Audit assertions are essential components of the auditing process. Assertions by management indicate that they have some basis for concluding that the financial statements are accurate and reliable. An auditor uses them to assess whether financial records depict a company’s financial position. Without audit assertions, it would be difficult for auditors to determine if the financial statements are materially misstatements.

The audit committee ensures that the company is transparent and compliant . Especially with its accounting standards throughout the auditing process in an audit. Therefore, the audit committee works with auditors to ensure that the corresponding financial statement reflects the health of the company.

The audit assertion can be understood as being risky. So, providing tests of control within an organisation, in addition to having such tests serve to strengthen the integrity. Specially of financial information.

Audit Assertions Meaning

Audit assertions relate to the financial statement items that are management’s representations. These representations ensure that the reported transactions were according to the standards. Also that the standards reflect the company’s economic status. Auditors check these assertions to test whether the financial statements are error-free and fraud-free.

Auditors who examine a company’s financial records verify that transactions, balances, and disclosures satisfy specific criteria. These criteria, called assertions, allow the auditor to form a judgment about the financial reporting by the company. Suppose management asserts that the financial statements are complete and accurate. In that case, it means they feel sure that all transactions have been recorded correctly and that there are no hidden liabilities or overstated assets.

Audit assertions allow auditors to assess the various financial reports effectively. They will also not provide any structured approach for auditors to evaluate financial statements if they lack these assertions. Assertions apply to multiple parts of financial statements, covering assets, liabilities, revenue, expenses, etc. By testing these assertions, auditors gather audit evidence and assertions about the reliability of financial information.

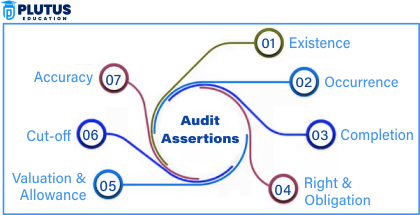

Types of Audit Assertions

Different types of audit assertions exist for other purposes. Auditors classify these assertions according to the financial statement aspect they will review. Each assertion gives a different way of proving that the financial information is accurate, complete, and presented correctly.

There are three main types of audit assertions:

Existence Assertion in Auditing

All assets, liabilities, and equity balances exist at the balance sheet date. This assertion assures auditors that the company is not reporting fictitious assets or overstating liabilities.

If a subject has accounts receivable of $10 million, he must be able to confirm this: Receivables are meant to be owed to them by customers. This assertion is usually verified by reviewing supporting documents such as customer invoices and confirmations, considering that non-existent assets are reflected in the company’s financial statements; this may mislead investors and other stakeholders.

Completeness Assertion in Auditing

The completeness assertion in auditing tests that all transactions and activities that should be recorded are reflected in the financial statements. If, for example, a corporation does not include a related expense or liability, this can substantially misinform users about the corporation’s finances.

Auditors test completeness by matching financial transactions with recorded supporting documents—for example, invoices, contracts, and purchase orders. They will also compare financial statements to general ledger balances to check for omissions. This assertion becomes highly critical in audit assertions for accounts payable; for instance, a company might attempt to understate liabilities to show a healthier financial position.

Accuracy Assertion in Audit

Accuracy assertion in audit guarantees that the financial data has been recorded correctly. This implies that all transactions are reflected correctly in the financial statements without error or misstatement.

Auditors usually check this assertion by carrying out mathematical checks, examining data entries, and reconciling amounts in financial statements with supporting documents. For example, accounts receivable audit assertions assure auditors that their financial accounting system reflects valid customer invoices in the right quantities and bookings.

Valuation and Allocation Assertion

Assignments are made to record assets, liabilities, and equity at their appropriate values. Assets and liabilities must be valued relatively, following proper accounting principles.

For example, auditors check whether the firm has depreciated assets properly and followed the proper valuation techniques in audit assertions for fixed assets. The higher the value a company places on its assets, the more it blinds the eyes of investors about its actual financial position.

Rights and Obligations Assertion

Such an assertion claims the company has legal rights to its assets and liability responsibilities. The reason is that such assertions are safeguards against any organisation from claiming ownership of assets it does not own.

If a building is reported as an asset by a company, it must confirm that it owns the legal rights to that property. The same is true for audit assertions of inventory; auditors check that the inventory belongs to the company and is not used as collateral to obtain a loan.

Presentation and Disclosure Assertion

The presentation and disclosure assertion ensures that all financial information is presented correctly and disclosed by accounting standards. Companies must provide clear, accurate, and complete financial disclosures.

For example, auditors examine whether financial statement notes include all necessary details about contingencies, related-party transactions, and accounting policies. This assertion is crucial in audit assertions for revenue, as companies must disclose revenue recognition policies clearly to avoid misleading stakeholders.

Audit Assertion Case

To understand the working of audit assertion examples in a real-life situation, one might consider a case like this:

XYZ Ltd. declares $5 million in inventory on the balance sheet. The auditor inspects this inventory with the following audit assertions:

- Existence Assertion: The auditor inspects the warehouse to ensure the inventory exists.

- Completeness Assertion: The auditor checks purchase records and inventory logs to ensure that all inventory transactions are recorded.

- Accuracy Assertion: The auditor verifies that the inventory cost is matched by supplier invoices and appended duly in financial statements.

- Valuation and Allocation Assertion: The auditor ascertains that the inventory is marked correctly using correct accounting methods, viz FIFO or weighted average cost.

- Rights and Obligations Assertion: The auditor checks whether XYZ Ltd. owns the inventory or holds it on consignment for another company.

- Presentation and Disclosure Assertion: The auditor consults financial statement notes to determine whether XYZ Ltd has disclosed all information related to accounting policies regarding inventories.

Applying these audit procedures and assertions lets the auditor say whether the inventory balance in financial statements is correct and reliable. If some assertion does not apply, an auditor will ask for adjustments or give a qualified audit opinion.

Audit Assertion FAQs

1. Define audit assertion.

Audit assertion is thus the management’s claim regarding the financial statements that they are accurate, complete, and presented in a certain way. These assertions are significant for auditors since they form a basis to ascertain whether the financial statements represent the actual financial condition of the company.

2. How will an audit assertion help the auditors?

Audit assertions offer a clear framework to verify whether the accounts are accurate and reliable. Audit assertions help to come up with clear conclusions based on a set of prescribed practices in audit assertions, which directs the auditor in testing financial transactions, evaluating risks, and ensuring compliance with accounting standards.

3. What are audit assertions for accounts payable?

Audit assertions for accounts payable ensure that all liabilities are recorded correctly. Auditors check whether payables exist, are complete, and are appropriately valued to avoid understating liabilities.

4. How do audit assertions function for inventory?

Audit assertions confirm the existence of inventory, its proper value, and ownership by the company. Auditors do this by physically inspecting inventory and verifying the valuation methods used.

5. What is the functionality of internal controls and audit assertions?

While internal controls and audit assertions work together to prevent financial misstatements, strong internal controls specific to an area and an assertion significantly, impact the weak nature of internal controls that lead to misstatements. Internal controls allow accurate records of transactions, lowering the risks of fraud and error in financial statements.