Trading and settlement are two of the most significant elements of the stock market. It refers to the process of buying and selling securities such as stocks, bonds, and derivatives in the market. In simple words, settlement is basically the process of passing the ownership of the securities from the seller to the buyer. It is evident that without an effective trading and settlement procedure, a financial market would not be efficiently efficient, transparent and risk-free. Among the processes involved in this trading and settlement procedure are order placement and executing the order, clearing the trade, and final settlement. Investors and traders must understand well about the trading and settlement procedure in detail to have effective trading in the stock market.

Trading Procedure

Trading is at the heart of activities undertaken by the stock exchange. It offers an exchange platform through which securities can be sold or bought in an organized manner. The steps involved in leading to smooth execution, price discovery, and change in ownership are as described above. Being aware of the process that involves trading and settlement, full involvement in the market has always been imperative to investors. It is only when a coordinated securities trading and settlement process is achieved that stability is given to a market and risks are reduced to the lowest possible level on behalf of those involved.

Step 1: Opening a trading and demat account

Investment in the stock markets would require an investor to open a trading account and a demat account with a registered stockbroker. For placing buy/sell orders, one will make use of a trading account, while a demat account would house “dematerialized” securities in electronic form; thereby, one need not carry share certificates around. An investor has to opt for a SEBI-registered broker and is required to pass through the KYC process. KYC consists of proof of identity, which could be an Aadhaar or PAN card, proof of address, and bank details. After verification, the investor receives a unique client ID through which he can place trades on the online trading platform or offline brokerage services.

Step 2: Deposit Funds in the Trading Account

In the first step, the investor has to deposit sufficient funds into the trading account. Then, at that point, it would be decided how much amount can be purchased by the investor. Almost all stockbrokers accept many modes of payment like net banking, UPI, NEFT, RTGS, and digital wallets so that faster transactions take place. Another facility that some brokers may offer would be margin trading, which allows investors to buy securities while borrowing from them. Margin trading is not risk-free because one needs to maintain a minimum balance to avoid position liquidation.

Step 3: Research and Stock Selection

After opening the trading account, investors research and select stocks before placing orders. Investors can get to know how well a company performs through the use of fundamental analysis that involves reviewing financial statements, market trends, and growth potential in business. Some investors use technical analysis based on price charts, historical data, and the patterns in the stocks to predict future prices. Investors obtain current, real-time stock market information, advice from experts, and other financial news to guide their decisions through brokers.

Step 4: Buy/Sell Order.

After identifying which stock to invest in, the investor could send his order to buy or sell to a stock exchange through a broker. A stock exchange offers types of orders as a way of satisfying the different intentions of the buyers.

- Market Order. The seller and buyer may sell and sell immediately for whichever price is offered to the stock that is open by the market.

- Limit Order. This type of selling and buying happens only when an investor agrees on the price.

- Stop-Loss Order: Automatically trades the stock with a set earlier level to control extreme losses that may be accumulated.

- Intraday Order: Stock bought as well as sold within the day of trading itself

- Delivery Order: The investor has the purchased share as an investment for the future.

Once an order is placed, it stays in the system till there is a matching order. There is an order status one can see of his order at the trading platform of the broker.

Step 5: Order Matching and Trade Execution

The electronic trading system of the stock exchange starts searching for a matching order within seconds of the order’s entry. A buy order is instantly traded if the order of purchase matches an order of sale with the same price and quantity. The exchange ensures that the trade follows the trading and settlement procedure in the stock exchange, as well as the rules set by SEBI. Upon the completion of the trade, the stock exchange sends a confirmation message of the trade to the broker and investor.

Step 6: Confirmation of trade and Contract Note

On receiving confirmation of the trade, both the buyer and seller advise their brokers that they have received confirmation of the trade. The broker then issues a legal document called a contract note. The note contains the following details:

Description of the trade (name of security, amount, and rate)

Brokerage charges and trading fee

The time at which the trade is executed and trading information on the stock exchange

A unique serial number refers to the order of the trade transaction.

All the points must be evident in the contract note so that it can be examined; if there have been some wrong details, then those brokers must immediately be informed.

