A fundamental principle of financial statement presentation, it allows for the accurate representation of the financial position,. Also performance, and cash flows into material misstatements and biases of any persuasion. Hence, giving an honest picture of the state of any concern to all its stakeholders-including investors, creditors, and regulators. To state it plainly, the true and fair view in auditing . It is free of error and manipulation and gives the correct picture of the company.

This established concept helps build the foundation of trust for the users of financial reporting. Auditors must ensure that financial statements meet accounting standards and provide reliable information to users. The article discusses what the true and fair view means in auditing, its importance, the auditor’s responsibility, the true-and-fair view versus compliance distinction, the meaning of true and fair override in auditing, and what auditors do in forming a judgment of financial statements.

True and Fair View in Auditing

With a true and fair view, an auditor is supposed to give a guiding principle for constructing a reliable picture in truth and honesty by which investment or financial statements reflect economic activities accurately. It demands the presence of some feature in the financial information that makes it ensure reliability and comparability and then leads to transparency in that information about which it should help in decision-making by interested parties or users.

In this, the auditors would see that the financial statements are elaborated according to accounting standards and regulatory requirements. A true and fair view does not mean the financial statements are free of errors, but rather, they are free of material misstatements, which, if there were, could mislead the user. The financial statements must mirror the actual financial health of the company concerning its assets and liabilities, as well as income and expenses.

A true-and-fair view must be achieved following Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). A mere true-and-fair view should also give users an understanding of financial information. Obscuring financial information with technical particulars will misconstrue the users’ experience. Therefore, financial information must be presented clearly and in an orderly to facilitate stakeholders’ accurate interpretations of the information. Such clarity sustains their decision-making and keeps them secured from the correspondence of financial reporting regulations.

Importance of True and Fair View in Financial Reporting

A true and fair view is essential for ensuring that financial reports are transparent and credible. It guarantees that the financial statements present a true and fair picture of a company`s financial health, which is vital for stakeholders.

Investor Confidence

Financial statements are the tools investors use to evaluate a company’s profitability and economic stability. With a true and fair view, an investor makes a well-informed decision about buying, holding, or selling the shares. In cases where the financial statements are misrepresented, it is likely that the investor would bear the brunt and may suffer losses.

Lender Trust

Lenders first look into the company’s financial statements before loaning funds. The true-and-fair view will provide lenders with reliable financial information to gauge a company’s ability to repay debts.

If creditors lend to financially weak companies due to the oversight of financial statements, this can place those creditors at an increased risk of default. Bad debts and subsequent economic loss to banks would be the result. Conversely, honest disclosure of financial statements enables creditors to make informed lending decisions, leading to a stable credit market and better business relationships.

Data on Regulatory Compliance

Regulators verify whether corporations comply with accounting standards and legal requirements in all dealings. If companies stay true and fair, they can meet all compliance requirements while limiting the possibility of penalties and legal actions.

The regulators such as Securities and Exchange Commission (SEC) or Financial Reporting Council (FRC) check whether the compliance of financial reporting standards is being maintained. If a company does not prove true and fair, then it faces the risk of being taken to court, fined, or very unlikely delisted from the stock exchange. Financial transparency protects the corporation against such legal liability and provides it with a credible reputation in the market.

Business Decision-Making

Management uses financial statements as a basis for key decisions. A true-and-fair view gives accurate data for a clear basis for the plans related to investments, allocations of resources, and risk management.

Managers depend on financial reporting to identify value allocation, pursue expansion strategies, and measure cost optimization. When such information is untrue, it will portend detrimental decisions, which may lead to malfeasance, losses, and inefficiencies in the organizations. The true-and-fair view helps organizations adopt realistic ways of goal achievement, strengthening the development of their financial plans.

Prevention of Fraud

On the contrary, a true and fair view discourages financial manipulations and frauds. It firmly requires financial statements to reasonably articulate the respective business transactions, leaving little or no room for unethical practices such as profit inflation or hiding liabilities from view.

Corporate scandals like the Enron and WorldCom cases remind us harshly of the consequences of financial fraud. If a company engages in the manipulation of financial statements, investors and regulators are misled, and the result is a massive economic and legal bludgeoning.

Auditor’s Responsibility for Ensuring a True and Fair View

The auditor verifies whether the financial statements give a true and fair view. Such an auditor has to look at his commitment to checking financial documents, his understanding of all the inquiries, and to draw a small, independent opinion that is free from material misstatements for the client’s financial statements.

