Audit risk refers to the chance that an auditor can wrongly deliver a clean opinion on financial reports, including material misstatements. The types of audit risk are inherent, control, and detection. Audit risk occurs whenever an auditor renders an improper opinion because of misstatements, fraud, or weakness in internal control. Recognizing these risks helps ensure a valid audit process. Auditors employ the audit risk model (ARM) to assess risk levels and enhance audit quality. The article will cover audit risk, audit risk categories, the audit risk model, its equation, and practical calculation examples.

What is Audit Risk?

Audit risk is the risk that the auditor will not be able to detect material misstatements in financial statements, thus issuing an incorrect audit opinion. It is a blend of factors that have the potential to impact the reliability and accuracy of financial reporting. Auditors utilize risk-based internal audit methods to recognise and control these risks. This implies the auditor can either:

- If mistakes or deceptions are not detected, give an unqualified audit opinion on financial statement misstatements.

- Recognise misstatements but misread their effect, resulting in false conclusions.

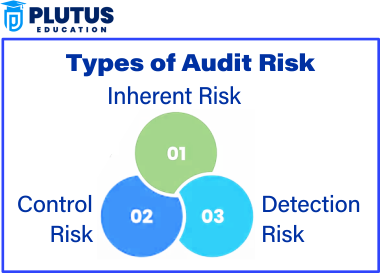

Types of Audit Risk

Audit risk refers to the chance that an auditor can wrongly deliver a clean opinion on financial reports, including material misstatements. Auditors classify audit risk into three main types: inherent risk, control risk, and detection risk.

Inherent Risk

Inherent risk is the natural risk of material misstatement in financial statements due to error or fraud. It spans beyond an audit and is shaped by elements like the nature of transactions, industry-specific rules, and management character. Some industries, like the banking or pharmaceutical industry, have a high level of regulation and compliance to navigate, which can increase the potential inherent risks for those companies.

Also, high risk can be worse when management is pressured to deliver on financial commitments or reporting is not transparent. For example, a rapidly growing startup may carry a higher inherent risk because its financial processes are still developing. Auditors should consider these elements to adequately adjust their audit procedures and reduce the risk of material omissions.

Control Risk

Control risk arises when a company’s internal controls fail to prevent or detect material misstatements. Weak internal controls, lack of oversight or inadequate policies may increase control risk. For example, a company is susceptible to massive errors or fraud without proper approval processes for financial transactions.

In addition, organisations that lack proper segregation of duties or do not ensure that employees receive sufficient training to adhere to internal control procedures can also face increased control risk. For example, when one employee is responsible for recording and approving transactions, the risk of errors or fraud increases. To identify where controls can be improved to reduce control risk further, auditors assess the effectiveness of internal controls.

Detection Risk

Detection risk is when an auditor’s procedures fail to identify material misstatements. The risk of losing out on this depends on the audit procedures and the auditor’s expertise. For instance, if an auditor only depended on manual validations rather than automated tools, the risk of detection may be heightened.

Auditors are also employed to thoroughly analyze financial statements using several tools, data analytics, and sampling methods to minimize detection risk. For example, tools can monitor thousands of transactions over a month to determine outliers that may signify an error or other fraud-related issues. Auditors keep themselves educated and trained to address the latest risks that could lead to material misstatements in the financial statements.

What is an Audit Risk Model (ARM)?

Auditors employ the Audit Risk Model (ARM) to evaluate and control audit risk. Auditors use it to evaluate the financial statement audit’s risk and design their procedures. The ARM is based on the relationship between the three kinds of audit risk: Inherent Risk, Control Risk, and Detection Risk.

Audit Risk = Inherent Risk × Control Risk × Detection Risk

Formula of Audit Risk Model

Audit Risk = Inherent Risk × Control Risk × Detection Risk

Audit Risk: The overall risk of issuing an incorrect audit opinion.

Inherent Risk: The natural risk of material misstatement.

Control Risk: The risk of internal control failures.

Detection Risk: The risk of auditor procedures failing to detect misstatements.

Audit Risk Model Calculation and Example

The ARM (Audit Risk Model) walks auditors through risk assessment and material misstatement in financial statements. This structured approach helps mitigate potential fraud and misstatements, significantly strengthening the financial reporting process. The process contains three main steps:

Step 1: Identify the Types of Audit Risk

The first and most important step is identifying the type of audit risk, inherent, control and detection. Given below in more detail:

- Inherent Risk (IR): The inherent risk of financial statements being fraudulently manipulated (or misstated) prior to considering the effectiveness of internal controls. Higher in sectors whose operations are tightly regulated (pharmaceuticals, banking, etc.).

- Control Risk (CR): The risk that a company’s internal controls will fail to prevent or detect material misstatements. Grows when controls are lacking, like inadequate approval processes or insufficient supervision.

- Risk of Detection (DR): This represents the risk that audit procedures will not be able to detect material misstatements. It all depends on audit techniques, the sample size and overall audit testing.

Step 2: Apply the Audit Risk Formula

This equation helps auditors quantify the overall risk and determine the necessary level of audit procedures. The formula defines the relationship between these components:

Audit Risk=Inherent Risk×Control Risk×Detection Risk

Step 3: Adjust Audit Procedures Based on Risk Level

If audit risk is high, then detection risk can be decreased by increasing audit procedures. Widen sample sizes, use sophisticated analytical tools and rigorous audits. If audit risk is low, auditors can perform standard audit procedures but must ensure that significant risks have been covered.

Example Calculation of Audit Risk

Let’s understand the Audit Risk Model with a practical example:

Example:

- Inherent Risk = 50% (high due to complex transactions)

- Control Risk = 40% (moderate due to average internal controls)

- Detection Risk = 10% (low due to effective audit procedures)

Using the formula:

Audit Risk = 0.50 × 0.40 × 0.10 = 0.02 or 2%

This means there is a 2% chance that the auditor may issue an incorrect opinion.

Audit Risk FAQs

What are the three audit risk types?

The three types include inherent risk, control risk, and detection risk. The three risks establish the probability of financial misstatements.

How is audit risk computed?

Audit risk is computed through the formula AR = IR × CR × DR, where each risk factor is computed concerning company conditions.

What is the audit risk model used for?

The audit risk model assists auditors in assessing overall audit risk and deciding the extent of audit procedures needed.

How is risk-based internal audit different from external audit risk?

Risk-based internal audits enhance internal controls, whereas external audit risks relate to financial misstatements in public reports.

How can detection risk be minimized?

Detection risk can be minimized by augmenting audit testing, applying analytical procedures, and examining more financial transactions.