Step 7: Trade Being Directed to the Clearing House

After various traders perform the deal, then that specific stock exchange will send a report of respective trades for clearing at one clearing house or clearing corporation.

A clearing corporation is an intermediary agency acting between two parties- a buyer and a seller- and it provides assurance. The parties commit their trade commitment. It highly reduces the chances of counterparty risks. NSE, the National Securities Clearing Corporation Limited, clears and settles on its behalf while it is facilitated on its behalf of BSE by the Indian Clearing Corporation Limited. It verifies the trade, which depends upon the terms and conditions mutually agreed between the two parties. Thereafter, the amount payable by a buyer and the deliverable security of the seller is computed.

Step 8: Margin Requirement and Risk Management

The clearing house checks whether margins in the trade accounts of both buyers and sellers are adequate to forward the trade for settlement. This is the advance deposit made before trade to avert default. The margin that is agreed upon depends on the price volatility of a stock, market condition, and volume. More funds have to be deposited if the trader’s margin falls below this threshold; otherwise, the broker may liquidate the position.

Step 9: Deposit of funds and blocking of securities

Once the margin has been covered, just after one or two days, the clearing house debit entry has to be made in the buyer’s trading account based on the amount bought. Also, the seller’s demat account has to be temporarily blocked regarding the number of securities sold. It is so because, at this step, both parties settle their respective liabilities for final settlement.

Step 10: Netting and Settlement of Contracts

The clearinghouse will apply netting, where the different transactions are added together to yield the resulting liabilities. There is no separate settlement of transactions; the net payable or payable amount is settled with every single participant. All these reduce the volumes of transactions, the time to clear and settle is speeded up, and the market benefits with higher liquidities.

Step 11: Settlement and Change of Ownership End

On the settlement date, the securities and funds actually get exchanged. The seller’s blocked shares will be credited to the buyer’s demat account, whereas the proceeds of the sale are credited to the seller’s bank account. Here, the cycle is T+1 in India, which means one working day after the execution of the trade. This means that if the trade has been executed on Monday, then settlement will be made on Tuesday.

Step 12: Post-Settlement Reconciliation

The investors should reconcile their demat and bank accounts so that the securities and funds get transferred properly after settlement. The trade and settlement reports submitted by the brokers will guide the investor while reconciling so that they can ascertain accuracy. Any discrepancy should be immediately brought to the notice of the clearing house or broker.

Step 13: Auction and Closeout for Failed Trades

In case a selling member fails to provide the underlying security, the auction process for the purchase of difference is initiated by the exchange from the open market. If the price bid at an auction turns out to be above the original trading price, it penalizes the seller by demanding the difference in addition. The netting formula compensates the buyer while closing out. If the shares do not materialize in the auction, then the loss from the investor is lost due to failure in delivery.

Step 14: Compliances and Record-Keeping

All the trades after settlement will be maintained by the broker-investor for tax and audit purposes. Stock exchanges and clearing houses also prepare compliance reports to ensure that the trading and settlement procedure in the stock exchange meets the regulatory norms. Investors need to maintain the contract notes, transaction records, and their respective demat account statements for future reference.

It is a well-defined sequence that also underlines the process of trading, which ensures the transparency, efficiency, and security of stock market transactions. It enables investors to understand the process so that they can make the right decisions and enter the stock market with confidence.

Stock Exchanges in India

The regulated and transparent stock exchanges provide a platform for trading in securities. Major stock exchanges in India are two, namely the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE). Both these exchanges operate a well-defined trading and settlement of NSE and BSE process that guarantees smooth trade execution and ownership transfer.

National Stock Exchange (NSE)

The NSE was established in 1992 when the open outcry system in India was to be completely revamped with the dream of taking electronic trading to India. The NSE is one of the world’s largest stock exchanges trading equities, derivatives, commodities, and currency trading. The benchmark index of the NSE is Nifty 50, holding the top 50 companies in the list of the exchange. NSE has a T+1 settlement cycle where the trades settle one business day after the execution. SEBI regulates the exchange for investor protection and for fair trade.

