The definition of assertion in auditing refers to management’s statements or representations. It is concerning about the attributes of financial statements. The auditors use these assertions. It is to verify whether the financial statements represent a company’s financial position fairly. Management makes assertions about account balances, transactions, and presentation of financial information. The auditor evaluates these assertions using procedures. They include testing, confirmations, and analytical review. It is used to identify misstatements, fraud, or errors that would influence economic decisions.

Assertions associated with financial statements fall into existence, completeness, valuation, accuracy, and presentation categories. The auditor’s role is to test these assertions to identify possible errors. To detect fraud or misstatements among these assertions. The auditing standards set out by boards present more detailed classes of assertions. It helps evaluate financial statements. These assertions are helpful for financial transparency for the auditor, accountant, and business.

Assertion Meaning in Audit

Assertions are what an auditor interprets as statements. Or representations made by the management about the elements of financial statements. Such assertions work as a basis for the auditor to verify whether the financial statements are accurate. Also to check whether they areaccording to the accounting standards.

Management assertions cover areas like account balances, transactions, and presentation of financial information. The auditor will claim to have assessed these assertions through tests,. Also theough confirmations, and analytical reviews. It is to investigate whether misstatements, fraud, or errors exist. Specially in some area that would affect decisions about finances.

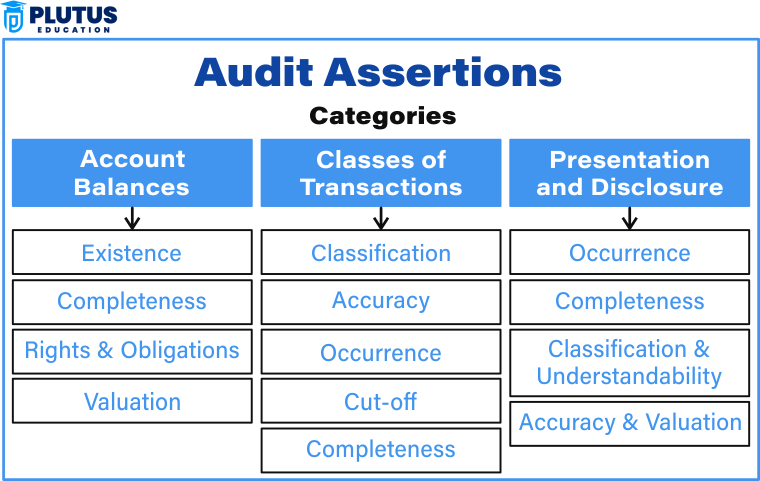

Audit assertions may fall into different categories, such as:

- Assertions on classes of transactions (sales, purchases, expenses, etc.)

- Assertions about account balances (cash, inventories, receivables, etc.)

- Assertions concerning presentation and disclosure (i.e., in line with financial reporting standards)

These assertions are critical for auditors in forming an opinion on financial statements . It is guaranteeing the credibility of financial information.

Financial Statement Assertions

PCAOB assertions are standards for auditors to assess the public company’s financial statement. The assertions are tested for whether the financial statement is accurate, reliable, and consistent . That too with financial reporting requirements. There are five key areas of assertions classified under PCAOB for financial statements:

Existence or Occurrence Assertion

This assertion ensures that all assets, liabilities, and transactions have been recorded. The auditors will physically verify them, contracts will be reviewed, and transactions will be confirmed.

Completeness Assertion

Completeness assertion is to ascertain that all transactions that should be covered in audit work have been recorded. Audit expects unrecorded liabilities or untimely revenue. Omission affects the actual financial statement presentation.

Valuation or Allocation Assertion

The valuation assertion in auditing ensures the appropriate recording of assets, liabilities. Also appropriate recording of revenue. The auditor will check depreciation schedules, inventory, and fair value estimates.

Rights and Obligations Assertion

This assertion states that an entity owns the asset and is legally liable for all its liabilities. The auditor checks the land ownership and entitlement documents.

Presentation and Disclosure Assertion

The auditor ensures that the financial statement presentation complies with accounting principles. Disclosures should be complete and reasonably understandable . so as not to mislead the users of the financial statements.

