Assurance engagement is a professional service where an independent practitioner assesses financial. Non-financial data to improve its reliability for stakeholders. Such engagements establish confidence in an organisation’s reports, statements. Compliance with regulatory requirements. Assurance engagement is typically applied in financial audits, compliance reviews, and performance evaluations. In this paper, we shall discuss the definition of assurance engagement and its main characteristics. The types, advantages, and disadvantages to familiarise ourselves. Its application in auditing and business decision-making.

Assurance Engagement Meaning

An assurance engagement is a professional audit or accounting review process to check the accuracy and reliability of an organisation’s presented information by an independent lead. Whether to ensure stakeholders, like investors, regulatory authorities, and management. That the information is free from material misstatement or bias. The purpose of an assurance engagement is widely recognised.

Assurance engagement example: an assurance engagement is a financial audit done by an external auditor to verify a company’s financial statements. An opinion of the auditor on adherence to International Financial Reporting Standards (IFRS). The absence of misstatements in the financial statements.

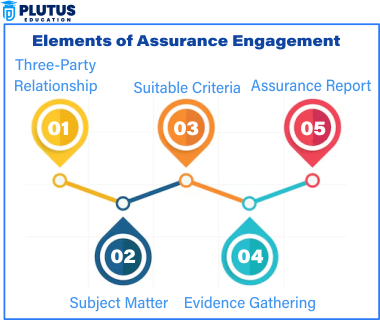

Elements of Assurance Engagement

The process of conducting an assurance engagement is well structured. It includes several steps that ensure the confidence of the stakeholders in the output provided to them. Three-party relationships, subject matter, appropriate criteria, evidence gathering. Assurance reports are the five primary elements that ensure the effectiveness and reliability of the engagement.

Three-Party Relationship

In an assurance engagement, the relationship involves three parties: the responsible party, the practitioner (auditor), and the intended users. The responsible party is the person or entity preparing the subject matter. For example, a company’s management presenting financial statements. The independent professional who performs the engagement and evaluates the subject matter. The intended users are the stakeholders who depend on the assurance report, such as investors, regulators, or lenders.

Subject Matter

Here, the subject matter is the information that is the subject of the assurance engagement. This may involve financial statements or sustainability reports. It can address internal controls. The subject matter needs to be clearly defined to ensure that the practitioner assesses the appropriate data set. This, in turn, offers clarity and assurance to the target users.

Suitable Criteria

The practitioner considers whether the subject matter is per objectively verifiable criteria. Such as Generally Accepted Accounting Principles (GAAP) or International Standards on Auditing (ISA). The criteria are standards used to find the truthfulness and trustworthiness. The criteria are set to enable an efficient, objective, transparent, and industry-compliant audit.

Evidence Gathering

The auditor obtains considerable and appropriate evidence on whether the subject matter applies to the criteria or not as part of the engagement. Typical evidence-gathering procedures include examining documents, data analysis, and interviewing management. Gathering sufficient and appropriate evidence allows the auditor to provide assurance based on strong evidence.

Assurance Report

An assurance report, in the end can either provide reasonable or limited assurance over the reliability of that subject matter. Providing the correct information to the intended users makes them trust this subject. It formally ends the engagement and provides leading stakeholders with the information. To make decisions and note the final document of record.

Types of Assurance Engagement

There are several types of audits, including financial statement, internal, compliance, performance, and information systems audits. Each designed to provide specific information to improve organizational transparency and performance.

Internal Audit

Audits are conducted internally by a company’s own auditors. These auditors assess the company’s internal controls, risk management processes, and operational efficiency. The ultimate goal of an internal audit is to assist the organization in enhancing. Its internal protocols, governance structure, and performance. Internal auditors help promote efficiency, safety, and regulatory compliance. By identifying potential weaknesses and recommending improvements.

Compliance Audit

When it comes down to it, a compliance audit is a checkpoint to make sure the organisation is abiding by laws, regulations, and internal policies. The auditors review whether or not the organization adheres to legal requirements for taxation. Industry regulations, and operations. By confirming compliance, this kind of auditing enables the organisation to avoid legal penalties, fines, and reputational damage. It also shows the company’s dedication to maintaining high regulatory compliance levels.

Financial Statement Audit

The most popular type of assurance engagement is the financial statement audit. Auditors check the financial statements of an entity to provide an opinion. Whether it presents a true and fair view of the financial position and performance. It is also a thorough examination of the statements to ensure they are consistent with accounting standards such as GAAP or IFRS. Thus, it offers stakeholders confidence in the organisation’s financial health. The audit is designed to ensure the accuracy of the financial statements and provide assurance to stakeholders. Such as investors, creditors, and regulators about the reliability of the financial information.