Bombay Stock Exchange

BSE was founded in 1875, and it is Asia’s oldest and one of the world’s largest stock exchanges, with more than 5000 listed companies. The Sensex is the benchmark index of BSE that covers 30 of the primary key companies of many industries. An exchange takes place through the state-of-the-art electronic trading platform BOLT, which acts as an arm of BSE Online Trading; extremely prompt trade executions are delivered. The BSE has a very high sensitivity of integrity in the market as well as investors’ confidence because all the rules imposed by SEBI are strictly followed at BSE. T+1 settlement cycle is adopted even at NSE. The cycle offers a fast transfer of ownership.

Trading Mechanism

Trading mechanism refers to the process through which security purchasing and selling take place on the stock exchange in an orderly fashion. This gives market efficiency, liquidity, and price determination based on fair valuation. Mechanisms within this category comprise several orders, trading sessions, and how price is determined.

Orders Types

There are many different types of orders that may take place in the trading of securities for executing stock market transactions in conformity with strategy. A market order is completed at the best available price so that the trade can be consummated right away. A limit order permits investors to buy or sell at a predetermined price, which offers better control over the execution of the trade. A stop-loss order automatically sells a stock when its price has fallen below a given threshold and thus minimizes potential losses. Intraday trading occurs when the security bought is sold back on the same trading day; delivery-based trading is when a stock bought is held for an extended period by the share buyer.

Trading Sessions in the Stock Market

A stock exchange trades throughout the whole day. It operates during the entire session to determine its opening price based on demand and supply. It is during this session that the usual buying and selling occurs most of the time. This post-closing session enables the investors to update their orders, and the settlement will be computed using their official stock prices at closing.

What is the Settlement Date?

Settlement date is that date when the last date securities and funds transferred from a seller to a buyer; that means when the trade is complete. The Indian stock exchanges adopt the T + 1 settlement cycle, and after the completion of the one working day, the securities are collected which is called the settlement date. Guarantee by clearing house guarantees all payment in order to avoid a higher risk of default. The date of settlement informs the investor whether he needs to make a balance of funds and securities. Penalties or cancellation of a trade will be the case if such is not made on time.

Procedure for Settlement

The settlement procedure ensures that all blockades resulting from the transfer of security and funds after an execution transaction are cleared. All market participants should be aware of the trading sequence as well as the settlement procedure. Steps of the Settlement Process

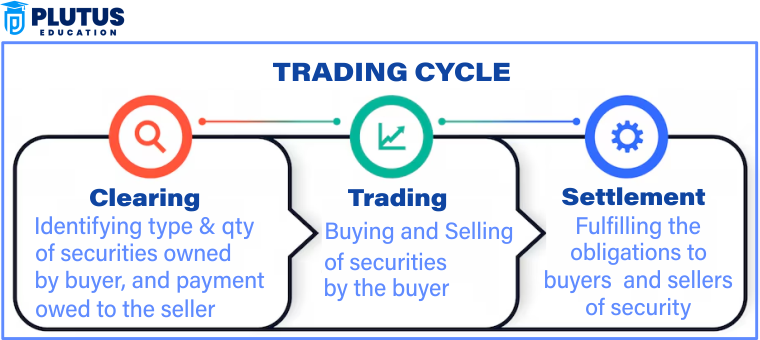

The settlement process is a proper process that is conducted following the settlement of the trade to achieve the accomplishment of transferring securities and cash accurately. One’s understanding regarding trading and way of settlement is crucial at a stock exchange and thus for every investor since his every trade does not get spoilt in any way. With these factors in mind, the settlement process actually involves a number of stages that include trade execution, trade confirmation, clearing, settlement, and transfer of funds and securities. A successful arrangement for a securities trading and settlement system reduces several risks and ensures that each entity discharges financial obligations.

Step 1: Trade Execution

Actually, the settlement process starts when an opposite sell order matches the buy order of a trade executed in the stock exchange. In case an investor gives an order to buy or sell securities, then the trading system of the stock exchange matches it with an opposite order. Assume that an investor orders to buy 100 shares of a particular company at ₹500 per share, and another investor has placed an order to sell the same number and price. The trade will be completed then. At this stage, the transaction locks in, and ownership transfer waits until the trade is settled.

