Audit procedures may prevent auditors from verifying the occurrence of every financial transaction pertinent to an audit, they resorted to numerous approaches of sampling. In this way, audit procedures may be applied to selected portions of data, and findings may be extrapolated to the whole population. Varieties of sampling used in audits include statistical and non-statistical sampling. Performing audit sampling, both statistical and non-statistical, helps auditors assess risks, from fraud detection to financial compliance.Statistical sampling refers to those sampling provisions based on probability. It guarantees that unbiased procedures for choosing the sample are being applied. Non-statistical sampling is when the auditor applies their discretion. EEvenin the area of judgment when selecting samples. Both statistical and non-statistical sampling have their pros and cons. It depends on the audit purpose.

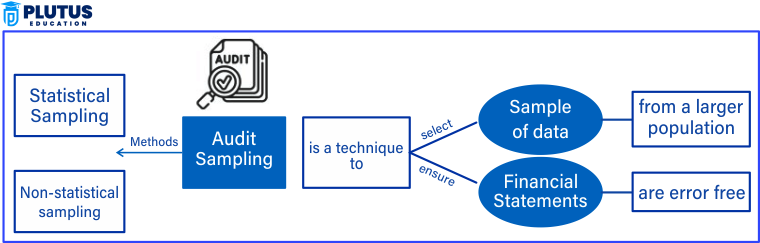

What is Audit Sampling?

Instead of reviewing every transaction, audit sampling is selecting and evaluating a representative portion of financial data. This method allows auditors to conclude the entire dataset based on the selected sample. Audits would become impractical, costly, or time-consuming without sampling, especially for large organizations with thousands of transactions.

Then, fourth, the accuracy of the audit rests with the quality of selected samples. If the auditors choose an unrepresentative sample, misleading conclusions are likely to result. The auditors, therefore, must have a structured procedure for audit sampling to make sure that the sample selected is representative.

Importance of Audit Sampling

Audit sampling is essential because it ensures adherence to accounting standards, regulatory requirements, and internal controls.

- Companies must give these assurances that their audit is a basis for maintaining financial transparency, fraud detection, and prevention of material misstatements.

- An efficient sampling process would lead auditors to areas of high risk and thus enhance audit efficiency without wasting time on low-risk transactions.

- Proper application of audit sampling thus gives auditors the confidence to testify to the correctness of financial statements and the absence of material error.

- Such processes ultimately uphold investor confidence and compel adherence to financial reporting regulations.

Types of Audit Sampling

Inlining with their specific nature are two prominent methods of sampling in auditing. They are statistical audit sampling and non-statistical audit sampling. Both methods contain one or another means of judging and processing financial data for effective results but are different in sample selection or evaluation. Knowing these contrasts helps auditors choose the proper sampling method for a particular audit.

Statistical Audit Sampling

Statistical audit sampling is a method of sampling based on a probabilistic theory. Each transaction involved has a known chance of being selected, making the process unbiased and further defended and justified mathematically. The auditor uses statistical formulas to determine the sample sizes and evaluate errors.

- Objectivity: The probability basis for sample selection eliminates personal judgment on accepting or rejecting samples.

- Quantifiable evidence: The auditors justify the probability of an error occurrence in financial records, thus utilizing statistical evidence to back their audit opinion.

- Consistent methodology: Statistical sampling implies using defined mathematical principles to enhance audit verifiability and reliability, meaning different auditors use the same sampling method and arrive at the same conclusion.

- Requires special skills: Even though statistical sampling is the most accurate, it requires applying some special skills.

Auditors are required to be aware of the probability theory and statistical considerations. In addition, using computer software for efficient data processing will add value.

Non-Statistical Audit Sampling

Non-statistical audit sampling supports selecting and evaluating audit samples based on the auditor’s training and experience. Instead of probability approaches, the auditor determines judgmentally the sample size and the criteria for its selection based upon the particular circumstances and risk assessment.

- Flexibility: Without strict statistical rules, the auditor can determine their sample selection criteria according to industry practice and knowledge of their company’s operations. Therefore, in complex audits, non-statistical sampling works better.

- Faster: Non-statistical sampling is easier and quicker because it does not burden calculations heavily. A precious saving of time can be made, especially in cases where the audit is required to meet a tight deadline.

- More prone to imperfections: Non-statistical sampling may be more biased since the auditor makes individual decisions in sample selection. That means the auditor could inadvertently select a sample that forwards a specific agenda while overlooking serious flaws/errors that would not affect that agenda.

- Less defensible: The non-statistical approach is not as easily defended because it does not provide for a measurable probability of error. Thus, if the regulators challenge any audit conclusions reached, the auditors may find it more difficult to defend how they arrived at that conclusion.