Performance Audit

It assesses the organisation’s operations’ economy, efficiency, and effectiveness. Beyond financial statements, operational audits. Check how well the organization is performing, and they review. Whether the organization is meeting its goal. The idea is to ensure that resources are allocated in the best possible way to maximise results. Performance audits allow organisations to identify areas for improvement. Eliminate waste, and improve their overall operations to drive more success and value for their stakeholders.

Information Systems Audit

An information systems audit (it audit) primarily evaluates an organization’s systems. This refers to the protection of data, controls of the system, and IT governance framework overall. Auditors determine whether the tech infrastructure is operating effectively and securely. The organisation’s information systems are managed, secured, and aligned. With the objectives of the business. IT audits identify vulnerabilities and recommend improvements. To protect sensitive data and prevent cyber threats.

Benefits of Assurance Engagement

Many benefits of assurance engagements are in business, investors, and regulatory authorities.

- Enhances Credibility and Trust: Independent assurance reports increase confidence in financial and non-financial data. Investors use these reports to reach informed conclusions. Assurance engagements strengthen the company’s and its management’s credibility by offering an impartial assessment. Its financial position and integrity, thereby fostering investor confidence.

- Improves Compliance with Regulations: Assurance engagements help businesses. Comply with financial reporting standards and regulatory requirements. They guide companies so they can dodge fines and lawsuits. By ensuring their activities meet the standards of the laws and industries that govern them. It also establishes trust with the regulators. While giving a competitive edge to the business.

- Identifies Risks and Weaknesses: Assurance engagements can find errors, fraud, and weaknesses in internal control. They offer suggestions for improving risk management operations. As these vulnerabilities, it helps the businesses reduce the respective risk. Optimizing their system and ensuring long-term stability and success, such as assurance reports.

- Improves Decision-Making: Assurance reports enable management to make better financial decisions and run operations efficiently. This gives businesses data-driven decision-making based on areas that need improvement. With accurate information, management can manage resources & improve processes. It augment strategic planning for growth.

- Enhances Corporate Governance: Assurance engagements encourage transparency and accountability in financial reporting. They also help make sure management acts ethically and follows best practices. Assurance reports enhance good governance and enforce a robust corporate culture, ensuring that the company’s financial statements accurately and ethically reflect its performance.

Limitations of Assurance Engagement

While assurance engagement has advantages, some limitations impact its scope and reliability.

- Cannot Provide Absolute Assurance: Assurance engagements can provide reasonable assurance but not absolute assurance, so expect some risk. Auditors strive to be a source of confidence. But cannot ensure complete accuracy because of uncertainties in financial reporting and operations.

- Time-Intensive and Expensive: Performing assurance engagements may take a lot of time, effort, and money. It requires an in-depth analysis of data, investigations, and assessments that can be costly for enterprises. At the same time, we don’t have to lose sight of the fact that these costs are necessary for creating accuracy and trust in financial reporting that provides value for the investment.

- Reliance on Management’s Data: Assurance providers rely on data inputs from management that may be incomplete or manipulated. Auditors are expected to take this information at face value, but the reality is that data can be biased or incorrect.

- Limited Scope: The analysis relates only to certain prescribed topics and will not be binding upon all risks. Generally, Auditors should examine specified areas of all aspects of finance according to general principles, so some risks or problems may be left unexamined. Specific agreed-upon objectives dictate the scope of an assurance engagement.

- Subject to Human Judgment and Errors: Because of auditors’ subjective judgments or incompetence, they sometimes misinterpret the data or are unable to discover concealed fraud. Auditors follow set procedures, but there is always the possibility of human error when analyzing complex financial data.

Assurance Engagement FAQs

What is assurance engagement?

An engagement type wherein assurance is provided refers to the process of independent review where auditors verify that financial or non-financial information is accurate and reliable.

What are the types of engagements within assurance?

They include reasonable assurance, limited assurance, compliance assurance, performance assurance, and sustainability assurance.

What is the difference between assurance engagement and audit engagement?

Audit engagement offers a comprehensive financial analysis and reasonable assurance, whereas assurance engagement encompasses wider scopes, such as compliance and risk management.

What are the benefits of assurance engagement?

It increases credibility, better compliance, risk identification, better decision-making, and corporate governance.

Why does assurance engagement have limitations?

It cannot offer complete certainty, relies upon management’s data, is expensive and can be narrow in scope.