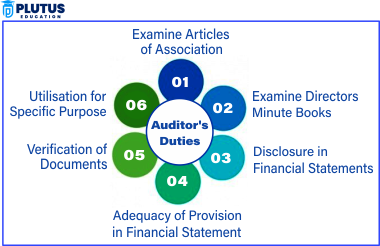

Risk Assessment

This is defined as risks that auditors encounter in auditing one’s client’s financial statement. They argue that risk includes loss due to fraud, mistakes, and weak internal controls. Risk assessments should bring undue exposure to auditors to the highest-risk areas.

Practical risk assessment allows the auditor to focus on areas with an increased chance of error or fraud. Through such assessments, auditors give a picture view of the organization’s financial health most accurately in financial statements. If the risks are ignored, the financial statements can mislead the stakeholders, resulting in economic losses and legal actions.

Evaluating Accounting Policies

Auditors examine the client’s accounting policy to check whether it conforms to GAAP or IFRS. It also considers whether the policy has been applied consistently and relatively to all transaction entries.

The policies should be uniformly applied within an organization, as confusion might result from differing policies. Frequent changes in the application of these policies or erratic applications might lead to the misrepresentation of financial statements. The auditor traces deviations and ensures financial reporting reflects the true and fair view on a standard policy adherence basis.

3Verifying Financial Transactions

Auditors check the accuracy of financial records by partnering with invoices issuing receipts and contracts. This involves checking whether the financial transaction is recorded correctly and whether the exact financial position of the company is reflected in it.

Verifying financial transactions assists in detecting fraud, such as fake invoices, overstated revenue, or hidden liabilities. Without correct, highly detailed, effective, and accurate financial records, an accurate and true picture of reality will be denied in financial statements. It will mislead both investors and regulators.

Evaluation of Laws and Regulations Compliance

Auditors ensure that the financial statements serve legal and regulatory purposes, such as taxes, corporate laws, and other forms of industry-specific regulation.

Legal non-compliance can be a source of financial penalties, loss of business licenses, and reputational damage. Auditors confirm that financial reporting complies with all applicable regulations, taking care further to protect businesses from legal risks.

Reporting Findings and Issue of Audit Opinion

After the auditors audit the financial statements, they write and present an audit report. Different opinions are given about the statements of various companies the auditors have gone through.

- Unqualified Opinion: Financial statements are said to provide a true and fair view.

- Qualified Opinion: Financial statements have some issues, but they have not gone to the extent of being highly misleading.

- Adverse Opinion: The financial statements are materially misstated and do not provide a true and fair view.

- Disclaimer of Opinion: The auditor cannot express an opinion due to a lack of evidence.

Audit opinions have a bearing on the credibility as well as the financial stability of a company. True and fair views help maintain investor trust, but an adverse audit opinion can lead to a drop in stock prices and regulatory scrutiny.

True and Fair View vs. Compliance

True and fair views vs. compliance are often mixed up with one another, but they define two different audit concepts. Compliances ensure that the financial reports are perfectly prepared according to the law and regulation used; however, a true and fair view stretches further than compliance as it assures that the financial statement genuinely shows the actual financial position and performance of the organization. Understanding these two concepts’ differences can be essential for businesses, auditors, and stakeholders.

| Aspect | True and Fair View | Compliance |

| Definition | Ensuring financial statements reflect the actual financial position and performance. | Adhering to legal and regulatory financial reporting requirements. |

| Objective | Providing accurate and unbiased financial information. | Meeting the minimum legal and regulatory requirements. |

| Focus | Transparency, reliability, and fair representation. | Following accounting rules and regulations. |

| Flexibility | Allows judgment in presenting financial information. | Strict adherence to laws and standards. |

| Impact | Builds trust among investors, creditors, and stakeholders. | Ensures companies avoid legal penalties and regulatory issues. |

Goals for True and Fair View

It will clear the financial representation of an entity and keep it very realistic to all stakeholders. Compliance keeps the company within the legal framework of the regulation but does not imply that its financial statements will reflect its economic reality.

- A firm would comply with the accounting standards, but there can still be no true and fair view when the financial statements do not reflect the actual economic condition of the established company.

- Mostly, the time when strict adherence to accounting policies tends to hallucinate the financial reality. Sometimes, the unruly application of accounting rules distorts financial reality.

- For instance, according to the accounting standard, a particular set of depreciation methods is prescribed, but their imposition results in misleading values in financial statements, so the company may need to use true and fair override to continue. Ultimately, it must be clarified whether the management override accurately shows the economic reality of financial statements and incorporates just technical compliance.

- In the case of unusual transactions or financial conditions that fall outside regular accounting treatment, a True and fair override is necessary to be entered into the record appropriately to reflect the company’s financial position properly when the type of financial transaction is so complex that it does not meet the ordinary definitional confines.