Although both forms are essential for any type of audit, while statistical sampling delivers accuracy and consistency, non-statistical sampling permits the auditor to draw on their expertise to identify areas of greatest risk transaction-wise. Hence, under many circumstances, the auditor will adopt both techniques to find an appropriate compromise between efficiency and precision.

Methods of Audit Sampling

Auditors’ various audit sampling methods are adopted for picking and analyzing financial traffic. Auditors have their method based on the audit objectives, the volume of data, and the degree of risk. Each method has its advantages and disadvantages.

Random Sampling

Random sampling takes a sample from the population without any discernible pattern. All transactions have equal chances of being selected, which ensures an unbiased selection process.

- Eliminates selection bias: In this kind of selection, auditors couldn’t favor specific transactions unintentionally. Thus, it becomes a very fair and objective audit.

- Statistically valid: Random sampling obeys the rules of statistical audit sampling; thus, it is a reliable method for the audit for which great accuracy is required.

- Not always risk-based: One drawback is that random sampling does not give high priority to high-risk transactions. If not selected randomly, little or no attention might be given to some critical areas.

Systematic Sampling

Systematic sampling picks every “n-th” unit after deciding on a starting point from a list. This guarantees a structured and evenly distributed sample selection.

- Simplifies selection process: Systematic sampling is easy to implement since auditors only need to define the selection interval (e.g., every 10th transaction).

- Allows for even coverage: Unlike purely random sampling, systematic sampling spreads selected items across the dataset, reducing the risk of missing significant patterns.

- May introduce hidden bias: If the dataset follows a recurring pattern (e.g., similar transactions every 10 entries), systematic sampling could unintentionally favor certain transactions.

Stratified Sampling

Stratified sampling divides a population into subgroups based on specific characteristics such as transaction size, department, or risk levels. From each stratum, auditors will select a sample.

- The increase in sample diversity: All sample categories are released to facilitate a more thorough audit.

- Centers on high-risk strata: More samples could be assigned to the high-risk strata so that enough attention is paid.

- More complex to implement: This approach requires more planning on developing appropriate subgroups and the proportion of each sample.

Haphazard Sampling

Haphazard sampling is a non-statistical technique of audit sampling in which the auditors choose items for an audit in an unmethodical way. It is dependent on convenience rather than the structured criteria.

- Simple and quick: The best example of such sampling techniques is haphazard sampling, which makes this quick and easy as there are no complicated selection rules.

- Considerably vulnerable to bias: Because it is not random in its selection, auditors will have a substantial likelihood of biased sampling since they might be drawn to similar or easily accessible transactions.

- Defenseless under regulatory scrutiny: Regulators and outside reviewers might dispute conclusions using such sampling techniques.

Monetary Unit Sampling (MUS)

MUS selects transactions based on their monetary amounts, giving preferential treatment to the most significant transactions. This is instrumental in the detection of material misstatements.

- More significant transactions: Consequently, more significant transactions are more liable to misstatements, thereby increasing overall audit efficiency in focusing on high-value items.

- Works quite well with financial statement audits: MUS fits naturally into the context of auditing standards addressing material misstatements.

- We will miss some minor errors: As smaller transactions will not have a strong chance of being selected, some minor errors might be lost on the net.

Auditors use those sampling techniques for the audit based on objectives, risk levels, and available resources. The combination of several methods is often beneficial in promoting a successful audit.

How to Choose the Right Audit Sampling Technique?

Choosing the proper audit sampling method is one of the most critical considerations. The choice will determine how effective, efficient, and accurate the audit findings will be. After all, an auditor must carefully weigh several factors before using the appropriate audit sampling method.

- An audit’s nature, database size, risk involved, and regulations will be the determining factors.

- There is no one correct sampling technique for every audit.

- The auditor must consider the purpose of the audit, the type of financial transaction examined, and the likelihood of mistakes or fraud.

- The goal is to choose a technique to validate the conclusion and meet audit standards.

Types of Audit Sampling FAQs

1. What are the different types of audit sampling?

The different kinds of audit sampling include statistical audit sampling and non-statistical audit sampling. Under each type, auditors use other methods like random, systematic, stratified, haphazard, and monetary unit sampling.

2. What is the difference between statistical and non-statistical audit sampling?

Statistical audit sampling relies on probability-based approaches to create objective assessment results, while non-statistical audit sampling uses the auditor’s judgment, making it more flexible but less scientifically rigorous.

3. How do auditors choose appropriate audit sampling techniques?

Auditors use criteria involving risk levels, audit objectives, amount of data, and regulatory requirements to determine the method to be adopted.

4. What is risk-based audit sampling?

Risk-based audit sampling focuses on choosing transactions with more significant risks instead of random or systematic forms.

5. Why is judgmental sampling used in auditing?

Judgmental sampling involves the expertise of auditors to choose transactions for review selectively. It can also be applied when historical data indicates more at-risk areas. The limitations of this type of sampling arise due to the possible bias involved.