Step 2: Confirm the Trade

Confirmation of the trade is received by the buyer and seller from their respective stockbrokers after confirmation of the trade. A legal document that confirms the trade and a contract note are issued by the stock exchange. This note includes the most basic information related to security name, quantity, price, time of trade, brokerage charges, and settlement obligations. The investor must authenticate the Contract Note to determine whether it is correct or not as per the trade order. He has to inform a broker about mismatches as soon as possible for any settlement issues arising from that cause.

Step 3: Processing through Trade reporting and Clearing House

Once the trade is confirmed, the clearing house- the National Securities Clearing Corporation Limited(NSCCL) for NSE and Indian Clearing Corporation Limited(ICCL) for BSE- will step in. The clearing house acts as a go-between a buyer and a seller so that risk-free settlement can take place. It collects trade data from the stock exchange and determines the financial obligations of each party. For example, it would specify the precise amount that the buyer should be charged and what number of securities the seller is liable to deliver to the clearing house. In this practice, the clearing house protects both, and if one doesn’t pay, then the other suffers at least minimal loss in monetary terms.

Step 4: Margin Requirement and Risk Management

The clearinghouse will need to settle the traders and brokers; this means that the latter has to carry a margin before the trade is allowed to go through. A margin can be termed as an advanced payment between the buyer and the seller regarding the transaction at hand so they can carry out their obligations to the trade. All these have three types that are initial margins, mark-to-market margins and exposure margins, and all these have been used for the protection of some risks of market price fluctuation and default; if a broker fails to retain the required amount of margin to hold the amount, then there is a trading that is required to be square off to have a loss protected.

Step 5: Netting of trades.

The clearinghouse maintains a netting system through which the trades made in multiple on the same security are offset to determine the net obligation of every trader. Here, the trades are instead determined by the number calculated for each participant of the net payable or receivable. For instance, if a trader has bought 200 shares of some company and sells 100 on the same day to another trader on the same side, the clearing house will consider the net position of just 100. Netting simplifies procedures and reduces securities volumes exchanged-which makes for an efficient system.

Step 6: Funding and Securities blocking

It freezes the amount in the buyer’s account for that particular fund, thereby locking up the securities in the seller’s demat account. This ensures that all the obligations are satisfactorily settled. The buying party needs to provide a balance in his trading account. The selling party needs to keep the securities liable for transferring them. If this is not complied with by either of the parties, the penalty would be imposed against him, and the trade would be reversed.

Step 7 Settlement of securities and funds

This settling of securities and funds is based on the settlement date. Such securities get credited to the buyer’s demat account, and at the same time, the sale proceeds are credited to the seller’s bank account. T+1 is followed in India for settlement, which means a business day subsequent to the day of trade execution. If, on Monday, such a trade took place, settlement would be performed by Tuesday.

Step 8: Post-Settlement Reconciliation

After settlement, brokers and traders have to check whether all the securities and funds have been correctly transferred. Investors have to check their demat and bank accounts to ensure whether the shares bought are credited and whether the payments received are correct. In case of any discrepancy, they have to inform the clearing house or the stockbroker. Thus, no error or fraudulent activity will reach the investor’s portfolio.

Step 9: Failed Trade Auction and Closeout Process

If a seller fails to deliver the number of securities he promised, the stock exchange initiates an auction process from the market. In this, the defaulting seller would be penalized while the buyer is allowed the shares at the price of the auction. Even in the auction, if the securities are not available, the stock exchange will compensate the buyer based on the predetermined closeout formula. Based on this procedure, the buyer will not incur any loss in case of a defaulting seller.

Step 10: Final Reporting and Compliance

After the final settlement of all the transactions, the stock exchange and the clearing house file a final report with the authority to take action for compliance purposes. These reports carry information about the trades conducted, status settled, margin information and penalty levied. The brokers and the investors should maintain these accounts for audit and tax purposes. The stock exchange also ensures that the entire trading and settlement process remains within the legal perimeters of SEBI. Hence, the market is assured to be a safe and transparent place.