- For instance, if one entity gets hold of another by an unusual technique, no standard accounting treatment would apply correctly in his books.

What is True and Fair Override in Auditing?

True and fair overrides are available for situations in which the literal application of an accounting standard causes the financial statements to misinform or mislead the stakeholder community as to the position of the reporting entity at that time. An example pertains to instances in which the outdated valuation methods used by regulations do not adequately reflect what exists in the market, thus inducing the true and fair override.

Legal and ethical confines. But that does not mean every time a company can cleverly use the true and fair override, it will have to back it up with sound logic. Auditors scrutinize whether it is necessary to override accounting standards and whether doing so culminates in a true and fair view of financial statements. As usual, users usually find explicit reasoning for using the override shared in the financial statements.

How Auditors Will Evaluate Whether Financial Statements Are True and Fair?

Auditors resort to different techniques to verify if the financial statements properly portray a true and fair view. They might conduct detailed checks and use analytical procedures while assessing financial records to determine if there are significant or material misstatements and misrepresentations in the financial statements.

1. Analytical Procedures

Auditors compare financial data with different harmonically paired times, which detects any possible inconsistency. Analyzing trends, financial ratios, and all deviations will find potential errors, frauds, or unusual activities capable of affecting the accurate representation of the financial statements.

If the profit margin or debt-to-equity ratios have shown any sudden or unexplained changes, the auditor will investigate further. Anomalies have been identified. These often imply accounting errors, revenue from manipulations, or fraudulent transactions. Such results would be great for the auditors to identify such differences early before recording these discrepancies in financial statements that are likely not to reflect the true status of the company’s performance and economic standing.

2. Testing for Substance

Auditors substantiate the authenticity of every specific financial transaction, receipt, invoice, contract, and bank statement. This is to validate that each recognized transaction happened in reality and that receipts are accurate without fictitious or fraudulent transactions in the financial statements. Suppose the company has reported vast amounts of revenue. In that case, the auditor can then call for supporting documents such as sales invoices and customer contracts to ensure the alidity fofthat amount being declared aorthy of recording.

3. External Confirmations

Auditors shall contact external parties like banks, suppliers, and customers to corroborate financial balances. This will help verify whether cash balances, accounts receivable, and accounts payable are reported figures and not manipulated.

If the company claims a large cash balance, confirmation may be required from the bank to gain assurance. It can be suspicious if the statement given by the bank does not correspond with the company’s financial records. Similarly, confirmation through customers is done to auditors in verifying receivables, and this confirmation is extra evidence showing that financial statements portray a true and fair view.

4. Audit of Management

Estimates Management expects estimates to be more realistic, which is applied in depreciation, provision, and future earnings projections. The auditor views whether they are reasonable and necessarily comparable with potential industry best practices or related estimates.

For instance, when the company underestimates its expenses or overestimates future income, the financial statements will be much brighter than they are. Auditors analyze past trends, industry benchmarks, and external data to help determine whether management’s estimates are fair and free from bias. Should estimates deviate from reality, the auditors will dispute and ask for adjustments to keep the figures as accurate as possible.

5. Fraud Risk Assessment

Auditors assess the possibility of financial fraud by probing unusual transactions, examining related-party transactions, and testing inconsistencies in the economic data. They study whether there are indications concerning intentional misstatements or efforts for income manipulation with their analysis.

Financial statement-related talking about specific lines of cash transaction, off-balance-sheet items, and relatively uncommon journal entries. Concerning an entity’s related party transactions (like subsidiaries or family-owned enterprises), auditors check if such transactions occurred at fair market values. Any strange transaction that is not in line with standard business practice will be investigated further. Identifying and managing fraud risks ensures that frequent qualifications in financial reporting are minimized.

True and Fair View in Auditing FAQs

What does a true and fair view in auditing refer to?

A true and fair view in auditing means that financial statements clearly and credibly represent the company’s financial state without any material misstatements or biases.

What do you understand from a true and fair view?

It ensures transparency, builds investor confidence and protects against financial fraud by presenting accurate financial information.

What is the responsibility of the auditor for a true and fair view?

By verifying compliance with accounting standards, auditors employ various strategies to examine financial records, evaluate risks, and confirm transactions in a true and fair view.

What is the difference between true and fair view and compliance?

Compliance is the narrower legal requirement, while a true and fair view ensures that financial statements portray reality.

What is a true and fair override in auditing?

It allows deviation from accounting standards if applying such standards would result in downward misleading financial statements.