The whole audit process revolves around two essential components- the audit strategy and the audit plan. These terms are often used interchangeably but are not the same: the audit strategy and plan differ. Hence, all auditors, accounting professionals, and businesses must understand their differences for smooth, efficient, and risk-based auditing.

An audit strategy is a high-level framework explaining how an audit will be conducted. It sets a high-level direction and scope with key areas of focus resulting from a risk assessment and business objectives. The audit plan is a detailed road map listing specific procedures, timelines, and responsibilities for executing that audit strategy.

A strong audit strategy ensures that the auditors will allocate resources effectively, prioritize the high-risk areas, and align the audit objectives with the company’s financial and operational environment. Audit planning may be vague if a strong strategy is absent, leading to potential inefficiencies and errors.

What is an Audit Strategy?

Audit strategy is the overall approach auditors take to perform the audit work. In this case, auditors must establish an overall audit strategy that sets an audit’s scope, timing, and direction at the planning stage.

Auditors usually use the audit strategy to prepare the audit plan, which lists the procedures needed for each relevant assertion of significant accounts and balances in financial statements.

It will rapidly illuminate insights from multiple data sources. Using technology appropriately allows auditors to conduct audits more efficiently. It improves the reliability of their work by enhancing their ability to form valid audit opinions based on appropriate audit evidence.

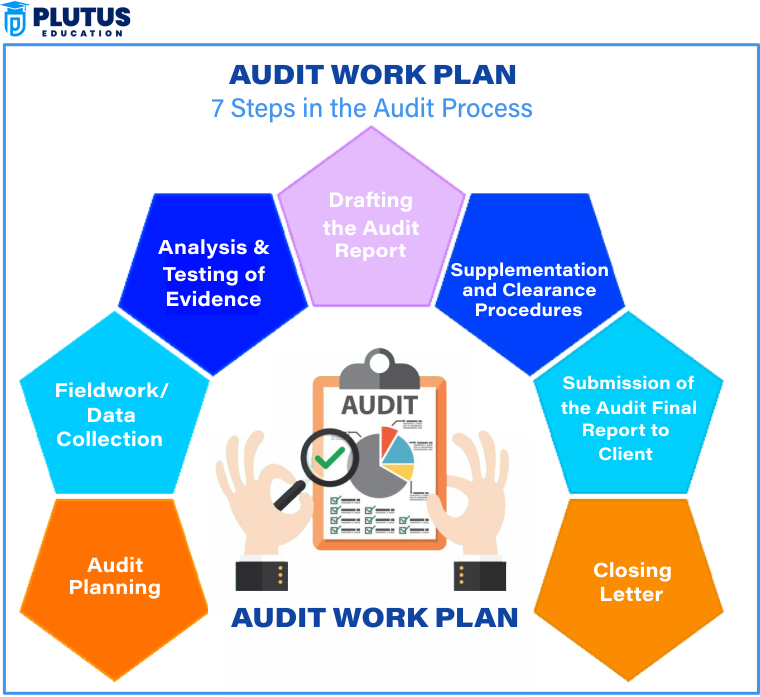

What Is an Audit Plan?

An audit plan refers to a set of specific procedures, operations, and resources required to execute the audit strategy; it serves as a guide for the auditors in keeping the audit process within a systematic outline.

An audit strategy is a high-level plan that defines an overall approach to the scope and direction of an audit. It sets the high-level parameters for conducting the audit. It also gives a more detailed written document that prescribes specific procedures, steps, and methodologies for systematically carrying out the audit strategy.

Audit Strategy vs Audit Plan: Key Differences

The distinction between audit strategy and audit plan is shown above in the table: With audit strategy as the framework and audit plan as the one that lays the road for a structured execution, the two are highly interdependent and key for a successful audit:

| Aspect | Audit Strategy | Audit Plan |

| Definition | A high-level plan that defines the overall approach, scope, and direction of an audit. It provides a broad framework for conducting the audit effectively. | A detailed document outlines specific procedures, steps, and methodologies to execute the audit strategy systematically. |

| Purpose | Sets objectives, identifies key risk areas, and allocates resources efficiently to ensure the audit is well-structured and goal-oriented. | It serves as an operational guide that auditors follow to ensure a systematic, thorough, and efficient audit execution. |