The PCAOB assertions guarantee the transparency and accountability of financials. It is by giving auditors a structured approach.

Audit Assertions ASB Standards

The Accounting Standards Board (ASB) standard assertions tell auditors about the examination of financial statements . It is for public and private entities. The assertions guide auditors in ascertaining transactions, account balances, and disclosures.

The ASB has put forth the following three main categories of assertions:

- Assertions concerning classes of transactions and events

- Assertions concerning account balances

- Assertions concerning presentation and disclosures

Each assertion helps ascertain financial statements’ accuracy, completeness, and presentation.

Assertions About Classes of Transactions and Events

These assertions concern revenue, expenses, and other transactions. They ensure that the proper recording and classification of transactions have been done.

- Occurrence Assertion: This assertion ensures that all recorded transactions happen. Auditors look out for fake sales as well as fraudulent purchases.

- Completeness Assertion: The completeness assertion in an audit ensures that all the transactions are recorded. Auditors verify the financial records for missing transactions.

- Accuracy Assertion: Under the accuracy assertion in an audit, the transactions have been appropriately recorded. The auditors examine invoices, receipts, and financial documentation.

- Cutoff Assertion: This confirms that transactions have been recorded in the proper period. The auditors check year-end transactions.

- Confirmation of Classification: Assertions ensure that the transactions are correctly classified or presented in financial statements. The misclassification might confuse the stakeholders.

Transaction assertions help an auditor detect errors and fraud in the accuracy of financial statement reporting. Auditors will check whether transactions relate to:

- Complete and Proper Classification

- Accurate Recording

- Validity and Authorization

- Presentation in compliance with Accounting Principles

- Key Assertions Regarding Transactions

Assertions About Account Balances

The existence assertion in the audit, completeness, valuation, and rights/obligations assertions are subsumed in this. Auditors apply the verification of the accuracy of balance sheet items to them. Assertions about account balances facilitate the auditors in verifying the accuracy as far as balances of assets, liabilities, and equity; such assertions enable the financial statements to reflect the actual position of a company. Such assessments are as follows:

- Existence Assertion: The existence assertion in the audit affirms that reported assets and liabilities exist. Corporal audit verification will use auditors’ evidence to establish possible assets and liabilities through bank(s) balance verification.

- Completeness Assertion: This assertion ensures that all assets and liabilities are recorded. All missing liabilities can mislead the investors.

- The valuation assertion states that assets and liabilities should be recorded at actual values. Auditors consider examining depreciation, inventory valuation, and impairment losses during the audit.

- Rights and Obligations Assertion: These assertions ensure the company’s legal title to its assets. The auditors examine documentation and agreements.

Claims referring to account balances are valuable in identifying financial misstatements and, more importantly, in the prevention of such misstatements.

Assertion on Presentation and Disclosure

These assertions relate to whether information about presentation and disclosure standards is complete and presentable. Auditors assess the adequacy of the notes and supplementary disclosures. With that, ASB standard assertions are being applied by auditors in structured audits to uphold the credibility of financial reporting.

Assertion Meaning in Audit FAQs

What does assertion mean in an audit?

The assertion meaning in audit refers to the claims that management undertakes concerning the accuracy of the financial statements. These assertions help the auditors to verify whether financial reports are complete, accurate, and fairly presented.

What are the types of assertions in an audit?

The significant assertions in the audit include Assertions regarding transactions, such as occurrence, completeness, and accuracy. Assertions about account balances include existence, valuation, rights, and obligations. Assertions regarding presentation and disclosure, such as classification, completeness, etc.

What is completeness assertion in an audit?

The completeness assertion in an audit ensures that all transactions, balances, and disclosures are comprehensive. Auditors check if liabilities, revenue, or expenses are missing.

What does accuracy assertion mean in an audit?

The accuracy assertion makes it possible for auditors to put checks on invoices, financial reports, and calculations that record information in the financial statements.

Why are management assertions essential?

Management assertions in the audit are essential because they provide the basis upon which an auditor assesses the financial statements. These assertions help detect fraud and misstatement and help in transparency in financial reports.