All these trading and settlement steps ensure that all the transactions go through with no risks involved. On its part, the stock market provides for easy transfer of ownership, financial stability, and confidence in investment.

Emerging Trends in Trading and Settlement

An improvement in technology and regulations also brought changes to trading and settlement cycles under the stock exchange. Faster and more secure settlements have also been supported due to innovation that has taken various forms of a T+1 settlement cycle, blockchain, artificial intelligence, or algorithmic trading. All is a step ahead toward reducing risks associated with a procedure to help make the entire process efficient. Transparency in dealing with the financial markets also brings a smooth condition for investors in order to ensure that trading with the financial markets is reliable.

Introduction of T+1 Settlement Cycle

The new T+1 cycle replaces the old T+2 cycle. This reduces the settlement cycle, and therefore, the transaction is completed within a business day. Investors would get securities and funds within one business day under this cycle, as against earlier. This enhances liquidity, reduces counterparty risks, and makes the market more efficient. Simultaneously, it also presents a challenge for foreign investors because, due to this short cycle, they have to shift their whole process of transferring funds.

Blockchain Technology in Trading and Settlement

Blockchain offers an entirely decentralized and transparent system for transforming securities trading and settlement. In blockchain-based transactions, the transactions are tamper-proof; hence, fraud is eliminated, and delay in settlement is minimized. Blockchain removes the intermediaries that incorporate clearing houses; thus, the transaction cost is reduced while settlements are accelerated. Most stock exchanges around the world, including India, are also experimenting with blockchain to improve the trading process.

AI Algorithmic Trading

Through AI and algorithmic trading, merchants can trade with incredible speed using data-based strategies. The system powered by AI scans the market for trends of price movement, which helps predict and, consequently, make automatic trading decisions. It brings faster, accurate, and emotionless trading to the market and thereby creates liquidity within it. However, AI-based trading also raises some concerns, such as sudden price movements and regulatory oversight.

Digital Payment Systems and Real-Time Settlement

Hence, UPI and instant bank transfers streamlined the trading and settlement process with digital payment systems. Real-time transfer will make sure that the money and the securities are released to investors within no time. Many stock exchanges are formulating real-time gross settlement systems in order to expedite it faster. Instant settlements will decrease the financial risks and will increase investor confidence.

Regulatory Changes and Investor Protection

SEBI formulated regulations that authorize regulation bodies to protect investors against all types of scams and other forms of manipulation in the markets. Some include margin and surveillance in high-frequency trading. Another initiative, the investor education programs, enhances literacy in finance, among others; all these impact the reduction of fraud and ensure safe trading at the stock exchange.

Implementation of Cloud Computing and Big Data on Trading

The whole process allows significant volumes of trading data to be speedily processed over the stock exchanges and brokers’ desks. Therefore, the ability of big data analytics will make a forecast to the investor about the market’s trends, provide optimization in a portfolio, and make proper choices. This again increases trading and reduces errors as well as malicious activities. More financial institutions have started to make use of more cloud-based environments for faster trade operations and improved securities.

Prospects of Trading as well as Settlements

Futures trading and settlement will be blockchain- and AI-centric. All settlements will become as real-time and automated as possible. Stocks will trade much more quickly, securely, and accessible to institutional or retail traders. With any evolving technology, the regulators face the challenge of innovation and investor protection: trading will then be faster and more transparent; it gets only cheaper through continuous improvement.

Trading and Settlement FAQs

1. What is Clearing and settlement process ?

Clearing and settlement enable placing and executing the trades along with transferring the ownership.

2. What is security trading and settlement?

Trading of buying or selling shares, bonds and derivative products through the proper exchange of securities with sufficient funds, therefore, termed as aptly as buying or selling.

3. What are the Phases of a trading and settlement procedure?

It is the process that involves trade execution, clearing of obligation, and settlement that requires the exchange of securities and money.

4. What is a trading and settlement at NSE and BSE?

Both exchanges settle at T+1, and therefore, all trade executions are squared within one working day after executing.

5. What is a trading and settlement process in the stock exchange?

The process includes an order, execution of the trade, clearing obligations, and final settlement under SEBI regulations.