| Components | Audit scope, objectives, risk assessment, audit approach, resource allocation, materiality determination, and use of technology. | Specific audit procedures, assigned responsibilities, timing and scheduling, compliance verification, and documentation guidelines. |

| Focus Areas | Risk assessment, scope determination, and strategic planning for audit efficiency. | Detailed testing, gathering audit evidence, and implementing procedures for financial accuracy verification. |

| Nature of Work | Conceptual and strategic: determines what needs to be done in the audit. | Procedural and operational: focuses on how to execute the audit. |

| Risk Assessment | Identifies and prioritises significant risks before starting the audit to focus on high-risk areas. | Implements tests and procedures specific to the audit strategy to assess and respond to identified risks. |

| Time and Resource Allocation | Specifies how time, workforce, and technology will be allocated throughout the audit process. | Provides a structured timeframe and assigns specific functions to auditors for task completion. |

| Use of Technology and Tools | Defines how audit software, data analytics, and automated tools will assess risk and improve effectiveness. | Specifies which audit tools will be used for data verification, documentation, and report generation. |

| Materiality Consideration | Sets a threshold for material misstatements and determines their impact on financial statements. | Executes specific procedures for testing materiality thresholds and identifying misstatements based on strategy parameters. |

| Audit Approach | Defines whether the audit is control-based, internal-based, or substantive-based (direct transaction testing). | Executes audit procedures based on the selected approach. |

| Audit Planning Process | Defines objectives and prioritises risks, forming the foundation for audit planning. | Marks the conclusion of audit planning; sets the sequence and execution of audit tasks. |

| Documentation Requirements | It offers a broad view of how the audit process should be documented and what key aspects should be recorded. | Specifies the format, structure, and methods for documenting audit findings, working papers, and reports. |

| Examples | Audit Strategy Example: An auditor targets high-risk financial transactions in a company’s accounts and allocates additional resources to fraud-prone areas. | Audit Plan Example: The auditor schedules an in-depth review of revenue recognition policies, assigns a team to verify bank reconciliations, and sets deadlines for fieldwork completion. |

| Execution Stage | Designed before the audit begins to provide a strategic framework for planning and execution. | Developed the audit strategy to provide a structured flow for execution. |

| Importance | Ensures the audit process is risk-aware, efficient, and well-directed. It helps define objectives clearly and avoid unnecessary efforts. | Ensures systematic, well-documented audit execution, minimises errors, enhances compliance, and facilitates timely reporting. |

Components of the Audit Plan

An audit plan refers to a set of specific procedures, operations, and resources required to execute the audit strategy; it serves as a guide for the auditors in keeping the audit process within a systematic outline. The features of the audit plan are:-

Audit Procedures

Audit procedures are the open and secret tests carried out: tracing the transactions, analysing the financial statements, confirming the balances at the auditors’ request, investigating the changes, and checking whether there is any legal frame part of such procedures. They provide enough support of evidence for an auditor to come up with his audit opinion.

Assignment of Responsibilities

According to the audit plan, responsibilities have been assigned to the individual auditors concerning their respective skills and experience. The assignment of responsibility will ensure that such audit matters are covered in full and serve as a control mechanism for distributing the workload along with the appropriate technical expertise within the assigned areas.

Time Allocation and Scheduling

One of the most critical aspects of audits is time control. The audit plan defines when, for each audit procedure, the work is to be done without deviating from the point of a timely work to see that it is successfully brought to a close at that particular time. A brilliant plan is a fairground for any valid audit to run correctly and promptly.

Compliance with Regulations

Auditors should generally be satisfied that their work has been or will be conducted in compliance with all material aspects of all applicable laws and regulations. In a broadly defined sense, auditors believed that the audit plan included procedures to check compliance with relevant accounting standards, taxation laws, and corporation governance provisions in audit plans and execution. The compliance, in turn, fosters a belief in the results of audit findings, which are considered trustworthy and legally sound.

Documentation and Reporting

This audit plan was for the documentation and reporting side of audit results. Documentation is a principle of transparency, accountability, and even a reference to ensure that all auditing conclusions are well-grounded, worthy of respect, and credible against public scrutiny.

