

A) Balancing financial risk and tax benefits from debt

B) Relying only on retained earnings

C) Eliminating long-term debt from financing

D) Prioritizing dividend distribution over capital investments

Ans: A) Balancing financial risk and tax benefits from debt

Q3: Which statement best describes the impact of high financial leverage on a firm’s cost of capital?

A) It initially reduces the cost of capital due to tax benefits but increases financial distress costs over time

B) It eliminates the cost of equity

C) It has no impact on the firm’s financial risk

D) It makes debt the cheapest source of financing indefinitely

Ans: A) It initially reduces the cost of capital due to tax benefits but increases financial distress costs over time

Q4: What happens when a company takes on excessive debt under the trade-off theory?

A) The firm’s value continues to increase indefinitely

B) Bankruptcy costs may outweigh the tax benefits of debt

C) The cost of equity financing decreases significantly

D) The company eliminates financial distress risk

Ans: B) Bankruptcy costs may outweigh the tax benefits of debt

Q5: Which financial metric is most useful when evaluating trade-off theory implications?

A) Return on Assets (ROA)

B) Debt-to-Equity Ratio

C) Price-to-Earnings (P/E) Ratio

D) Operating Margin

Ans: B) Debt-to-Equity Ratio

Relevance to US CPA Syllabus

Understanding the trade-off theory is crucial for US CPA candidates as it is fundamental to corporate finance, taxation, and risk assessment. The CPA syllabus emphasises financial decision-making, cost-benefit analysis, and the impact of leverage on economic health.

Trade-Off Theory of Capital Structure US CPA Questions

Q1: Under the trade-off theory, why do companies use debt despite potential risks?

A) To maximise equity financing

B) To take advantage of interest tax shields while managing bankruptcy risks

C) To ensure low operational costs

D) To eliminate the need for retained earnings

Ans: B) To take advantage of interest tax shields while managing bankruptcy risks

Q2: Which cost is associated with excessive leverage under the trade-off theory?

A) Reduced dividend payouts

B) Higher financial distress costs

C) Increased net income

D) Improved cash flow predictability

Ans: B) Higher financial distress costs

Q3: Why do firms not rely solely on debt financing despite its tax benefits?

A) Debt financing has no advantages

B) Interest rates remain constant over time

C) Excessive debt increases the probability of financial distress and bankruptcy

D) Tax savings are unlimited

Ans: C) Excessive debt increases the probability of financial distress and bankruptcy

Q4: Which financial ratio is most important for analysing capital structure trade-offs?

A) Gross Profit Margin

B) Debt-to-Equity Ratio

C) Accounts Receivable Turnover

D) Quick Ratio

Ans: B) Debt-to-Equity Ratio

Q5: A company following the trade-off theory will finance its operations by:

A) Using only retained earnings

B) Balancing debt and equity to optimise tax benefits and minimise bankruptcy risks

C) Eliminating long-term liabilities

D) Increasing dividends at the expense of debt reduction

Ans: B) Balancing debt and equity to optimise tax benefits and minimise bankruptcy risks

Relevance to CFA Syllabus

The trade-off theory is a core part of the CFA syllabus. It helps candidates understand how firms make capital structure decisions based on tax benefits, financial distress costs, and overall firm value. It is a key topic in corporate finance and investment analysis, impacting how financial analysts assess firms’ risk-return trade-offs.

Trade-Off Theory of Capital Structure CFA Questions

Q1: According to the trade-off theory, what is the optimal capital structure?

A) 100% debt financing

B) 100% equity financing

C) A mix of debt and equity that maximises firm value while minimising financial distress costs

D) No capital structure is optimal

Ans: C) A mix of debt and equity that maximises firm value while minimising financial distress costs

Q2: According to the trade-off theory, which factors affect a firm’s capital structure?

A) Tax benefits from debt financing

B) Financial distress costs

C) Both A and B

D) Neither A nor B

Ans: C) Both A and B

Q3: What is the primary reason firms limit their use of debt in capital structure decisions?

A) Debt has no financial advantages

B) Bankruptcy and financial distress risks increase with excessive leverage

C) Interest expenses are not tax-deductible

D) Equity is always a cheaper financing option

Ans: B) Bankruptcy and financial distress risks increase with excessive leverage

Q4: According to the trade-off theory, which statement is true?

A) Firms always prefer debt over equity

B) Tax shields increase firm value, but excessive debt increases bankruptcy risks

C) The Modigliani-Miller theorem states that capital structure is irrelevant

D) Debt financing is always risk-free

Ans: B) Tax shields increase firm value, but excessive debt increases bankruptcy risks

Q5: Which metric is best for assessing the impact of leverage in trade-off theory?

A) Earnings Per Share (EPS)

B) Interest Coverage Ratio

C) Dividend Yield

D) Inventory Turnover

Ans: B) Interest Coverage Ratio