With guidance from audit plan auditing work, an auditor would be able to conduct the audit as follows: irreproachably efficient, accurate, and compliant with legal regulations.

Components of Audit Strategy

The elements of the audit strategy will enhance each audit undertaken. Each aspect will strengthen the audit from planned efficiency, well-thought-out, and risk-focused perspectives.

Understanding the Client’s Business and Industry

Therefore, An effective audit strategy can only be developed when auditors understand the client’s unique business and industry context. The company’s model, the primary operational processes, and the flow of operations for financial information systems should be seriously considered. The broader outside factor, such as regulatory requirements, the prevailing economic conditions, etc., should also be considered. All these help the auditors to discover areas that could represent high inherent risk and need to be focused on during the audit process.

Defining the Scope of Audit

The audit scope sets the extent and boundaries of the audit procedures to be performed. Auditors select which financial statements, account items, and transactions will be examined based on materiality and risk evaluations. An explicit scope parameter will help ensure that the audit focuses on and is relevant to the organisation’s financial health under review. A well-defined scope will also allow input efficiency resource allocation and manage the risk of unnecessary audit procedures.

Risk Assessment and Key Focus Areas

The risk assessment is part of an audit strategy that enables the auditor to determine areas with a greater tendency towards material misstatements. This will involve examining inherent risk attributes related to the nature of the business operations, controlling risk factors associated with internal processes, and detecting risk in audit procedures. The auditor may thus concentrate on the high-risk areas for a more focused audit, accuracy, and conformity purposes. A significant impact on risk assessment will result in better audit quality and a lower chance of financial misrepresentation.

Audit Resources and Team Allocation

Effective allocation of resources and specialists is a prerequisite for successfully executing the auditing engagement strategy. The auditors are expected to assess the complexity of the assignment before determining the size of the audit team and the required skill sets. Because of the complexity of the audit, the engagement may call for the inclusion of specialists such as IT auditors or tax experts. Defining the members’ roles and responsibilities will ensure accountability and smooth execution of audit procedures.

Time and Scheduling

A well-stated timeline ensures that the audit operation is done practically without delays. Deadlines are communicated to auditors regarding phases, from initial planning to final reporting, linked to external timelines. Scheduling includes accessing documentation concerning the fieldwork coordinated with client management. The timeliness in activity execution comes in handy in identifying and rectifying issues before the audit deadline.

The Audit Tools and Technologies

There is an occurrence of merging distinguishing auditing tools and techniques in modernism into more accurate and efficacious work performance. While streamlining, auditors use data analytics, automation, and auditing software to do their jobs more efficiently and find deviations. Utilizing digital tools makes handling large amounts of data easier and eliminates human error. In addition, they are combined with cybersecurity, which means that clients’ sensitive information is secured during the audit.

Reporting and Communication Strategy

Effective communication must be present across the audit processes for transparency and collaboration toward listening from the auditors’ point of view. Audit communication schedules are up for establishment between the management and relevant stakeholders regarding the findings and grievances. Regular progress updates and interim reporting help one foresee issues that might be faced before the final production of the audit report. Audits are supposed to provide a structured basis for documentation to ensure audit documentation stays within regulatory standards and gains valuable insight for stakeholders.

Audit Strategy Vs Audit Plan FAQs

1. In terms of audit strategy and audit plan, what is the fundamental difference?

The audit strategy gives a broad approach to the audit, while the plan specifies the particular procedures and steps for implementing the strategy. In simple terms, a strategy provides a roadmap, while a plan ensures structured execution.

2. Without an audit strategy, can audits be performed?

An audit must have a strategy for defining its scope, objectives, and approach, but if it lacks such a strategy, it would lead to an inefficient and unorganised audit process.

3. What role does risk assessment play in audit strategy?

Risk assessment is a significant aspect of the overall audit strategy because it helps the audit focus primarily on the essential financial areas that contain risk.

4. What is an audit plan example?

An example of an audit plan includes audit timetable scheduling, which assigns auditors to various test procedures and due dates.

5. Why is audit strategy important?

The auditors will optimise resources using compliance strategies and simultaneously set a framework for auditing, making it practical and efficient regarding usefulness, relaying information, and allocation.